Red Lobster 2010 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2010 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

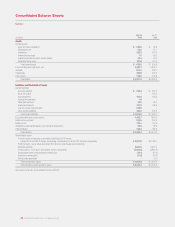

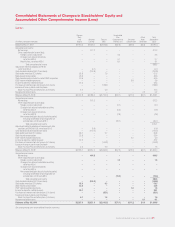

34 DARDEN RESTAURANTS, INC. | 2010 ANNUAL REPORT

Notes to Consolidated Financial Statements

Darden Restaurants

34 DARDEN RESTAURANTS, INC. | 2010 ANNUAL REPORT

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Darden

We use the variance/covariance method to measure value at risk, over

time horizons ranging from one week to one year, at the 95 percent confidence

level. At May 30, 2010, our potential losses in future net earnings resulting

from changes in foreign currency exchange rate instruments, commodity

instruments, equity forwards and floating rate debt interest rate exposures

were approximately $32.8 million over a period of one year (including the

impact of the interest rate swap agreements discussed in Note 10 of the Notes

to Consolidated Financial Statements, included elsewhere in this report). The

value at risk from an increase in the fair value of all of our long-term fixed rate

debt, over a period of one year, was approximately $129.4 million. The fair value

of our long-term fixed rate debt during fiscal 2010 averaged $1.62 billion, with

a high of $1.73 billion and a low of $1.48 billion. Our interest rate risk manage-

ment objective is to limit the impact of interest rate changes on earnings and

cash flows by targeting an appropriate mix of variable and fixed rate debt.

APPLICATION OF NEW ACCOUNTING STANDARDS

We have included reference to previously issued accounting guidance as it

was originally issued with reference to the ASC Topic or Subtopic where the

respective guidance has been codified within the FASB ASC.

In September 2006, the FASB issued SFAS No. 157, “Fair Value

Measurements,” which has been codified into the Fair Value Measurements

and Disclosures Topic (Topic 820) of the FASB ASC. Topic 820 defines fair value,

establishes a framework for measuring fair value and enhances disclosures

about fair value measures required under other accounting pronouncements,

but does not change existing guidance as to whether or not an instrument is

carried at fair value. For financial assets and liabilities, Topic 820 is effective for

fiscal years beginning after November 15, 2007, which required us to adopt

these provisions in fiscal 2009. For nonfinancial assets and liabilities, Topic 820

is effective for fiscal years beginning after November 15, 2008, which required

us to adopt these provisions in fiscal 2010. The adoption of Topic 820 did not

have a significant impact on our consolidated financial statements.

In December 2007, the FASB issued SFAS No. 141R, “Business

Combinations,” which has been codified into the Business Combinations

Topic (Topic 805) of the FASB ASC. Topic 805 provides companies with

principles and requirements on how an acquirer recognizes and measures in

its financial statements the identifiable assets acquired, liabilities assumed,

and any noncontrolling interest in the acquiree as well as the recognition and

measurement of goodwill acquired in a business combination. Topic 850

also requires certain disclosures to enable users of the financial statements

to evaluate the nature and financial effects of the business combination.

Acquisition costs associated with the business combination will generally be

expensed as incurred. The provisions in Topic 805 are effective for business

combinations occurring in fiscal years beginning after December 15, 2008,

which required us to adopt these provisions for business combinations

occurring in fiscal 2010 and thereafter. This guidance was adopted at the

beginning of fiscal 2010 and will be implemented for any future business

combinations. The adoption did not have a significant impact on our

consolidated financial statements.

In June 2008, the FASB issued FASB Staff Position (FSP) EITF 03-6-1,

“Determining Whether Instruments Granted in Share-Based Payment

Transactions Are Participating Securities,” which has been codified into the

Earnings Per Share Topic of the FASB ASC, within Subtopic 260-10. Subtopic

260-10 provides that unvested share-based payment awards that contain

nonforfeitable rights to dividends or dividend equivalents (whether paid or

unpaid) are participating securities and shall be included in the computation

of earnings per share pursuant to the two-class method. The two-class

method is an earnings allocation method for computing earnings per share

when an entity’s capital structure includes either two or more classes of

common stock or common stock and participating securities. It determines

earnings per share based on dividends declared on common stock and

participating securities (i.e., distributed earnings) and participation rights

of participating securities in any undistributed earnings. This guidance is

effective for fiscal years beginning after December 15, 2008, which required

us to adopt these provisions in fiscal 2010. The adoption of this guidance did

not have a significant impact on our consolidated financial statements.

In December 2008, the FASB issued FSP 132(R)-1, “Employers’

Disclosures about Postretirement Benefit Plan Assets,” which expands the

disclosure requirements about fair value measurements of plan assets for

pension plans, postretirement medical plans, and other funded postretirement

plans. This guidance has been incorporated into the Compensation-Retirement

Benefits Topic of the FASB ASC (Topic 715) and is effective for fiscal years

ending after December 15, 2009, which required us to adopt these provisions

during the fourth quarter of fiscal 2010. The additional disclosures are included

in Note 17 of the notes to the consolidated financial statements included

elsewhere in this report and incorporated herein by reference.

In April 2009, the FASB issued FSP SFAS No. 107-1 and Accounting

Principles Board (APB) Opinion No. 28-1, “Interim Disclosures about Fair Value

of Financial Instruments,” which amends SFAS No. 107, “Disclosures about

Fair Value of Financial Instruments” and APB Opinion No. 28, “Interim Financial

Reporting,” to require disclosures about the fair value of instruments for interim

reporting periods. This FSP has been codified into the Financial Instruments

Topic of the FASB ASC, within Subtopic 825-10. This guidance is effective for

interim reporting periods ending after June 15, 2009, which required us to

adopt these provisions during the first quarter of fiscal 2010.

In May 2009, the FASB issued SFAS No. 165, “Subsequent Events,” which

has been incorporated into the Subsequent Events Topic of the FASB ASC,

within Subtopic 855-10. Subtopic 855-10 establishes general standards

of accounting for and disclosing events that occur after the balance sheet

date but before financial statements are issued or are available to be issued.

This guidance is effective for interim and annual periods ending after

June 15, 2009, which required that we adopt these provisions in the first

fiscal quarter of 2010. In February 2010, the FASB issued ASU 2010-09,

“SubsequentEvents(Topic855)–AmendmentstoCertainRecognitionand

Disclosure Requirements.” This update removes the definition of a public

entity from the ASC and amends disclosure requirements by only requiring

those entities that do not file or furnish financial statements with the SEC to

disclose the date through which subsequent events have been evaluated.

In July 2009, the FASB issued SFAS No. 168, “FASB Accounting Standards

Codification,” as the single source of authoritative nongovernmental U.S.

GAAP. As a result, all existing accounting standard documents have been

superseded. All other accounting literature not included in the ASC will be

considered non-authoritative. The ASC did not change GAAP but instead

combined all authoritative guidance into a comprehensive, topically organized

structure. Upon adoption of the ASC, this statement is now codified in FASB

ASC Topic 105, “Generally Accepted Accounting Principles.” This statement

is effective for interim and annual periods ending after September 15, 2009,

which required us to adopt this statement during the second fiscal quarter of

2010. The adoption of this Statement did not impact the consolidated financial