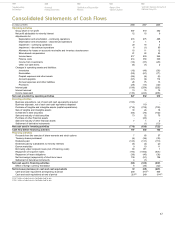

Food Lion 2008 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2008 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

|

|

Shortly after the October 2008 amendments were issued, it became apparent that the effective date and the transitional requirements of the October amend-

ment had been ambiguously drafted and as a result did not fully reflect the IASB’s intentions. The IASB corrected this subsequently. As the initial amendments

had no impact on the Group, the subsequent clarification with respect to the effective date and transition did neither.

Standards and Interpretations Issued but not yet Effective

The following standards, amendments to existing standards or interpretations have been published and are mandatory for the Group’s accounting periods

beginning on January 1, 2009 or later periods, but Delhaize Group has not early adopted them:

• Improvements to IFRS: The IASB has adopted an annual process to deal with non-urgent, but necessary, minor amendments to IFRSs (the “annual improve-

ments process”). The first Improvements to IFRS were issued on May 22, 2008 in two parts. Part I includes those amendments that result in accounting changes

for presentation, recognition or measurement purposes. Part II includes those amendments that are terminology or editorial changes only, which the IASB

expects to have no or minimal effect on accounting. Most amendments of Part I and all of Part II are effective as of January 1, 2009, with one being effective for

annual periods beginning on or after July 1, 2009. Delhaize Group has reviewed the 34 amendments to various standards and expects that the amendments

will have no impact on the financial performance or position of the Group, although some of the amendments might require additional disclosures. Delhaize

Group will update its accounting policies, where appropriate, in order to reflect the amendments made by the IASB.

• AmendmentsIFRS1andIAS27Cost of an Investment in a subsidiary, jointly controlled entity or associate (annual periods beginning on or after January

1, 2009). The amendments allow first-timer adopters to use a deemed cost of either fair value or the carrying amount under previous accounting practice

to measure the initial costs of investments in subsidiaries, jointly controlled entities or associates in the separate financial statements. The amendment also

removes the definition of the cost method from IAS 27 and replaces it with a requirement to present dividends as income in the separate financial statements

of the investor. The amendments will not have any impact on the consolidated financial statements of the Group.

• RevisedIFRS1First Time Adoption of IFRS (annual periods beginning on or after January 1, 2009). This Standard replaces IFRS 1 First Time Adoption of

IFRS initially issued in 2003 and subsequently amended several times to accommodate first-time adoption requirements resulting from new or amended

IFRS. The revised version issued in 2008 retains the substance of the previous version (including the change mentioned above), but changed the structure of

the standard to make it easier for the reader. The revised standard will have no impact on Delhaize Group.

• AmendmentstoIFRS2Vesting Conditions and Cancellations (annual periods beginning on or after January 1, 2009). The amended standard deals with

vesting conditions and cancellations. It clarifies that vesting conditions are service conditions and performance conditions only. Other features of a share-based

payment are not vesting conditions. These features would need to be included in the grant date fair value for transactions with employees and others providing

similar services; they would not impact the number of awards expected to vest or valuation thereof subsequent to grant date. All cancellations, whether by

the entity or by other parties, should receive the same accounting treatment. As indicated above, currently Delhaize Group’s share-based compensation plans

contain service conditions only. Therefore, the amendment has no impact on the consolidated financial statements of the Group.

• RevisedIFRS3Business Combinations (applicable to business combinations for which the acquisition date is on or after the beginning of the first annual

reporting period beginning on or after July 1, 2009). While the revised IFRS 3 continues to apply the purchase accounting method, it introduces a number of

changes in the accounting for business combinations that will impact the amount of goodwill recognized, the reported results in the period of the acquisition

and future results. Main changes relate to the definition of a business, the treatment of contingent consideration and transaction costs, the accounting for

any pre-existing interest in the acquiree and the measurement of minority interest (now referred to as “non-controlling interest”), where the acquirer has the

option (on a acquisition-by-acquisition basis) to measure them either at fair value or at its proportionate interest in the identifiable asset and liabilities of the

acquiree (which equals the current method used in IFRS 3). Delhaize Group will apply the revised IFRS 3 prospectively for business combinations taking place

after January 1, 2010. Therefore, there will be no impact on prior periods in the Group’s 2010 consolidated financial statements.

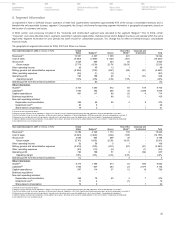

• IFRS8Operating Segments (applicable for annual periods beginning on or after January 1, 2009): The standard replaces IAS 14 Segment Reporting and

introduces the so-called “management approach” to segment reporting into the IFRS literature. The Standard requires an entity to report financial and descrip-

tive information about its reportable segments. Reportable segments are operating segments or aggregations of operating segments that meet specified

criteria. Operating segments are components of an entity about which separate financial information is available that is evaluated regularly by the chief oper-

ating decision maker in deciding how to allocate resources and in assessing performance. Generally, financial information is required to be reported on the

same basis as is used internally for evaluating operating segment performance and deciding how to allocate resources to operating segments.

As indicated above, Delhaize Group currently presents primary segment information in respect of its geographical segments (see Note 6). The Group has

completed its assessment of the impact of the revised guidance and has concluded that IFRS 8 will not have an impact on the Group’s reportable segments.

• RevisedIAS1 Presentation of Financial Statements (annual periods beginning on or after January 1, 2009): The revised standard introduces several (smaller)

changes to IAS 1, with the most significant being the requirement to separate owner and non-owner changes in equity and the introduction of the statement of

comprehensive income, which contains all items of recognized income and expense, either in one or two statements. As the currently used SoRIE is no longer

a statement of changes in equity, a consequential change of these new requirements for the Group is that the Consolidated Statements of Changes in Equity

(see Note 16) will have to be presented outside the notes as a primary statement. As all changes relate to presentation only, the implementation of the revised

IAS 1 will have no impact on the financial performance of the Group. Delhaize Group is still evaluating whether it will continue to present two statements or

might want to change to one statement. Based on the Group’s detailed analysis of the changes, Delhaize Group concluded that it has all the information at

hand in order to comply with all revised presentation requirements. Financial statements in accordance with the revised IAS 1 will be presented in the Group’s

first 2009 interim reporting, prepared in accordance with IAS 34.

• AmendmenttoIAS23Borrowing Costs (applicable for annual periods beginning on or after January 1, 2009): The amendment requires an entity to capitalize

borrowing costs directly attributable to the acquisition, construction or production of a qualifying asset (one that takes a substantial period of time to get ready

for use or sale) as part of the cost of that asset. The option of immediately expensing those borrowing costs will be removed. As explained above, Delhaize

Group is already applying the option to capitalize borrowing costs. Therefore, the adoption of the amended IAS 23 has no impact on the financial statements

of the Group.

77

Certification of Responsible

Persons

Historical

Financial Overview

Report of the

Statutory Auditor

Summary Statutory Accounts of

Delhaize Group SA

Supplementary

Information