Airtran 2007 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2007 Airtran annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

37

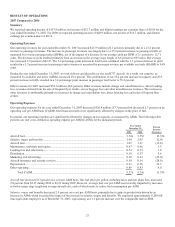

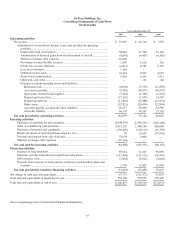

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Market Risk-Sensitive Instruments and Positions

We are subject to certain market risks, including changes in interest rates and commodity prices (i.e., aircraft fuel). The adverse effects

of changes in these markets pose a potential loss as discussed below. The sensitivity analyses do not consider the effects that such

adverse changes may have on overall economic activity, nor do they consider additional actions we may take to mitigate our exposure

to such changes. Actual results may differ. See the Notes to the Consolidated Financial Statements for a description of our financial

accounting policies and additional information.

Interest Rates

We had approximately $764.9 million and $498.9 million of variable-rate debt as of December 31, 2007 and December 31, 2006,

respectively. We have mitigated our exposure on certain variable-rate debt by entering into interest rate swap agreements. These

swaps expire between 2018 and 2019. The notional amount of the outstanding debt related to interest rate swaps at December 31, 2007

was $190.8 million. The interest rate swaps effectively result in us paying a fixed rate of interest on a portion of our floating rate debt

securities through the expiration of the swaps. As of December 31, 2007, the fair market value of our interest rate swaps was a liability

of $4.8 million. If average interest rates increased by 100 basis points during 2008 as compared to 2007, our projected 2008 interest

expense would increase by approximately $7.5 million.

As of December 31, 2007 and 2006, the fair value of our long-term debt was estimated to be $1.063 billion and $857.9 million,

respectively, based upon discounted future cash flows using current incremental borrowing rates for similar types of instruments or

market prices. Market risk on our fixed rate debt, estimated as the potential increase in fair value resulting from a hypothetical 100

basis point decrease in interest rates, was approximately $10.4 million as of December 31, 2007, and approximately $13.4 million as

of December 31, 2006.

Aviation Fuel

Our results of operations can be significantly impacted by changes in the price and availability of aircraft fuel. Aircraft fuel expense

for the years ended 2007 and 2006 represented approximately 37.0 percent and 36.5 percent of our operating expenses, respectively.

Efforts to reduce our exposure to increases in the price and decreases in the availability of aviation fuel include the utilization of fuel

pricing arrangements in purchase contracts with fuel suppliers covering a portion of our anticipated fuel requirements. The fuel pricing

arrangements consist of both fixed price and collar arrangements. Because these contracts are accounted for under the normal

purchase exception included in SFAS 133, these contracts are not considered derivative financial instruments for financial reporting

purposes. As of December 31, 2007, we had no fixed pricing arrangements with fuel suppliers for any future period.

In addition to the fuel purchase contracts discussed above, we have entered into fuel related derivative financial instruments with

financial institutions to reduce the impact of fluctuations in jet-fuel prices on future fuel expense. Our primary objective of entering

into derivative instruments is to reduce the impact on our operating results of the volatility of jet fuel prices. We do not hold or issue

derivative financial instruments for trading purposes. As of December 31, 2007, the fair market value of our fuel related derivative

assets was $13.0 million and was comprised of option and swap arrangements. As of December 31, 2007, these contracts pertain to

70.6 million gallons of our 2008 fuel purchases and 2.0 million gallons of our 2009 fuel purchases and represent 17.9 percent of our

anticipated 2008 jet-fuel requirement and 0.5 percent of our 2009 jet fuel requirements. As of January 23, 2008, we entered into

additional fuel related derivatives, which increase the gallons under contract to 102.1 million gallons and 44.8 million gallons for 2008

and 2009, respectively. This represents 25.8 percent and 10.6 percent of our total 2008 and 2009 anticipated fuel consumption,

respectively.

For every dollar increase per barrel in crude oil or refining costs, our fuel expense for 2008, before the impact of our derivative

financial instruments, would increase $10.0 million based on current and projected operations.