Bed, Bath and Beyond 2009 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2009 Bed, Bath and Beyond annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

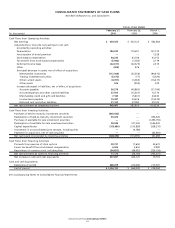

BED BATH & BEYOND 2009 ANNUAL REPORT

23

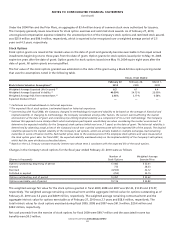

4. LINES OF CREDIT

At February 27, 2010, the Company maintained two uncommitted lines of credit of $100 million each, with expiration dates of

September 3, 2010 and February 28, 2011, respectively. These uncommitted lines of credit are currently and are expected to be

used for letters of credit in the ordinary course of business. During fiscal 2009, the Company did not have any direct borrow-

ings under the uncommitted lines of credit. As of February 27, 2010, there was approximately $6.1 million of outstanding letters

of credit. Although no assurances can be provided, the Company intends to renew both uncommitted lines of credit before the

respective expiration dates. In addition, as of February 27, 2010, the Company maintained unsecured standby letters of credit of

$55.0 million, primarily for certain insurance programs.

At February 28, 2009, the Company maintained two uncommitted lines of credit of $100 million each. These uncommitted lines

of credit were utilized for letters of credit in the ordinary course of business. During fiscal 2008, the Company did not have any

direct borrowings under the uncommitted lines of credit. As of February 28, 2009, there was approximately $7.1 million of out-

standing letters of credit and approximately $45.5 million of outstanding unsecured standby letters of credit, primarily for certain

insurance programs.

5. FAIR VALUE MEASUREMENTS

The Company adopted the accounting guidance related to fair value measurements and disclosures for financial assets and liabili-

ties on March 2, 2008 and for non-financial assets and liabilities on March 1, 2009. This guidance defines fair value, establishes a

framework for measuring fair value in generally accepted accounting principles and expands disclosures about fair value measure-

ments. The adoption of this guidance for financial and non-financial assets and liabilities did not have a material impact on the

Company’s consolidated financial statements.

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability (i.e. “the exit price”) in an

orderly transaction between market participants at the measurement date. In determining fair value, the Company uses various

valuation approaches, including quoted market prices and discounted cash flows. The guidance also established a hierarchy for

inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by

requiring that the most observable inputs be used when available. Observable inputs are inputs that market participants would

use in pricing the asset or liability developed based on market data obtained from independent sources. Unobservable inputs are

inputs that reflect a company’s judgment concerning the assumptions that market participants would use in pricing the asset or

liability developed based on the best information available under the circumstances. The fair value hierarchy is broken down into

three levels based on the reliability of inputs as follows:

•

Level 1 – Valuations based on quoted prices in active markets for identical instruments that the Company is able to access. Since

valuations are based on quoted prices that are readily and regularly available in an active market, valuation of these products

does not entail a significant degree of judgment.

•

Level 2 – Valuations based on quoted prices in active markets for instruments that are similar, or quoted prices in markets that

are not active for identical or similar instruments, and model-derived valuations in which all significant inputs and significant

value drivers are observable in active markets.

•Level 3 – Valuations based on inputs that are unobservable and significant to the overall fair value measurement.

As of February 27, 2010, the Company’s financial assets utilizing Level 1 inputs include long term investment securities traded on

active securities exchanges. The Company did not have any financial assets utilizing Level 2 inputs. Financial assets utilizing Level 3

inputs included short term and long term investments in auction rate securities consisting of preferred shares of closed end munic-

ipal bond funds and securities collateralized by student loans, and a related put option (See “Investment Securities,” Note 6).

To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determina-

tion of fair value requires more judgment. Accordingly, the Company’s degree of judgment exercised in determining fair value is

greatest for instruments categorized in Level 3. In certain cases, the inputs used to measure fair value may fall into different levels

of the fair value hierarchy. In such cases, an asset or liability must be classified in its entirety based on the lowest level of input

that is significant to the measurement of fair value.

Valuation techniques used by the Company must be consistent with at least one of the three possible approaches: the market