Pfizer 2006 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2006 Pfizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

28 2006 Financial Report

Financial Review

Pfizer Inc and Subsidiary Companies

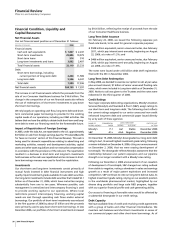

Financial Condition, Liquidity and

Capital Resources

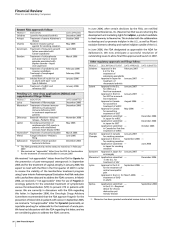

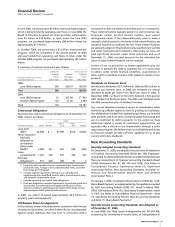

Net Financial Assets

Our net financial asset position as of December 31 follows:

(MILLIONS OF DOLLARS) 2006 2005

Financial assets:

Cash and cash equivalents $ 1,827 $ 2,247

Short-term investments 25,886 19,979

Short-term loans 514 510

Long-term investments and loans 3,892 2,497

Total financial assets 32,119 25,233

Debt:

Short-term borrowings, including

current portion of long-term debt 2,434 11,589

Long-term debt 5,546 6,347

Total debt 7,980 17,936

Net financial assets $24,139 $ 7,297

The increase in net financial assets reflects the proceeds from the

sale of our Consumer Healthcare business for $16.6 billion. The

change in the composition of our net financial assets also reflects

the use of redemptions of short-term investments to pay down

short-term borrowings.

We rely largely on operating cash flow, long-term debt and short-

term commercial paper borrowings to provide for the working

capital needs of our operations, including our R&D activities. We

believe that we have the ability to obtain both short-term and long-

term debt to meet our financing needs for the foreseeable future.

Impact of Repatriation of Foreign Earnings

In 2005, under the Jobs Act, we repatriated to the U.S. approximately

$37 billion in cash from foreign earnings (see the “Provision/(Benefit)

for Taxes on Income” section of this Financial Review). This cash is

being used for domestic expenditures relating to advertising and

marketing activities, research and development activities, capital

assets and other asset acquisitions and non-executive compensation

in accordance with the provisions of the Jobs Act. The repatriation

resulted in a decrease in short-term and long-term investments

held overseas as the cash was repatriated and an increase in short-

term borrowings overseas was used to fund the repatriation.

Investments

Our short-term and long-term investments consist primarily of

mutual funds invested in debt financial instruments and high

quality, liquid investment-grade available-for-sale debt securities.

Our long-term investments include debt securities that totaled $2.1

billion as of December 31, 2006, which have maturities ranging

substantially from one to ten years. Wherever possible, cash

management is centralized and intercompany financing is used

to provide working capital to our operations. Where local

restrictions prevent intercompany financing, working capital

needs are met through operating cash flows and/or external

borrowings. Our portfolio of short-term investments was reduced

in the first quarter of 2006 by about $7 billion and the proceeds

were primarily used to pay down short-term borrowings. In late

December 2006, our portfolio of short-term investments increased

by $16.6 billion, reflecting the receipt of proceeds from the sale

of our Consumer Healthcare business.

Long-Term Debt Issuance

On February 22, 2006, we issued the following Japanese yen

fixed-rate bonds, to be used for general corporate purposes:

•

$508 million equivalent, senior unsecured notes, due February

2011, which pay interest semi-annually, beginning on August

22, 2006, at a rate of 1.2%; and

•

$466 million equivalent, senior unsecured notes, due February

2016, which pay interest semi-annually, beginning on August

22, 2006, at a rate of 1.8%.

The notes were issued under a $5 billion debt shelf registration

filed with the SEC in November 2002.

Long-Term Debt Redemption

In May 2006, we decided to exercise our option to call, at par-value

plus accrued interest, $1 billion of senior unsecured floating-rate

notes, which were included in Long-term debt as of December 31,

2005. Notice to call was given to the Trustees and the notes were

redeemed in the third quarter of 2006.

Credit Ratings

Two major corporate debt-rating organizations, Moody’s Investors

Services (Moody’s) and Standard & Poor’s (S&P), assign ratings to

our short-term and long-term debt. The following chart reflects

the current ratings assigned to our senior unsecured non-credit

enhanced long-term debt and commercial paper issued directly

by us by each of these agencies:

NAME OF COMMERCIAL

LONG-TERM DEBT

DATE OF LAST______________________

RATING AGENCY PAPER RATING OUTLOOK ACTION

Moody’s P-1 Aa1 Stable December 2006

S&P A1+ AAA Negative December 2006

On December 19, 2006, Moody’s downgraded our long-term debt

rating to Aa1, its second highest investment grade rating, following

a review initiated on December 4, 2006, citing our announcement

on December 2, 2006, that we were ceasing development of

torcetrapib. The downgrade reflects Moody’s assessment that the

relationship between our patent exposures and our pipeline

strength is no longer consistent with a Moody’s Aaa rating.

Following our December 2, 2006 announcement of our cessation

of development of torcetrapib, S&P changed our rating outlook

from stable to negative, noting a slowdown in sales and earnings

growth as a result of major patent expirations and increased

competition. S&P continues to rate our long-term debt at AAA, its

highest investment grade rating, relying on our excellent position

in the worldwide pharmaceutical market, highlighted by our

diverse drug portfolio and large scale R&D program, together

with our superior financial profile and cash-generating ability.

Our access to financing at favorable rates would be affected by

a substantial downgrade in our credit ratings.

Debt Capacity

We have available lines of credit and revolving-credit agreements

with a group of banks and other financial intermediaries. We

maintain cash balances and short-term investments in excess of

our commercial paper and other short-term borrowings. As of