Food Lion 2008 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2008 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

|

|

• AmendmenttoIAS27Consolidated and Separate Financial Statements (applicable for annual periods beginning on or after July 1, 2009): The revised IAS

27 requires that changes in the ownership interest of a subsidiary (without loss of control) is accounted as an equity transaction and will therefore not result in

goodwill or gains any longer. Furthermore, the amended standard changes the accounting for losses incurred by the subsidiary as well as the loss of control

of a subsidiary. Any remaining interest in the entity is re-measured at fair value, and a gain or loss is recognized in profit or loss. Delhaize Group will apply the

revised standard prospectively to transactions with non-controlling interests from January 1, 2010 and will have to change prospectively its current accounting

policy in this respect, as the Group is currently applying the so-called “parent entity extension.”

• AmendmentstoIAS32andIAS1 Puttable Financial Instruments and Obligations Arising on Liquidation (applicable for annual periods beginning on or

after January 1, 2009): The amendments provide a limited scope exception for puttable instruments to be classified as equity if they fulfil a number of speci-

fied features. The amendments to the standards will have no impact on the financial position or performance of the Group, as the Group has not issued such

instruments.

• AmendmentsIAS39Eligible Hedged Items (applicable for annual periods beginning on or after July 1, 2009): The amendment addresses the designation of

a one-sided risk in a hedged item, and the designation of inflation as a hedged risk or portion in particular situations. It clarifies that an entity is permitted to

designate a portion of the fair value changes or cash flow variability of a financial instrument as hedged item. The Group has investigated the amendments

and concluded that they will have no impact on the financial position or performance of the Group, as the Group has not entered into any such transactions.

• IFRIC13Customer Loyalty Programmes (applicable for annual periods beginning on or after July 1, 2008): This interpretation requires customer loyalty credits

to be accounted for as a separate component of the sales transaction in which they are granted. A portion of the fair value of the consideration received is

allocated to the award credits and deferred. This is then recognized as revenue over the period that the award credits are redeemed. The Group maintains

various loyalty points programs and believes that the current accounting practice is broadly in line with IFRIC 13 and therefore concluded that the application

of the interpretation will have an immaterial impact on the consolidated financial statements.

• IFRIC15Agreements for the Construction of Real Estate (applicable for annual periods beginning on or after January 1, 2009): The Interpretation clarifies

when and how revenue and related expenses from the sale of a real estate unit should be recognized if an agreement between a developer and a buyer is

reached before the construction of the real estate is completed. Furthermore, and more important for a wider range of companies, the interpretation provides

guidance on how to determine whether an agreement is within the scope of IAS 11 or IAS 18 and introduces the so-called “continuous transfer of risk and

rewards” approach into the IAS 18 literature. The Group has carefully considered the guidance included in IFRIC 15 and concluded that it will not have an impact

on the consolidated financial statements.

• IFRIC16Hedges of a Net Investment in a Foreign Operation (applicable for annual periods beginning on or after October 1, 2008): IFRIC 16 provides guid-

ance on the accounting for a hedge of a net investment. As such it provides guidance on identifying the foreign currency risks that qualify for hedge accounting

in the hedge of a net investment, where within the group the hedging instruments can be held in the hedge of a net investment and how an entity should

determine the amount of foreign currency gain or loss, relating to both the net investment and the hedging instrument, to be recycled on disposal of the net

investment. The Group concluded that there is currently no impact on the financial statements of the Group, as it does not hedge any of its net investments in

foreign operations.

• IFRIC17Distribution of non cash assets to owners (applicable for annual periods beginning on or after July 1, 2009): The Interpretation provides guidance

on how to account for distribution of non-cash assets to shareholders and clarifies that a dividend payable needs to be recognized when the dividend is

appropriately authorized and is no longer at the discretion of the entity. IFRIC 17 further points out that the liability needs to be measured at the fair value of the

asset to be distributed. IFRIC 17 amended IFRS 5 in connection with a non-current asset held for distribution, which is required to be measured at the lower of

its carrying value and fair value less costs to distribute. At distribution of the non-cash asset to the shareholder, the difference between the carrying values of

the liability and the asset distributed is recognized in a different line item in profit or loss. Delhaize Group has reviewed the requirements of the Interpretation

and concluded that it currently has no impact on the Group’s financial statements.

• IFRIC18Transfers of Assets from Customers (applicable for transfers of assets from customers received on or after July 1, 2009): The Interpretation applies

to agreements in which an entity receives from a customer an item of property, plant and equipment - or cash to acquire or construct such an item - that the

entity must then use either to connect the customer to a network or to provide the customer with ongoing access to a supply of goods or services, or to do

both. The Interpretation notes that the item needs to be recognized at fair value, if it represents an asset for the entity and clarifies the revenue recognition

incorporated in such a transfer agreement. Delhaize Group is currently in the process of reviewing the requirements of IFRIC 18 and has not concluded on the

impact the Interpretation might have on the Group’s financial statements.

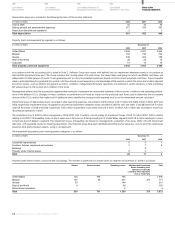

Financial Risk Management, Objectives and Policies

Delhaize Group’s principle financial liabilities, other than derivatives, comprise mainly debts and borrowings and trade and other payables. These financial

liabilities are mainly held in order to raise funds for the Group’s operations. On the other hand, the Group holds notes receivables, other receivables and cash

and cash-equivalents that result directly from the Group’s activities. The Group also holds several available-for-sale investments and enters into derivative trans-

actions.

Consequently, the Group is exposed to market risk, credit risk and liquidity risk, which are evaluated by Delhaize Group’s management and Board of Directors

and discussed in the section “Risk Factors” in this annual report.

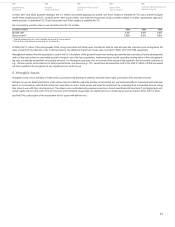

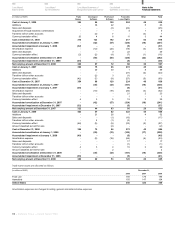

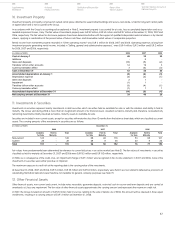

3. Acquisitions of subsidiary and minority interest

Business combinations

Acquisition of P.L.L.C.

On February 14, 2008, Delhaize Group acquired 100% of the shares and voting rights of P.L.Logistics Center – Dianomes – Apothikefsis - Logistics (P.L.L.C.) for

an amount of EUR 12 million. This company owns mainly land and construction permits at Inofyta, Greece, where a new distribution center of fresh products is

currently under construction. The fair value of the acquired land amounts to EUR 9 million and goodwill of EUR 5 million has been recognized. P.L.L.C. has been

included in the consolidated financial statements since February 14, 2008.

Consolidated

Balance Sheets

Consolidated

Income Statements

Consolidated Statements of

Recognized Income and Expense

Consolidated

Statements of Cash Flows

78 - Delhaize Group - Annual Report 2008

Notes to the

Financial Statements