CVS 2000 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2000 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44

|

|

Business Combinations

CVS/Arbor Merger

On March 31, 1998, CVS completed a merger with

Arbor Drugs, Inc. (“Arbor”), pursuant to which 37.8

million shares of CVS common stock were exchanged for all the

outstanding common stock of Arbor. The merger was a tax-free

reorganization that was accounted for as a pooling of interests

under APB Opinion No. 16,“Business Combinations.”

In accordance with APB Opinion No. 16, Emerging Issues Task

Force (“EITF”) Issue 94-3,“Liability Recognition for Certain Employee

Termination Benefits and Other Costs to Exit an Activity (Including

Certain Costs Incurred in a Restructuring)” and SFAS No. 121,

“Accounting for the Impairment of Long-Lived Assets and for Long-

Lived Assets to Be Disposed Of,” CVS recorded a $147.3 million

charge to operating expenses during the second quarter of 1998

for direct and other merger-related costs pertaining to the CVS/

Arbor merger transaction and certain restructuring activities (the

“CVS/Arbor Charge”).The Company also recorded a $10.0 million

charge to cost of goods sold during the second quarter of 1998

to reflect markdowns on noncompatible Arbor merchandise.

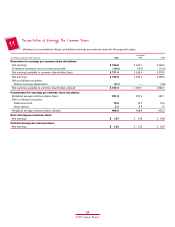

Following is a summary of the significant components of the

CVS/Arbor Charge:

Merger transaction costs included $12.0 million for estimated

investment banker fees, $2.5 million for estimated professional fees,

and $0.5 million for estimated filing fees, printing costs and other

costs associated with furnishing information to shareholders.

Employee severance and benefits included $15.0 million for

estimated excess parachute payment excise taxes and related

income tax gross-ups, $11.0 million for estimated employee

severance and $1.1 million for estimated employee outplacement

costs. The excess parachute payment excise taxes and related

income tax gross-ups relate to employment agreements that

Arbor had in place with 22 senior executives. Employee severance

and benefits and employee outplacement costs relate to 236

employees that were located in Arbor’s Troy, Michigan corporate

headquarters, including the 22 senior executives that were

covered by employment agreements.

Exit Costs ~ In conjunction with the merger transaction,

management made the decision to close Arbor’s Troy, Michigan

corporate headquarters and 55 Arbor store locations. As a result,

the following exit plan was executed:

1. Arbor’s Troy, Michigan corporate headquarters would be

closed as soon as possible after the merger. Management

anticipated that this facility would be closed by no later than

December 31, 1998. Since this location was a leased facility,

management returned the premises to the landlord at the

conclusion of the current lease term, which extended through

1999.This facility was closed in December 1998.

2. Arbor’s Troy, Michigan corporate headquarters employees

would be terminated as soon as possible after the merger.

Management anticipated that these employees would be

terminated by no later than December 31, 1998. However,

significant headcount reductions were planned and occurred

throughout the transition period. As of December 31, 1998, all

of the employees had been terminated.

3. The 55 Arbor store locations discussed above would be closed

as soon as practical after the merger. As of December 30, 2000,

all of these locations have been closed or are in the process

of being closed. Since these locations were leased facilities,

management planned to either return the premises to the

respective landlords at the conclusion of the current lease

term or negotiate an early termination of the contractual

obligations.

Noncancelable lease obligations included $40.0 million for the

estimated continuing lease obligations of the 55 Arbor store

locations discussed above. As required by EITF Issue 88-10,

“Costs Associated with Lease Modification or Termination,” the

estimated continuing lease obligations were reduced by estimated

probable sublease rental income.

Duplicate facility included the estimated costs associated

with Arbor’s Troy, Michigan corporate headquarters during

the shutdown period. This facility was considered to be a

duplicate facility that was not required by the combined

company. Immediately after the merger transaction, the Company

assumed all decision-making responsibility for Arbor and Arbor’s

corporate employees.The combined company did not retain these

employees since they were incremental to their CVS counterparts.

During the shutdown period, these employees primarily worked

on shutdown activities.The $16.5 million charge included $1.8

million for the estimated cost of payroll and benefits that would

be incurred in connection with complying with the Federal

In millions

Merger transaction costs $ 15.0

Restructuring costs:

Employee severance and benefits 27.1

Exit costs:

Noncancelable lease obligations 40.0

Duplicate facility 16.5

Asset write-offs 41.2

Contract cancellation costs 4.8

Other 2.7

Total $ 147.3

10

35

2000 Annual Report