Red Lobster 2010 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2010 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

32 DARDEN RESTAURANTS, INC. | 2010 ANNUAL REPORT

Notes to Consolidated Financial Statements

Darden Restaurants

32 DARDEN RESTAURANTS, INC. | 2010 ANNUAL REPORT

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Darden

Our fixed-charge coverage ratio, which measures the number of times

each year that we earn enough to cover our fixed charges, amounted to 4.7

times and 4.2 times, on a continuing operations basis, for the fiscal years ended

May 30, 2010 and May 31, 2009, respectively. Our adjusted debt to adjusted

total capital ratio (which includes 6.25 times the total annual minimum rent of

$120.8 million and $114.1 million for the fiscal years ended May 30, 2010 and

May 31, 2009, respectively, as components of adjusted debt and adjusted total

capital) was 57 percent and 62 percent at May 30, 2010 and May 31, 2009,

respectively. We include the lease-debt equivalent and contractual guarantees

in our adjusted debt to adjusted total capital ratio reported to shareholders, as

we believe its inclusion better represents the optimal capital structure that we

target from period to period and because it is consistent with the calculation of

the covenant under our Revolving Credit Agreement.

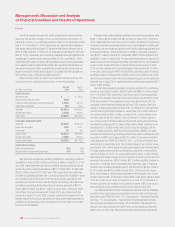

Based on these ratios, we believe our financial condition is strong. The

composition of our capital structure is shown in the following table.

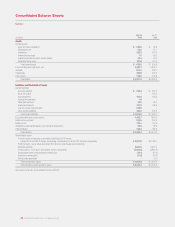

May 30, May 31,

(In millions, except ratios)

2010 2009

Capital Structure

Short-term debt $ – $ 150.0

Current portion long-term debt 225.0–

Long-term debt, excluding unamortized discounts 1,413.6 1,637.9

Capital lease obligations 58.9 60.0

Total debt $1,697.5 $1,847.9

Stockholders’ equity 1,894.0 1,606.0

Total capital $3,591.5 $3,453.9

Calculation of Adjusted Capital

Total debt $1,697.5 $1,847.9

Lease-debt equivalent 755.0 713.1

Guarantees 9.0 8.8

Adjusted debt $2,461.5 $2,569.8

Stockholders’ equity 1,894.0 1,606.0

Adjusted total capital $4,355.5 $4,175.8

Capital Structure Ratios

Debt to total capital ratio 47% 54%

Adjusted debt to adjusted total capital ratio 57% 62%

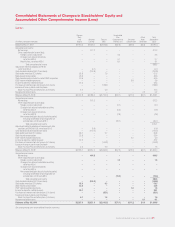

Net cash flows provided by operating activities from continuing operations

were $903.4 million, $783.5 million and $766.8 million in fiscal 2010, 2009

and 2008, respectively. Net cash flows provided by operating activities include

net earnings from continuing operations of $407.0 million, $371.8 million and

$369.5 million in fiscal 2010, 2009 and 2008, respectively. Net cash flows

provided by operating activities from continuing operations increased in fiscal

2010 primarily due to the impact of the timing of inventory purchases and

overall product demand, lower costs and higher net earnings. Net cash flows

provided by operating activities also reflect income tax payments of $94.8

mil lion, $64.4 million and $119.7 million in fiscal 2010, 2009 and 2008,

respectively. The lower tax payments in fiscal 2009, as compared with tax

payments in fiscal 2010 and 2008, primarily relates to the recognition of tax

benefits related to the timing of deductions for fixed asset related expenditures,

in addition to the application of the overpayment of income taxes in prior years

to fiscal 2009 tax liabilities.

Net cash flows used in investing activities from continuing operations were

$428.7 million, $562.4 million and $1.62 billion in fiscal 2010, 2009 and

2008, respectively. Net cash flows used in investing activities from continuing

operations included capital expenditures incurred principally for building new

restaurants, our new restaurant support center facility, replacing equipment and

technology initiatives. Capital expenditures related to continuing operations

were $432.1 million in fiscal 2010, compared to $535.3 million in fiscal 2009

and $429.2 million in fiscal 2008. The decreased expenditures in fiscal 2010

resulted primarily from decreased spending associated with our new restaurant

support center facility which was completed in the second quarter of fiscal

2010, and the replacement of restaurant assets. Excluding the $1.20 billion

in net cash used to acquire RARE in fiscal 2008, cash flows used in investing

activities increased in fiscal 2009, primarily due to an increase in new restau-

rant activity and construction of our new restaurant support center facility. We

estimate that our fiscal 2011 capital expenditures will be approximately $475

million to $525 million.

Net cash flows (used in) provided by financing activities from continuing

operations were ($290.0) million, ($204.8) million and $805.5 million in fiscal

2010, 2009 and 2008, respectively. Cash flows used in financing activities

for fiscal 2010 exceeded the cash flows used in financing activities for fiscal

2009 due primarily to the repayment of short-term debt in fiscal 2010 as

compared to short-term borrowings during fiscal 2009, partially offset by a

reduction in shares repurchased in fiscal 2010. For fiscal 2010, net cash flows

used in financing activities included our repurchase of 2.0 million shares of

our common stock for $85.1 million, compared to 5.1 million shares of our

common stock for $144.9 million in fiscal 2009 and 5.0 million shares of

our common stock for $159.4 million in fiscal 2008. During fiscal 2008 we

completed the offering of $1.15 billion of New Senior Notes, resulting in net

proceeds of $1.13 billion, which were used to repay borrowings under an

interim credit agreement, which funded the acquisition of RARE. Proceeds

received from the Revolving Credit Agreement were used to partially fund the

acquisition of RARE and to repay the $125.0 million 2.5 percent convertible

notes assumed from RARE. As of May 30, 2010, our Board of Directors had

authorized us to repurchase up to 162.4 million shares of our common stock

and a total of 154.1 million shares had been repurchased under the authorization.

The repurchased common stock is reflected as a reduction of stockholders’

equity. As of May 30, 2010, our unused authorization was 8.3 million shares.

We received proceeds primarily from the issuance of common stock upon the

exercise of stock options of $66.3 million, $57.5 million and $66.8 million in

fiscal 2010, 2009 and 2008, respectively. Net cash flows used in financing

activities also included dividends paid to stockholders of $140.0 million,

$110.2 million and $100.9 million in fiscal 2010, 2009 and 2008, respec-

tively. The increase in dividend payments reflects the increase in our annual

dividend rate from $0.72 per share in fiscal 2008, to $0.80 per share in fiscal

2009 and to $1.00 per share in fiscal 2010. In June 2010, the Board of

Directors approved an increase in the quarterly dividend to $0.32 per share,

which indicates an annual dividend of $1.28 per share in fiscal 2011.

Our defined benefit and other postretirement benefit costs and liabilities

are determined using various actuarial assumptions and methodologies

prescribedunderFASBASCTopic715,Compensation–RetirementBenefits

andTopic712,Compensation–NonretirementPostemploymentBenefits.

We use certain assumptions including, but not limited to, the selection of a

discount rate, expected long-term rate of return on plan assets and expected

health care cost trend rates. We set the discount rate assumption annually for