Foot Locker 2003 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2003 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

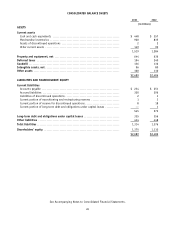

The Company is required to perform an impairment review of its goodwill, at least annually. The Company has chosen

to perform this review at the beginning of each fiscal year, and it is done in a two-step approach. The initial step requires

that the carrying value of each reporting unit be compared with its estimated fair value. The second step — to evaluate

goodwill of a reporting unit for impairment — is only required if the carrying value of that reporting unit exceeds its

estimated fair value. The fair value of each of the Company’s reporting units exceeded its carrying value as of February 2,

2003. The Company used a combination of a discounted cash flow approach and market-based approach to determine the

fair value of a reporting unit, which requires judgment and uses one or more methods to compare the reporting unit with

similar businesses, business ownership interests or securities that have been sold.

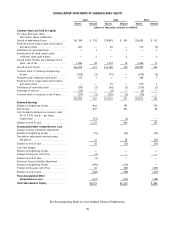

Pension and Postretirement Liabilities

The Company determines its obligations for pension and postretirement liabilities based upon assumptions related

to discount rates, expected long-term rates of return on invested plan assets, salary increases, age, mortality and health

care cost trends, among others. Management reviews all assumptions annually with its independent actuaries, taking into

consideration existing and future economic conditions and the Company’s intentions with regard to the plans.

Management believes that its estimates for 2003, as disclosed in “Item 8. Consolidated Financial Statements and

Supplementary Data,” to be reasonable. The expected long-term rate of return on invested plan assets is a component

of pension expense and the rate is based on the plans’ weighted-average target asset allocation of 64 percent equity

securities and 36 percent fixed income investments, as well as historical and future expected performance of those assets.

The Company’s common stock represented approximately two percent of the total pension plans’ assets at January 31,

2004. A decrease of 50 basis points in the weighted-average expected long-term rate of return would have increased 2003

pension expense by approximately $2.5 million. The actual return on plan assets in a given year may differ from the

expected long-term rate of return and the resulting gain or loss is deferred and amortized into the plans’ performance

over time. An assumed discount rate is used to measure the present value of future cash flow obligations of the plans

and the interest cost component of pension expense and postretirement income. The discount rate is selected with

reference to the long-term corporate bond yield. A decrease of 50 basis points in the weighted-average discount rate would

have increased the accumulated benefit obligation as of January 31, 2004 of the pension and postretirement plans by

approximately $30 million and approximately $0.6 million, respectively. Such a decrease would not have significantly

changed 2003 pension expense or postretirement income. There is limited risk to the Company for increases in healthcare

costs related to the postretirement plan as new retirees have assumed the full expected costs and existing retirees have

assumed all increases in such costs since the beginning of fiscal year 2001. The additional minimum liability included

in shareholders’ equity at January 31, 2004 for the pension plans represented the amount by which the accumulated

benefit obligation exceeded the fair market value of the plan assets. The Company was able to reduce the additional

minimum liability by $16 million during 2003 to reflect the better performance of the plans’ assets as well as a $50 million

contribution made in February 2003.

The Company expects to record postretirement income of approximately $13 million and pension expense of

approximately $18 million in 2004. Pension expense would be $22 million in 2004 had the Company not made the

$44 million contribution to its U.S. qualified retirement plan and the $6 million required contribution to its Canadian

qualified retirement plan.

Discontinued, Repositioning and Restructuring Reserves

The Company exited four business segments as part of its discontinuation and restructuring programs. The final

discontinued segment and disposition of the restructured businesses were completed in 2001. In order to identify and

calculate the associated costs to exit these businesses, management made assumptions regarding estimates of future

liabilities for operating leases and other contractual agreements, the net realizable value of assets held for sale or disposal

and the fair value of non-cash consideration received. The Company has settled the majority of these liabilities and the

remaining activity relates to the disposition of the residual lease liabilities.

17