Hyundai 2015 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2015 Hyundai annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

HYUNDAI MOTOR COMPANY Annual Report 2015

102 103

the former owners of the acquiree and the equity interests

issued by the Group in exchange for control of the acquiree.

The consideration includes any asset or liability resulting from

a contingent consideration arrangement and is measured at

fair value. Acquisition-related costs are recognized in profit

or loss as incurred. When a business combination is achieved

in stages, the Group’s previously held equity interest in the

acquiree is remeasured at its fair value at the acquisition date

(i.e. the date when the Group obtains control) and the result-

ing gain or loss, if any, is recognized in profit or loss. Prior

to the acquisition date, the amount resulting from changes in

the value of its equity interest in the acquiree that have pre-

viously been recognized in other comprehensive income are

reclassified to profit or loss where such treatment would be

appropriate if that interest were directly disposed of.

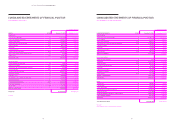

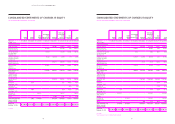

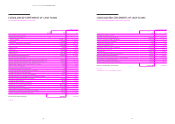

(5) Revenue recognition

1) Sale of goods

The Group recognizes revenue from sale of goods when all of

the following conditions are satisfied:

● the Group has transferred to the buyer the significant risks

and rewards of ownership of the goods; the amount of

revenue can be measured reliably;

● it is probable that the economic benefits associated with

the transaction will flow to the Group

The Group grants award credits which the customers can

redeem for awards such as free or discounted goods or ser-

vices. The fair value of the award credits is estimated by con-

sidering the fair value of the goods granted, the expected rate

and period of collection. The fair value of the consideration

received or receivable from the customer is allocated to award

credits and sales transaction. The consideration allocated to

the award credits is deferred and recognized as revenue when

the award credits are redeemed and the Group’s obligations

have been fulfilled.

2) Rendering of services

The Group recognizes revenue from rendering of services based

on the percentage of completion when theamount of revenue

can be measured reliably and it is probable that the economic

benefits associated with the transaction will flow to the Group.

3) Royalties

The Group recognizes revenue from royalties on an accrual

basis in accordance with the substance of the relevant agree-

ment.

4) Dividend and interest income

Revenues arising from dividends are recognized when the

right to receive payment is established. Interest income is rec-

ognized using the effective interest method as time passes.

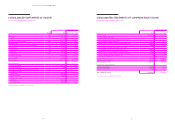

5) Construction contracts

Where the outcome of a construction contract can be es-

timated reliably, the contract revenue and contract costs

associated with the construction contract are recognized as

revenue and expenses, respectively by reference to the stage

of completion of the contract activity at the end of reporting

period.

The percentage of completion of a contract activity is reliably

measured based on the proportion of contract costs incurred

for work performed to date relative to the estimated total

contract costs, by surveys of work performed or by comple-

tion of a physical proportion of the contract work. Variations

in contract work, claim and incentive payments are included

to the extent that the amount can be measured reliably and

its receipt is considered probable. Where the outcome of a

construction contract cannot be estimated reliably, contract

revenue is recognized to the extent of contract costs incurred

that it is probable will be recoverable. Contract costs are rec-

ognized as expenses in the period in which they are incurred.

When it is probable that total contract costs will exceed total

contract revenue, the expected loss is recognized as an ex-

pense immediately.

(6) Foreign currency translation

The individual financial statements of each entity in the Group

are measured and presented in the currency of the primary

economic environment in which the entity operates (its func-

tional currency).

In preparing the financial statements of the individual en-

tities, transactions occurring in currencies other than their

functional currency (foreign currencies) are recorded using

the exchange rate on the dates of the transactions. At the

end of each reporting period, monetary items denominated in

foreign currencies are translated using the exchange rate at

the reporting period. Non-monetary items that are measured

in terms of historical cost in a foreign currency are translated

using the exchange rate at the date of the transaction. Non-

monetary items that are measured at fair value in a foreign

currency are translated using the exchange rates at the date

when the fair value was determined. Exchange differences

resulting from settlement of assets or liabilities and transla-

tion of monetary items denominated in foreign currencies are

recognized in profit or loss in the period in which they arise

except for some exceptions.

For the purpose of presenting the consolidated financial

statements, assets and liabilities in the Group’s foreign opera-

tions are translated into Won, using the exchange rates at the

end of reporting period. Income and expense items are trans-

lated at the average exchange rate for the period, unless the

exchange rate during the period has significantly fluctuated,

in which case the exchange rates at the dates of the trans-

actions are used. The exchange differences arising, if any,

are recognized in equity as other comprehensive income. On

the disposal of a foreign operation, the cumulative amount of

the exchange differences relating to that foreign operation is

reclassified from equity to profit or loss when the gain or loss

on disposal is recognized. Any goodwill arising on the acqui-

sition of a foreign operation and any fair value adjustments

to the carrying amounts of assets and liabilities arising on the

acquisition of that foreign operation are treated as assets and

liabilities of the foreign operation and translated at the ex-

change rate at the end of reporting period.

Foreign exchange gains or losses are classified in finance in-

come (expenses) or other income (expenses) by the nature of

the transaction or event.

(7) Financial assets

The Group classifies financial assets into the following spec-

ified categories: financial assets at fair value through profit

or loss (“FVTPL”), held-to-maturity (“HTM”) financial assets,

loans and receivables and available-for-sale (“AFS”) financial

assets. The classification depends on the nature and purpose

of the financial assets and is determined at the time of initial

recognition.

1) Financial assets at FVTPL

Financial instruments classified as financial assets at FVTPL

include contingent consideration that may be paid by an ac-

quirer as part of business combination to which K-IFRS 1103

applies or financial assets classified as held for trading or

designated as FVTPL upon initial recognition. A financial asset

is classified as FVTPL, if it has been acquired principally for

the purpose of selling or repurchasing in near term. All de-

rivative assets, except for derivatives that are designated and

effective hedging instruments, are classified as held for trad-

ing financial assets which are measured at fair value through

profit or loss. Financial assets at FVTPL are measured at fair

value, with any gains or losses arising on remeasurement rec-

ognized in profit or loss.

2) HTM financial assets

HTM financial assets are non-derivative financial instruments

with fixed or determinable payments and fixed maturity that

the Group has the positive intent and ability to hold to maturi-

ty. HTM financial assets are presented at amortized cost using

the effective interest rate less accumulated impairment loss,

and interest income is recognized using the effective interest

rate method.

3) Loans and receivables

Loans and receivables are non-derivative financial assets with

fixed or determinable payments that are not quoted in an ac-

tive market, and measured at amortized cost. Interest income

is recognized using the effective interest rate method except

for short-term receivables for which the discount effect is not

material.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2015 AND 2014