Cisco 2010 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2010 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

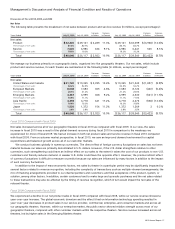

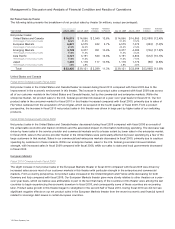

Management’s Discussion and Analysis of Financial Condition and Results of Operations

underway is the enterprise data center market. We believe the market is at an inflection point, as awareness grows that intelligent

networks are becoming the platform for productivity improvement and global competitiveness. We further believe that disruption in

the enterprise data center market is accelerating, due to changing technology trends such as the increasing adoption of

virtualization, the rise in scalable processing, and the advent of cloud computing and cloud-based IT resource deployments and

business models. These key terms are defined as follows:

Virtualization: refers to the process of aggregating the current siloed data center resources into unified, shared resource pools

that can be dynamically delivered to applications on demand thus enabling the ability to move content and applications

between devices and the network.

The Cloud: refers to an information technology hosting and delivery system in which resources, such as servers or software

applications, are no longer tethered to a user’s physical infrastructure but which instead are delivered to and consumed by the

user “on demand” as an Internet-based service, whether singularly or with multiple other users simultaneously.

This virtualization and cloud-driven market transition in the enterprise data center market is being brought about through the

convergence of networking, computing, storage, and software technologies. We are seeking to take advantage of this market

transition through, among other things, our Cisco Unified Computing System platform and Cisco Nexus product families, which are

designed to integrate the previously siloed technologies in the enterprise data center with a unified architecture. We are also

seeking to capitalize on this market transition through the development of cloud-based product and service offerings, through

which we intend to enable customers to develop and deploy their own cloud-related IT solutions, including software-as-a-service

(SaaS), and other-as-a-service (XaaS) solutions.

The competitive landscape in the enterprise data center market is changing, and we expect there will be a new class of very

large, well-financed, and aggressive competitors, each bringing its own new class of products to address this new market.

However, with respect to this market, we believe the network will be the intersection of innovation through an open ecosystem and

standards. We expect to see acquisitions, further industry consolidation, and new alliances among companies as they seek to serve

the enterprise data center market. As we enter this next market phase, we expect that we will strengthen certain strategic alliances,

compete more with certain strategic alliances and partners, and perhaps also encounter new competitors in our attempt to deliver

the best solutions for our customers.

Other market transitions on which we are focusing primary attention include those related to the increased role of video,

collaboration, and networked Web 2.0 technologies. The key market transitions relative to the convergence of video, collaboration,

and networked Web 2.0 technologies, which we believe will drive productivity and growth in network loads, appear to be evolving

even more quickly and more significantly than we had previously anticipated. Cisco TelePresence systems are one example of

product offerings that have incorporated video, collaboration, and networked Web 2.0 technologies, as customers evolve their

communications and business models. We are focused on simplifying and expanding the creation, distribution, and use of

end-to-end video solutions for businesses and consumers, and our fiscal 2010 acquisition of Tandberg ASA (“Tandberg”) is an

example of our increased emphasis on the video market segment.

We believe that the architectural approach that has served us well in addressing the market adjacencies in the communications

and information technology industry will be adaptable to other markets. Examples of market adjacencies where we aim to apply this

approach are mobility, the consumer, and electrical services infrastructure. With regard to mobility, the growth of IP traffic on

handheld devices is driving the need for more robust architectures, equipment and services in order to accommodate not only an

increasing number of worldwide mobile device users, but also increased user demand for broadband-quality business network and

consumer web applications to be seamlessly delivered on such devices. Our fiscal 2010 acquisition of Starent Networks, Corp.

(“Starent”) reflects our recognition of the significance of this market adjacency and our intent to offer solutions that help expand IP

network load capabilities for mobile devices. For the consumer market, through collaboration with technology partners, retailers,

service providers, and content publishers, we are striving to create compelling consumer experiences and make the network the

platform for a variety of services in the home, as broadband development moves from a device-centric phase to a network-centric

model. In the electrical services infrastructure market, we are developing an architecture for managing energy in a highly secure

fashion on electrical grids at various steps from energy generation to consumption in homes and buildings.

We are currently undergoing product transitions within several of our product families, and we believe that many of these

product transitions are gaining momentum based on the strong year-over-year product revenue growth across these product

families. We believe that our strategy and our ability to innovate and execute may enable us to improve our relative competitive

position in uncertain or difficult business conditions and may continue to provide us with long-term growth opportunities.

2010 Annual Report 9