Honeywell 2013 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2013 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

•Global demand for commercial air travel as reflected in global flying hours and utilization rates

for corporate and general aviation aircraft, as well as the demand for spare parts and

maintenance and repair services for aircraft currently in use;

•Level and mix of U.S. and foreign government appropriations for defense and space programs

and military activity;

•Changes in customer platform development schedules, requirements and demands for new

technologies;

•Availability and price variability of raw materials such as nickel, titanium and other metals; and

•International regulation affecting aircraft operating equipage.

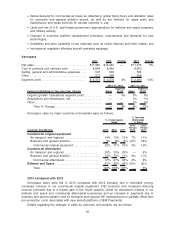

Aerospace

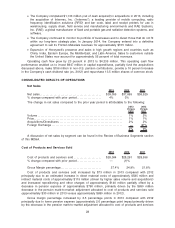

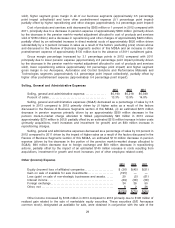

2013 2012 Change 2011 Change

Net sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $11,980 $12,040 — $11,475 5%

Cost of products and services sold . . . . . . . . . . . . . . 8,848 8,949 8,655

Selling, general and administrative expenses . . . . 547 606 589

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213 206 208

Segment profit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2,372 $ 2,279 4% $ 2,023 13%

Factors Contributing to Year-Over-Year Change Sales

Segment

Profit Sales

Segment

Profit

2013 vs. 2012 2012 vs. 2011

Organic growth/ Operational segment profit . . . . . . . . . . . . . — 4% 3% 8%

Acquisitions and divestitures, net . . . . . . . . . . . . . . . . . . . . . . . — — 1% 1%

Other. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — 1% 4%

Total % Change . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 4% 5% 13%

Aerospace sales by major customer end-markets were as follows:

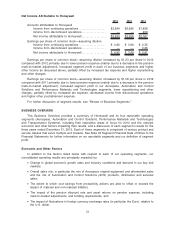

Customer End-Markets 2013 2012 2011

2013

Versus

2012

2012

Versus

2011

% of Aerospace

Sales

% Increase

(Decrease)

in Sales

Commercial original equipment

Air transport and regional . . . . . . . . . . . . . . . . . . . . . . . . . . 14% 13% 13% 7% 11%

Business and general aviation . . . . . . . . . . . . . . . . . . . . . . 8% 8% 6% (3)% 34%

Commercial original equipment . . . . . . . . . . . . . . . . . . . 22% 21% 19% 3% 19%

Commercial aftermarket

Air transport and regional . . . . . . . . . . . . . . . . . . . . . . . . . . 25% 25% 25% — 4%

Business and general aviation . . . . . . . . . . . . . . . . . . . . . . 12% 12% 11% 6% 17%

Commercial aftermarket . . . . . . . . . . . . . . . . . . . . . . . . . . 37% 37% 36% 2% 8%

Defense and Space . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41% 42% 45% (5)% (3)%

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100% 100% 100% — 5%

2013 compared with 2012

Aerospace sales were flat in 2013 compared with 2012 primarily due to favorable pricing,

increased volumes in our commercial original equipment (OE) business and increased licensing

revenue (primarily due to a royalty gain in the fourth quarter), offset by decreased volumes in our

defense and space and commercial aftermarket businesses and an increase in payments due to

business and general aviation and air transport and regional OE manufacturers to partially offset their

pre-production costs associated with new aircraft platforms (OEM Payments).

Details regarding the changes in sales by customer end-markets are as follows:

35