Office Depot 2000 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2000 Office Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

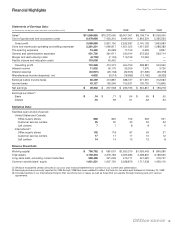

23

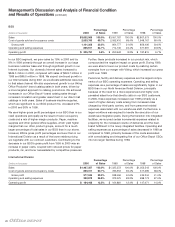

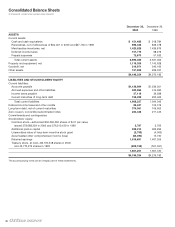

Office Depot, Inc. and Subsidiaries

us to finance a portion of our inventory. We generally offer credit

terms, under which we carry our own receivables, to our con-

tract and certain of our direct mail customers. As we expand

our contract and direct mail businesses, we anticipate that our

accounts receivable portfolio will continue to grow. Amounts

due for rebate, cooperative advertising and marketing programs

with our vendors comprise a significant percentage of our total

receivables. These receivables tend to fluctuate seasonally

(growing during the second half of the year and declining during

the first half), because certain collections do not happen until

after an entire program year has been completed.

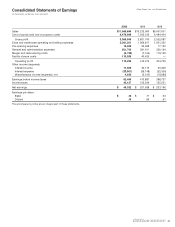

The decline in operating cash flows in 2000 is primarily attrib-

utable to lower gross profit and higher store and warehouse

operating and selling expenses and general and administrative

expenses, which is more fully explained in Results of Opera-

tions. In 1999, the decrease in operating cash flows from 1998

was due mainly to our aggressive store opening program. On

a worldwide basis in 1999, excluding joint venture operations

and licensing arrangements, we opened 159 stores, including

relocations of older stores, as compared to 106 openings

during 1998. Opening a new domestic store requires that we

outlay approximately $0.5 million in cash for the portion of

our inventories that is not financed by our vendors, as well as

approximately $0.2 million for pre-opening expenses (see

Pre-opening Expenses). Our focus on supply chain manage-

ment helped boost our 1998 operating cash flows by reducing

inventories by $139 million. This focus continued to reduce the

average inventory balances held in stores and CSCs in 1999

and 2000; however, this benefit was offset by increases resulting

from stocking our new stores with inventories. Incremental Y2K-

related purchases further impacted our inventory levels in 1999.

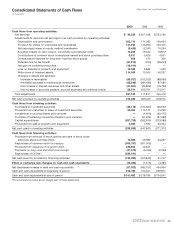

Our primary investing activity is the acquisition of capital assets.

The number of stores and CSCs we open or remodel each year

generally drives the volume of our capital investments. Over the

past three years, we opened 78, 159 and 106 stores during

2000, 1999 and 1998, respectively. This accounts for the majority

of the variation in our investing activities over the years. During

2000, we also had significant expenditures related to our Viking

integration plans. In 1999, computer and other equipment pur-

chases at our corporate offices and at our facilities, necessary

to complete Y2K remediation, relocation of our corporate data

center, and support for our store expansion, also contributed to

our increased cash investing needs.

We currently plan to open approximately 50 stores in our North

American Retail Division and numerous stores in our International

Division during 2001. We also plan to relocate several existing

warehouses, and open two additional warehouses in our

International Division. We estimate that our cash investing

requirements will be approximately $1.1 million for each new

domestic office supply store. The $1.1 million includes approxi-

mately $0.6 million for leasehold improvements, fixtures, point-

of-sale terminals and other equipment, and approximately $0.5

million for the portion of our inventories that will not be financed

by our vendors. In addition, our average new office supply store

requires pre-opening expenses of approximately $0.2 million.

The investment required for a new CSC is significantly more

than the amounts required for a new store. Each new domestic

and international CSC requires between $6 to $16 million for

capital assets and inventory, and pre-opening expenses of up

to $1.8 million, depending on the size, type and location of the

facility. Also in 2001, we plan on spending approximately $40

million in capital investments related to re-merchandising and

remodeling our store locations and consolidating and upgrading

our call centers.

We have expanded our presence in the electronic commerce

marketplace by entering into strategic business relationships

with several Web-based providers of business-to-business

electronic commerce solutions. We made equity investments in

these companies during 2000 and 1999 of $30.1 and $50.7 million,

respectively. During 2000, we sold certain of these investments

for $57.9 million. Also, because of the recent decline in the mar-

ket for Internet related companies, we performed an extensive

valuation of each of our remaining investments at the end of

2000. This resulted in a write down of $45.5 million, reducing

the current book value of the investments at December 30, 2000

to $29.9 million. We continue to believe the Internet represents

an exciting opportunity for our products and services, and we

will continue to look for opportunities to invest in companies

that provide business-to-business e-commerce solutions for

small- and medium-sized businesses.

Financing Activities

Our domestic credit facilities provide us with a maximum of

$600.0 million in funds. These facilities consist of two separate

credit agreements, a five-year loan providing us with a working

capital line and letters of credit capacity totaling $300.0 million,

and a 364-day loan for working capital also totaling $300.0 mil-

lion. As of December 30, 2000, we had outstanding borrowings

of $389.6 million under these lines of credit, as well as letters of

credit totaling $49.5 million. Our five-year agreement was entered

into in February 1998 and has various borrowing rate options,

including a rate based on our credit rating that currently would

result in an interest rate of 0.475% over the London Interbank

Offered Rate (“LIBOR”). In June 2000, we entered into a second

credit agreement with a 364-day term, which also has various

borrowing rate options, including a current borrowing rate of

0.500% over LIBOR. At December 30, 2000, the average

effective interest rates were 7.001% and 7.996% for the five-

year and 364-day facilities, respectively. Both agreements

contain similar restrictive covenants relating to various financial

statement ratios.