Mattel 2015 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2015 Mattel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

|

|

36

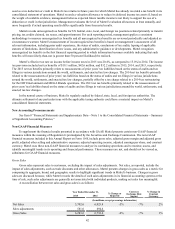

contributions by Mattel. The Plan allows employees to allocate both their voluntary contributions and their employer automatic

and matching contributions to a variety of investment funds, including a fund that is invested in Mattel common stock (the

“Mattel Stock Fund”). Employees are not required to allocate any of their Plan account balance to the Mattel Stock Fund,

allowing employees to limit or eliminate their exposure to market changes in Mattel’s stock price. Furthermore, the Plan limits

the percentage of the employee’s total account balance that may be allocated to the Mattel Stock Fund to 25%. Employees may

generally reallocate their account balances on a daily basis. However, pursuant to Mattel’s insider trading policy, employees

classified as insiders and restricted personnel under Mattel’s insider trading policy are limited to certain periods in which they

may make allocations into or out of the Mattel Stock Fund.

Application of Critical Accounting Policies and Estimates

Mattel makes certain estimates and assumptions that affect the reported amounts of assets and liabilities and the reported

amounts of revenues and expenses. The accounting policies and estimates described below are those Mattel considers most

critical in preparing its consolidated financial statements. Management has discussed the development and selection of these

critical accounting policies and estimates with the Audit Committee of its Board of Directors, and the Audit Committee has

reviewed the disclosures included below. These accounting policies and estimates include significant judgments made by

management using information available at the time the estimates are made. As described below, however, these estimates

could change materially if different information or assumptions were used instead.

For a summary of Mattel’s significant accounting policies, estimates, and methods used in the preparation of Mattel’s

consolidated financial statements, see Item 8 “Financial Statements and Supplementary Data—Note 1 to the Consolidated

Financial Statements—Summary of Significant Accounting Policies.” In most instances, Mattel must use an accounting policy

or method because it is the only policy or method permitted under accounting principles generally accepted in the United States

of America (“US GAAP”).

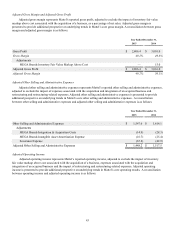

Accounts Receivable—Allowance for Doubtful Accounts

The allowance for doubtful accounts represents adjustments to customer trade accounts receivable for amounts deemed

partially or entirely uncollectible. Management believes the accounting estimate related to the allowance for doubtful accounts

is a “critical accounting estimate” because significant changes in the assumptions used to develop the estimate could materially

affect key financial measures, including other selling and administrative expenses, net income, and accounts receivable. In

addition, the allowance requires a high degree of judgment since it involves estimation of the impact of both current and future

economic factors in relation to its customers’ ability to pay amounts owed to Mattel.

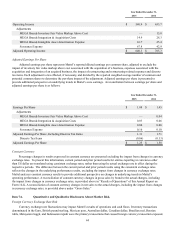

Mattel’s products are sold throughout the world. Products within the North America segment are sold directly to retailers,

including discount and free-standing toy stores, chain stores, department stores, other retail outlets and, to a limited extent,

wholesalers, and directly to consumers. Products within the International segment are sold directly to retailers and wholesalers

in most European, Latin American, and Asian countries, and in Australia and New Zealand, and through agents and distributors

in those countries where Mattel has no direct presence.

In recent years, the mass-market retail channel has experienced significant shifts in market share among competitors,

causing some large retailers to experience liquidity problems. Mattel’s sales to customers are typically made on credit without

collateral and are highly concentrated in the third and fourth quarters due to the seasonal nature of toy sales, which results in a

substantial portion of trade receivables being collected during the latter half of the year and the first quarter of the following

year. There is a risk that customers will not pay, or that payment may be delayed, because of bankruptcy or other factors

beyond the control of Mattel. This could increase Mattel’s exposure to losses from bad debts.

A small number of customers account for a large share of Mattel’s net sales and accounts receivable. In 2015, Mattel’s

three largest customers, Wal-Mart, Toys “R” Us, and Target, in the aggregate, accounted for approximately 37% of net sales,

and its ten largest customers, in the aggregate, accounted for approximately 48% of net sales. As of December 31, 2015,

Mattel’s three largest customers accounted for approximately 34% of net accounts receivable, and its ten largest customers

accounted for approximately 47% of net accounts receivable. The concentration of Mattel’s business with a relatively small

number of customers may expose Mattel to a material adverse effect if one or more of Mattel’s large customers were to

experience financial difficulty.

Mattel has procedures to mitigate its risk of exposure to losses from bad debts. Revenue is recognized upon shipment or

upon receipt of products by the customer, depending on the terms, provided that: there are no uncertainties regarding customer

acceptance; persuasive evidence of an agreement exists documenting the specific terms of the transaction; the sales price is

fixed or determinable; and collectibility is reasonably assured. Value added taxes are recorded on a net basis and are excluded

from revenue. Credit limits and payment terms are established based on the underlying criteria that collectibility must be

reasonably assured at the levels set for each customer. Extensive evaluations are performed on an ongoing basis throughout the