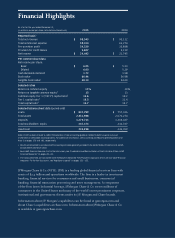

JP Morgan Chase 2015 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2015 JP Morgan Chase annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

99

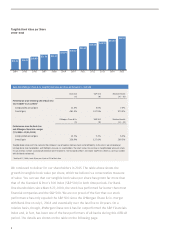

Virtually all of our businesses are close to

best in class, in overhead ratios and, more

important, in return on equity (ROE), as

shown on the chart on page 8. Of even more

relevance, we have these strong ratios while

making sizable investments for the future

(which we have reported on extensively in

the past and you can read more about in the

CEO letters). It is easy to meet short-term

targets by skimping on investments for

the future, but that is not our approach for

building the business for the long term.

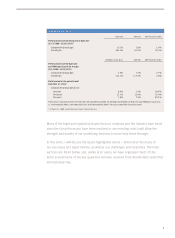

How do you compare your franchises with your peers? What makes you believe your businesses

are strong?

We are deeply aware that our clients

choose who they want to do business with

each and every day, and we are gratified

that we continue to earn our clients’ busi-

ness and their trust. If you are gaining

customers and market share, you have to

be doing something right. The chart below

shows that we have been meeting this goal

fairly consistently for 10 years.

Irreplicable Client Franchises Built Over the Long Term

2006 2014 2015

Consumer &

Community

Banking

Deposits market share1

# of top 50 Chase markets

where we are #1 (top 3) deposits

Average deposits growth rate

Active mobile customers growth rate

Card sales market share2

Merchant processing volume3,4

3.6%

11 (25)

7.7%

NM

16%

#3

7.6%

13 (40)

7.4%

22.1%

21%

#1

7.9%

12 (40)

9.0%

19.5%

21%

#1

Relationships with ~50% of U.S. households

#1 primary banking relationship share in Chase footprint11

#1 retail bank in the U.S. for acquiring, developing and

retaining customers12

#1 U.S. credit card issuer based on loans outstanding13

#1 U.S. co-brand credit card issuer14

#1 wholly-owned merchant acquirer15

Corporate &

Investment

Bank

Global Investment Banking fees5

Market share5

Total Markets revenue6

Market share6

FICC6

Market share6

Equities6

Market share6

#2

8.6%

#8

7.9%

#7

9.1%

#8

6.0%

#1

8.0%

#1

15.5%

#1

17.5%

#3

11.6%

#1

7.9%

#1

15.9%

#1

18.3%

#3

12.0%

>80% of Fortune 500 companies do business with us

Top 3 in 16 product areas out of 1716

#1 in both N.A. and EMEA Investment Banking fees17

#1 in Global Debt, Equity and Equity-related17

#1 in Global Long-Term Debt and Loan Syndications17

#1 in FICC productivity18

Top 3 Custodian globally with AUC of $19.9 trillion

#1 USD clearing house with 18.9% share in 201519

Commercial

Banking

# of states with Middle Market

banking presence

Multifamily lending7

Gross Investment Banking

revenue ($ in billions)

% of North America

Investment Banking fees

22

#28

$0.7

16%

30

#1

$2.0

35%

32

#1

$2.2

36%

#1 in customer satisfaction20

Leveraging the firm’s platform — average ~9 products/client21

Top 3 in overall Middle Market, large Middle Market

and ABL bookrunner

Industry-leading credit performance — 4th straight year of net

recoveries or single digit NCO rate

Asset

Management

Mutual funds with a 4/5 star rating8

Global active long-term open-end

mutual fund AUM flows9

AUM market share9

North America Private Bank (Euromoney)

Client assets market share10

119

#2

1.8%

#1

~3%

226

#1

2.5%

#1

~4%

231

#2

2.6%

#1

~4%

84% of 10-year long-term mutual fund AUM in top 2 quartiles22

Positive client asset flows every year since 2004

#3 Global Private Bank and #1 LatAm Private Bank23

Revenue and long-term AUM growth ~80% since 2006

Doubled GWM client assets (2x industry rate) since 200610

For footnoted information, refer to slide 42 in the 2016 Firm Overview Investor Day presentation, which is available on JPMorgan Chase & Co.’s website at

(http://investor.shareholder.com/jpmorganchase/presentations.cfm), under the heading Investor Relations, Investor Presentations, JPMorgan Chase 2016 Investor Day,

Firm Overview, and on Form 8-K as furnished to the SEC on February 24, 2016, which is available on the SEC’s website (www.sec.gov).

NM = Not meaningful