Pfizer 2006 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2006 Pfizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

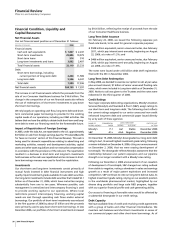

26 2006 Financial Report

Financial Review

Pfizer Inc and Subsidiary Companies

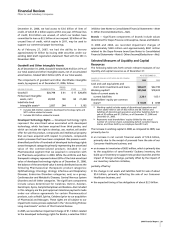

Acquisition-Related Costs

Adjusted income is calculated prior to considering integration and

restructuring charges associated with business combinations

because these costs are unique to each transaction and represent

costs that were incurred to restructure and integrate two

businesses as a result of the acquisition decision. For additional

clarity, only restructuring and integration activities that are

associated with a purchase business combination or a net-asset

acquisition are included in acquisition-related costs. We have not

factored in the impacts of synergies that would have resulted had

these costs not been incurred.

We believe that viewing income prior to considering these charges

provides investors with a useful additional perspective because the

significant costs incurred in a business combination result primarily

from the need to eliminate duplicate assets, activities or

employees—a natural result of acquiring a fully integrated set of

activities. For this reason, we believe that the costs incurred to

convert disparate systems, to close duplicative facilities or to

eliminate duplicate positions (for example, in the context of a

business combination) can be viewed differently from those costs

incurred in other, more normal business contexts.

The integration and restructuring charges associated with a

business combination may occur over several years, with the

more significant impacts ending within three years of the

transaction. Because of the need for certain external approvals for

some actions, the span of time needed to achieve certain

restructuring and integration activities can be lengthy. For

example, due to the highly regulated nature of the pharmaceutical

business, the closure of excess facilities can take several years, as

all manufacturing changes are subject to extensive validation

and testing and must be approved by the FDA. In other situations,

we may be required by local laws to obtain approvals prior to

terminating certain employees. This approval process can delay

the termination action.

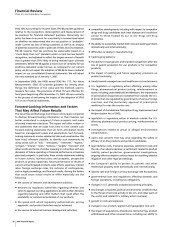

Discontinued Operations

Adjusted income is calculated prior to considering the results of

operations included in discontinued operations, such as our

Consumer Healthcare business, which we sold in December 2006,

as well as any related gains or losses on the sale of such operations.

We believe that this presentation is meaningful to investors

because, while we review our businesses and product lines

periodically for strategic fit with our operations, we do not build

or run our businesses with an intent to sell them.

Cumulative Effect of a Change in Accounting Principles

Adjusted income is calculated prior to considering the cumulative

effect of a change in accounting principles. The cumulative effect

of a change in accounting principles is generally one time in

nature and not expected to occur as part of our normal business

on a regular basis.

Certain Significant Items

Adjusted income is calculated prior to considering certain

significant items. Certain significant items represent substantive,

unusual items that are evaluated on an individual basis. Such

evaluation considers both the quantitative and the qualitative

aspect of their unusual nature. Unusual, in this context, may

represent items that are not part of our ongoing business; items

that, either as a result of their nature or size, we would not

expect to occur as part of our normal business on a regular basis;

items that would be non-recurring; or items that relate to products

we no longer sell. While not all-inclusive, examples of items that

could be included as certain significant items would be a major

non-acquisition-related restructuring charge and associated

implementation costs for a program which is specific in nature with

a defined term, such as those related to our AtS initiative; costs

associated with a significant recall of one of our products; charges

related to sales or disposals of products or facilities that do not

qualify as discontinued operations as defined by U.S. GAAP;

certain intangible asset impairments; adjustments related to the

resolution of certain tax positions; the impact of adopting certain

significant, event-driven tax legislation, such as charges

attributable to the repatriation of foreign earnings in accordance

with the Jobs Act; or possible charges related to legal matters, such

as certain of those discussed in Legal Proceedings in our Form

10-K and in Part II: Other Information; Item 1, Legal Proceedings

included in our Form 10-Q filings. Normal, ongoing defense costs

of the Company or settlements and accruals on legal matters

made in the normal course of our business would not be

considered certain significant items.

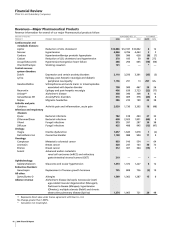

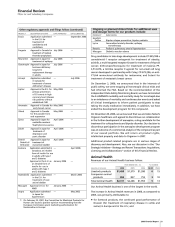

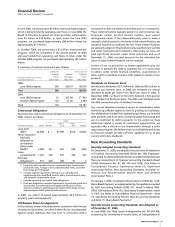

Reconciliation

A reconciliation between Net income, as reported under U.S.

GAAP, and Adjusted income follows:

YEAR ENDED DEC. 31, % CHANGE

__________________________________________ _________________

(MILLIONS OF DOLLARS) 2006 2005 2004 06/05 05/04

Reported net income $19,337 $ 8,085 $11,361 139 (29)

Purchase accounting

adjustments—

net of tax 3,131 3,967 3,389 (21) 17

Acquisition-related

costs—net of tax 14 599 744 (98) (19)

Discontinued

operations—

net of tax (8,313) (498) (425) M+ 17

Cumulative effect of

a change in

accounting

principles—

net of tax — 23 — * *

Certain significant

items—net of tax 813 2,293 629 (65) 265

Adjusted income $14,982 $14,469 $15,698 4 (8)

* Calculation not meaningful.

M+ Change greater than 1,000%.

Certain amounts and percentages may reflect rounding adjustments.