Airtran 2007 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2007 Airtran annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

34

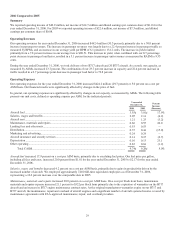

(1) Includes principal and interest payments, forecasted at the current interest rates, on the aforementioned debt of approximately

$1.0 billion. Our debt agreements for aircraft acquisitions generally carry terms of twelve years and are repaid either quarterly or

semiannually.

(2) Amounts include minimum operating leases obligations for aircraft, airport facilities and other leased property. Amounts

exclude contingent payments and aircraft maintenance deposit payments based on flight hours or landings. Lease agreements are

generally for fifteen years on aircraft obligations.

(3) Amounts include payment commitments, including payment of pre-delivery deposits, for aircraft on firm order. Payment

commitments include the forecasted impact of contractual price escalations. As noted under Aircraft Acquisitions and Aircraft

Purchase Commitments, we have arranged pre-delivery deposit financing for a portion of our pre-delivery deposit requirements

for aircraft scheduled to be delivered in 2008, 2009, and some in 2010. The above table does not reflect the effects of such

financings.

(4) Amounts include other contractual commitments. The table does not include payments to be made to third party aircraft

maintenance contractors pursuant to agreements whereby we pay such contractors based on aircraft flight hours or landings. The

table does not include liabilities to vendors, employees and others classified as current liabilities on our December 31, 2007

consolidated balance sheet.

A variety of assumptions are necessary in order to derive the information with respect to contractual commitments described in the

above table, including, but not limited to, the timing of the aircraft delivery dates. Our actual obligations may differ from these

estimates under different assumptions or conditions.

Off-Balance Sheet Arrangements

An off-balance sheet arrangement is any transaction, agreement or other contractual arrangement involving an unconsolidated entity

under which a company has (1) made guarantees, (2) a retained or a contingent interest in transferred assets, (3) an obligation under

derivative instruments classified as equity or (4) any obligation arising out of a material variable interest in an unconsolidated entity

that provides financing, liquidity, market risk or credit risk support to the company, or that engages in leasing, hedging or research and

development arrangements with the company.

We have no arrangements of the types described in the first three categories that we believe may have a material current or future

affect on our financial condition, liquidity or results of operations. Certain guarantees that we do not expect to have a material current

or future effect on our financial condition, liquidity or resulted operations are disclosed in Note 2 to our Consolidated Financial

Statements.

We have variable interests in many of our aircraft leases. The lessors are trusts established specifically to purchase, finance and lease

aircraft to us. These leasing entities meet the criteria of variable interest entities, as defined by Financial Accounting Standards Board

(FASB) Interpretation 46, Consolidation of Variable Interest Entities. We are generally not the primary beneficiary of the leasing

entities if the lease terms are consistent with market terms at the inception of the lease and do not include a residual value guarantee, a

fixed-price purchase option or similar feature that obligates us to absorb decreases in value or entitles us to participate in increases in

the value of the aircraft. This is the case in the majority of our aircraft leases; however, we have two aircraft leases that contain fixed-

price purchase options that allow us to purchase the aircraft at predetermined prices on specified dates during the lease term. We have

not consolidated the related trusts because even taking into consideration these purchase options, we are not the primary beneficiary

based on our cash flow analysis.

Critical Accounting Policies and Estimates

General. The discussion and analysis of our financial condition and results of operations is based upon our Consolidated Financial

Statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The

preparation of these financial statements requires us to make estimates and judgments that affect the reported amount of assets and

liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities at the date of our financial statements.

Our actual results may differ from these estimates under different assumptions or conditions. Critical accounting policies are defined

as those that are reflective of significant judgments and uncertainties, and are sufficiently sensitive to result in materially different

results under different assumptions and conditions. The following is a description of what we believe to be our most critical

accounting policies and estimates. See Notes to the Consolidated Financial Statements for a description of our financial accounting

policies.