Pfizer 2006 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2006 Pfizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

•

A significant adverse change in legal factors or in the business

climate that could affect the value of the asset. For example,

a successful challenge of our patent rights resulting in generic

competition earlier than expected.

•

A significant adverse change in the extent or manner in which

an asset is used. For example, restrictions imposed by the FDA

or other regulatory authorities that affect our ability to

manufacture or sell a product.

•

A projection or forecast that demonstrates losses associated with

an asset. This could include, for example, a change in a

government reimbursement program that results in an inability

to sustain projected product revenues and profitability. This also

could include the introduction of a competitor’s product that

results in a significant loss of market share.

Our impairment review process is as follows:

•

For finite-lived intangible assets, such as developed technology

rights, whenever impairment indicators are present, we perform

an in-depth review for impairment. We calculate the

undiscounted value of the projected cash flows associated with

the asset and compare this estimated amount to the carrying

amount of the asset. If the carrying amount is found to be

greater, we record an impairment loss for the excess of book

value over the asset’s fair value. Fair value is generally calculated

by applying an appropriate discount rate to the undiscounted

cash flow projections to arrive at net present value. In addition,

in all cases of an impairment review, we reevaluate the

remaining useful life of the asset and modify it, as appropriate.

•

For indefinite-lived intangible assets, such as brands, each year and

whenever impairment indicators are present, we calculate the fair

value of the asset and record an impairment loss for the excess of

book value over fair value, if any. Fair value is generally measured

as the net present value of projected cash flows. In addition, in

all cases of an impairment review, we reevaluate the remaining

useful life of the asset and determine whether continuing to

characterize the asset as indefinite-lived is appropriate.

•

For Goodwill, which includes amounts related to our

Pharmaceutical and Animal Health segments each year and

whenever impairment indicators are present, we calculate the

fair value of each business segment and calculate the implied

fair value of goodwill by subtracting the fair value of all the

identifiable net assets other than goodwill and record an

impairment loss for the excess of book value of goodwill over

the implied fair value, if any.

•

For other long-lived assets, such as property, plant and

equipment, we apply procedures similar to those for finite-lived

intangible assets to determine if an asset is impaired. Long-term

investments and loans are subject to periodic impairment

reviews and whenever impairment indicators are present. For

these assets, fair value is typically determined by observable

market quotes or the expected present value of future cash

flows. When necessary, we record charges for impairments of

long-lived assets for the amount by which the fair value is less

than the carrying value of these assets.

•

For non-current deferred tax assets, we provide a valuation

allowance when we believe that the assets are not probable of

recovery based on an assessment of estimated future taxable

income that incorporates ongoing, prudent, feasible tax-

planning strategies.

The value of intangible assets is determined primarily using

the “income method,” which starts with a forecast of all the

expected future net cash flows (see the “Our Strategic Initiatives—

Strategy and Recent Transactions: Acquisitions, Licensing and

Collaborations,” section of this Financial Review above).

Accordingly, the potential for impairment for these intangible

assets may exist if actual revenues are significantly less than those

initially forecasted or actual expenses are significantly more than

those initially forecasted. Some of the more significant estimates

and assumptions inherent in the intangible asset impairment

estimation process include: the amount and timing of projected

future cash flows; the discount rate selected to measure the risks

inherent in the future cash flows; and the assessment of the

asset’s life cycle and the competitive trends impacting the asset,

including consideration of any technical, legal, regulatory, or

economic barriers to entry as well as expected changes in

standards of practice for indications addressed by the asset.

The implied fair value of goodwill is determined by first estimating

the fair value of the associated business segment. To estimate the

fair value of each business segment, we generally use the “market

approach,” where we compare the segment to similar businesses

or “guideline” companies whose securities are actively traded in

public markets or which have recently been sold in a private

transaction. We may also use the “income approach,” where we

use a discounted cash flow model in which cash flows anticipated

over several periods, plus a terminal value at the end of that time

horizon, are discounted to their present value using an

appropriate rate of return. Some of the more significant estimates

and assumptions inherent in the goodwill impairment estimation

process using the “market approach” include: the selection of

appropriate guideline companies; the determination of market

value multiples for the guideline companies and the subsequent

selection of an appropriate market value multiple for the business

segment based on a comparison of the business segment to the

guideline companies; and the determination of applicable

premiums and discounts based on any differences in ownership

percentages, ownership rights, business ownership forms, or

marketability between the segment and the guideline companies;

and/or knowledge of the terms and conditions of comparable

transactions. When considering the “income approach,” we

include: the required rate of return used in the discounted cash

flow method, which reflects capital market conditions and the

specific risks associated with the business segment. Other estimates

inherent in the “income approach” include long-term growth rates

and cash flow forecasts for the business segment.

A single estimate of fair value results from a complex series of

judgments about future events and uncertainties and relies heavily

on estimates and assumptions (see “Estimates and Assumptions”

above). The judgments made in determining an estimate of fair value

can materially impact our results of operations. As such, for significant

items, we often obtain assistance from third-party valuation

specialists. The valuations are based on information available as of

the impairment review date and are based on expectations and

assumptions that have been deemed reasonable by management.

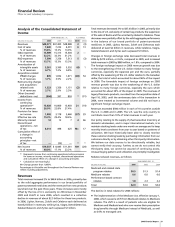

2006 Financial Report 11

Financial Review

Pfizer Inc and Subsidiary Companies