JP Morgan Chase 2015 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2015 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

1313

tive credit losses were for all banks during

the Great Recession (they were 5.6%), and

our credit book today is materially better

than what we had at that time. The 2015

CCAR losses were even with the actual losses

for banks during the worst two years of the

Great Depression in the 1930s (6.4%).

The stress test is extremely severe on trading and

counterparty risk.

Our 2015 CCAR trading and counterparty

losses were $24 billion. We have two compar-

isons that should give comfort that our losses

would never be this large.

First, recall what actually happened to us in

2008. In the worst quarter of 2008, we lost

$1.7 billion; for the entire year, we made $6.3

billion in trading revenue in the Investment

Bank, which included some modest losses

on the Lehman default (one of our largest

counterparties). The trading books are much

more conservative today than they were in

2008, and at that time, we were still paying

a considerable cost for assimilating and

de-risking Bear Stearns.

Second, we run hundreds of stress tests

of our own each week, across our global

trading operations, to ensure our ability

to withstand and survive many bad and

extreme scenarios. These scenarios include

events such as what happened in 2008, other

historically damaging events and also new

situations that might occur. We manage

our company so that even under the worst

market stress test conditions, we would

almost never bear a loss of more than $5

billion (remember, we earn approximately

$10 billion pre-tax, pre-provision each

quarter). We recognize that on rare occa-

sions, we could experience a negative signifi-

cant event that could lead to our having a

poor quarter. But we will be vigilant and will

never take such a high degree of risk that it

jeopardizes the health of our company and

our ability to continue to serve our clients.

This is a bedrock principle. Later in this

letter, I will also describe how we think about

idiosyncratic geopolitical risk.

And the capital we have to bear losses is

enormous.

We have an extraordinary amount of capital

to sustain us in the event of losses. It is

instructive to compare assumed extreme

losses against how much capital we have for

this purpose.

You can see in the table below that JPMorgan

Chase alone has enough loss absorbing

resources to bear all the losses, assumed by

CCAR, of the 31 largest banks in the United

States. Because of regulations and higher

capital, large banks in the United States are

far stronger. And even if any one bank might

fail, in my opinion, there is virtually no

chance of a domino eect. Our shareholders

should understand that while large banks do

significant business with each other, they do

not directly extend much credit to one other.

And when they trade derivatives, they mark-

to-market and post collateral to each other

every day.

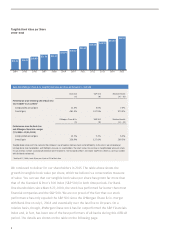

Resilience of JPMorgan Chase through multiple layers of protection

($ in billions)

Total loss absorbing resources

December 31, 2015:

JPMorgan Chase quarterly estimated

pre-tax, pre-provision earnings ~$ 10

Eligible long-term debt $ 125

Preferred equity 26 CCAR industry losses2

CET1 173 JPMorgan Chase losses $ 55

Total reserves1 25 Losses of 30 other participating banks 167

Total resources ˜$ 350 Total CCAR losses $ 222

1 Includes credit, legal, tax and valuation reserves.

2 As estimated for the nine quarters ending December 31, 2016, by the Federal Reserve in the 2015 CCAR severely adverse scenario.

Note: Numbers may not sum due to rounding.