Under Armour 2010 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2010 Under Armour annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

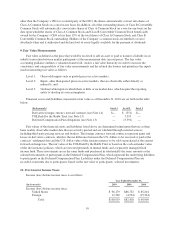

actual future losses from uncollectible accounts may differ from estimates. If the financial condition of customers

were to deteriorate, resulting in their inability to make payments, a larger reserve might be required. In the event

the Company determines a smaller or larger reserve is appropriate, it would record a benefit or charge to selling,

general and administrative expense in the period in which such a determination was made. As of December 31,

2010 and 2009, the allowance for doubtful accounts was $4.9 million and $5.2 million, respectively.

Inventories

Inventories consist of finished goods, raw materials and work-in-process. Costs of finished goods

inventories include all costs incurred to bring inventory to its current condition, including inbound freight, duties

and other costs. The Company values its inventory at standard cost which approximates landed cost, using the

first-in, first-out method of cost determination. Market value is estimated based upon assumptions made about

future demand and retail market conditions. If the Company determines that the estimated market value of its

inventory is less than the carrying value of such inventory, it provides a charge to cost of goods sold to reflect the

lower of cost or market. If actual market conditions are less favorable than those projected by the Company,

further adjustments may be required that would increase the cost of goods sold in the period in which such a

determination was made.

Income Taxes

Income taxes are accounted for under the asset and liability method. Deferred income tax assets and

liabilities are established for temporary differences between the financial reporting basis and the tax basis of the

Company’s assets and liabilities at tax rates expected to be in effect when such assets or liabilities are realized or

settled. Deferred income tax assets are reduced by valuation allowances when necessary.

Assessing whether deferred tax assets are realizable requires significant judgment. The Company considers

all available positive and negative evidence, including historical operating performance and expectations of

future operating performance. The ultimate realization of deferred tax assets is often dependent upon future

taxable income and therefore can be uncertain. To the extent the Company believes it is more likely than not that

all or some portion of the asset will not be realized, valuation allowances are established against the Company’s

deferred tax assets, which increase income tax expense in the period when such a determination is made.

Income taxes include the largest amount of tax benefit for an uncertain tax position that is more likely than

not to be sustained upon audit based on the technical merits of the tax position. Settlements with tax authorities,

the expiration of statutes of limitations for particular tax positions, or obtaining new information on particular tax

positions may cause a change to the effective tax rate. The Company recognizes accrued interest and penalties

related to unrecognized tax benefits in the provision for income taxes on the consolidated statements of income.

Property and Equipment

Property and equipment are stated at cost, including the cost of internal labor for software customized for

internal use, less accumulated depreciation and amortization. Property and equipment is depreciated using the

straight-line method over the estimated useful lives of the assets: 3 to 7 years for furniture, office equipment,

software and plant equipment. Leasehold improvements are amortized over the shorter of the lease term or the

estimated useful lives of the assets. The cost of in-store apparel and footwear fixtures and displays are

capitalized, included in furniture, fixtures and displays, and depreciated over 3 to 5 years.

The Company capitalizes the cost of interest for long term property and equipment projects based on the

Company’s weighted average borrowing rates in place while the projects are in progress. Capitalized interest was

$0.7 million and $0.4 million as of December 31, 2010 and 2009, respectively.

50