Whirlpool 2012 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2012 Whirlpool annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

|

|

PRIORITIES FOR SUSTAINABLE SUCCESS

We will continue to deliver the highest levels of performance

execution and build on the momentum of 2012. Our 2013

operating priorities of Winning Products | Winning

Performance | Winning People will be crucial to our

success and will support the achievement of our long-

term growth strategy through:

• Appliance ownership growth in new and emerging

markets

• Increased investments in our consumer-relevant

product innovations

• Growth in our higher-margin adjacent businesses

• Continued cost- and capacity-reduction initiatives

• Advancing our global product leadership

Our ability to move our business forward with focus,

consistency, discipline and speed will strengthen our

industry leadership this year and in the years to come.

We are encouraged by positive global trends that will

allow us to gain better traction from our actions. We see

structural demand growth returning in the U.S., our

largest market, driven by improving housing starts, a

modest return in discretionary spending and accelerated

appliance replacement, based on typical usage cycles.

Growth opportunities in emerging markets are also

expanding, with low appliance penetration levels in key

regions and strong underlying fundamentals. Our target

of 8 percent operating margins by 2014 is well within our

reach, as we further improve the mix of innovative new

products, broaden our higher-margin adjacent businesses,

continue executing our cost- and capacity-reduction

programs and maintain cost productivity.

In 2013, we will continue to make progress on our roadmap

for growth with great brands that bring leading consumer-

relevant innovation into consumers’ homes through

outstanding products. This map is a proven course for our

sustained success, framing the positive performance we

expect and creating long-term value for our shareholders.

At Whirlpool, we have only seen the beginning of our

return to value-creating results. We believe that the best

is yet to come as we work together, evolving into a leading

global branded consumer-products company.

Sincerely,

Jeff M. Fettig

Chairman of the Board and Chief Executive Officer

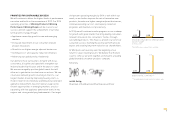

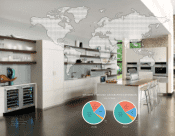

ONGOING BUSINESS OPERATIONS

CASH FLOW*

$ IN BILLIONS

2011 2012

DEBT/TOTAL CAPITAL**

2011 2012

$0.3

$0.9

36.8% 36.0%

**Total debt divided by total debt and total stockholders’ equity.

*Non-GAAP measure; see page 29 for reconciliation.

5