Foot Locker 2003 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2003 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

Income Taxes

The Company determines its deferred tax provision under the liability method, whereby deferred tax assets and liabilities

are recognized for the expected tax consequences of temporary differences between the tax bases of assets and liabilities

and their reported amounts using presently enacted tax rates. Deferred tax assets are recognized for tax credit and net

operating loss carryforwards, reduced by a valuation allowance, which is established when it is more likely than not that

some portion or all of the deferred tax assets will not be realized. The effect on deferred tax assets and liabilities of a change

in tax rates is recognized in income in the period that includes the enactment date.

A taxing authority may challenge positions that the Company has adopted in its income tax filings. Accordingly, the

Company may apply different tax treatments for transactions in filing its income tax returns than for income tax financial

reporting. The Company regularly assesses its tax position for such transactions and records reserves for those differences.

Provision for U.S. income taxes on undistributed earnings of foreign subsidiaries is made only on those amounts in

excess of the funds considered to be permanently reinvested.

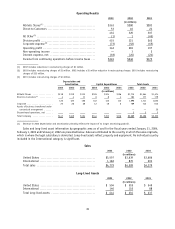

Insurance Liabilities

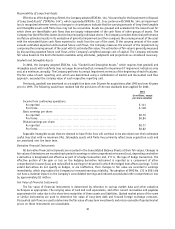

The Company is primarily self-insured for health care, workers’ compensation and general liability costs. Accordingly,

provisions are made for the Company’s actuarially determined estimates of discounted future claim costs for such risks

for the aggregate of claims reported and claims incurred but not yet reported. Self-insured liabilities totaled $14.0 million

and $16.1 million at January 31, 2004 and February 1, 2003, respectively. The Company discounts its workers’

compensation and general liability using a risk-free interest rate. Imputed interest expense related to these liabilities

was $1 million in 2003 and $2 million in both 2002 and 2001.

Foreign Currency Translation

The functional currency of the Company’s international operations is the applicable local currency. The translation

of the applicable foreign currency into U.S. dollars is performed for balance sheet accounts using current exchange rates

in effect at the balance sheet date and for revenue and expense accounts using the weighted-average rates of exchange

prevailing during the year. The unearned gains and losses resulting from such translation are included as a separate

component of accumulated other comprehensive loss within shareholders’ equity.

Reclassifications

Certain balances in prior fiscal years have been reclassified to conform to the presentation adopted in the current

year. In addition, the adoption of SFAS No. 144 in 2002, which also supersedes the accounting and reporting requirements

of APB No. 30, “Reporting the Results of Operations — Reporting the Effects of Disposal of a Segment of a Business, and

Extraordinary, Unusual and Infrequently Occurring Events,” required balance sheet reclassifications for the presentation

of discontinued operations and other long-lived assets held for disposal.

Recent Accounting Pronouncements

Several recent accounting pronouncements not previously discussed herein became effective during 2003. The

adoption of these pronouncements did not have a material impact on the Company’s consolidated financial position,

results of operations or cash flows. The adopted pronouncements were as follows:

•SFAS No. 149, “Amendment of Statement 133 on Derivative Instruments and Hedging Activities”

•SFAS No. 150, “Accounting for Certain Financial Instruments with Characteristics of both Liabilities and Equity”

•FASB Interpretation No. 46, “Consolidation of Variable Interest Entities”

31