Alpine 2010 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2010 Alpine annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

|

|

14

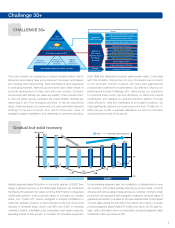

During the fiscal year ended March 31, 2010, the world economy showed signs of partial

recovery in financial-related sectors and stock markets from mid-year onward, bringing

evidence that the recession had bottomed out. However, aggravated employment conditions

and reduced incomes impeded personal consumption. These and other factors resulted in a

continued severe overall economic climate.

The automobile industry featured major structural changes, led by regionally disparate

developments for manufacturers: failures in the United States, restructuring and integration

in Europe, and developing nations’ emergence as a serious economic force. Against this

background, the governments of Japan, the United States and various European countries

responded with new car replacement subsidization policies, which spurred sales of compact

cars and environmentally responsive vehicles. In addition, the automobile markets of

developing nations expanded, with China overtaking the United States as the leading country

in terms of unit sales of new cars during the year.

There were indications of recovery for the car electronics industry, but a demand shift toward

compact cars, which feature lower factory installation rates for navigation systems, and

lackluster personal consumption undermined sales of brand-name products and after-market

sales to automobile manufacturers.

Under these conditions, the Alpine Group persevered in its drive to improve performance,

launching new products in the domestic after-market and carrying out aggressive activities

geared to gaining orders from automobile manufacturers. We also promoted our “CHALLENGE

30 Plus” program of structural reforms, implemented thorough cost-reductions, streamlined

investment in R&D and capital investment, and revised our global production system.

Performance by Segment

Audio Products

In the Audio Products segment, we carried out aggressive proposal-based marketing in the

domestic after-market of high-end speakers and amplifiers for minivans with clear cabin audio

reproduction, leading to an expanded market share. However, intensified price competition

over head units contributed to harsh operating conditions. In the European and U.S. after-

markets, sound system products with upgraded cabin audio quality, including speakers and

amplifiers, and Bluetooth-enabled CD players, which were launched in the European market

during the second half of the year, posted steady sales. Nonetheless, CD players, which

started the term on a positive sales note in North America, suffered sales declines, impacted

by lackluster personal consumption.

Orders for brand-name products by automobile manufacturers showed a partial recovery as a

result of a return to appropriate inventory levels for new cars following a period of adjustment.

However, the tardy pace of recovery in production by automobile manufacturers meant that

these positive indications stopped short of a full-blown recovery in sales.

Such key products for the segment as car audio equipment, led by CD players, continued

to gravitate toward integrated visual and car navigation products. For Alpine, sales of such

integrated products tend to augment sales in the Information and Communication Equipment

Segment, to the detriment of Audio Products Segment sales.

As a result of the above factors, sales by the Audio Products segment during the term

decreased by 20.3% compared to the corresponding period of the previous fiscal year, to

¥70.5 billion (US$757.3 million).

Information and Communication Equipment Segment

In this segment, we focused on the Rear Vision Navigation X08 Premium, a newly debuted

product in the domestic after-market, expanded our “minvan car life strategy,” developed

promotional activities targeting the family consumer bracket, and reinforced proposal-based

marketing. This system solution gained widespread acclaim from customers. In addition,

we provided added-value products and services attuned to customer needs through such

initiatives as deploying lines tailored specifically to individual car models and introducing

packages for hot-selling eco-cars. We also bolstered business for new car dealers and

promoted sales of Car Beena, a rear-seat entertainment system, with combined educational

and recreational benefits for younger passengers. This and other measures contributed to the

segment’s sales during the term.

The Rear Vision Navigation X08 Premium is a system product composed of a Rear Vision

rear-seat large-screen, high-picture-quality entertainment system, compatible with DVD and

terrestrial digital broadcasting, and an X08 navigation system with an advanced driving-

assistance function. During the fiscal year, the Rear Vision Navigation X08 Premium was

awarded a 2009 Nikkan Jidosha Shimbun (a daily automotive newspaper) product prize in the

Car Navigation category.

Overseas Sales

(Millions of yen)

2006 2007

138,335

2008

215,281

2009

228,379

2010

166,873

219,056

Capital Expenditures

(Millions of yen)

2006 2007

4,379

2008

10,778

2009

12,620

2010

10,160

13,673

Total Assets/Net Assets

(Millions of yen)

2006

181,185

120,908

2007 2008

153,036

97,036

2009

169,553

112,377

2010

132,423

96,874

167,785

116,265

Total Assets

Net Assets

Net Assets for the years from 2006 is recalculated.

Consolidated Financial Review