Vodafone 1999 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 1999 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77

|

|

P58-59 USA Accounting Principals

1999

£m

1998

£m

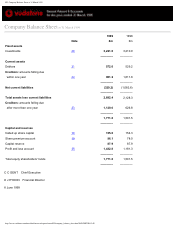

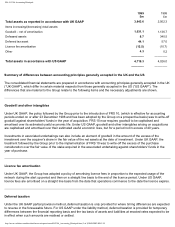

Total assets as reported in accordance with UK GAAP 3,643.6 2,502.3

Items increasing/(decreasing) total assets:

Goodwill – net of amortisation 1,031.1 1,136.7

Defeased assets 8.7 340.5

Deferred tax asset 44.1 57.0

Licence fee amortisation (12.5) (10.7)

Other 4.3 0.2

–––––––– ––––––––

Total assets in accordance with US GAAP 4,719.3 4,026.0

–––––––– ––––––––

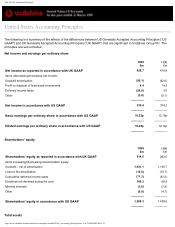

Summary of differences between accounting principles generally accepted in the UK and the US

The consolidated financial statements are prepared in accordance with accounting principles generally accepted in the UK

(“UK GAAP”), which differ in certain material respects from those generally accepted in the US (“US GAAP”). The

differences that are material to the Group relate to the following items and the necessary adjustments are shown.

Goodwill and other intangibles

Under UK GAAP, the policy followed by the Group prior to the introduction of FRS 10, (which is effective for accounting

periods ended on or after 23 December 1998 and has been adopted by the Group on a prospective basis) was to write-off

goodwill against shareholders’ funds in the year of acquisition. FRS 10 now requires goodwill to be capitalised and

amortised over its estimated useful economic life. Under US GAAP, goodwill and other intangibles arising on acquisitions

are capitalised and amortised over their estimated useful economic lives, but for a period not in excess of 40 years.

Investments in associated undertakings can also include an element of goodwill in the amount of the excess of the

investment over the acquirer’s share in the fair value of the net assets at the date of investment. Under UK GAAP, the

treatment followed by the Group prior to the implementation of FRS 10 was to write-off the excess of the purchase

consideration over the fair value of the stake acquired in the associated undertaking against shareholders’ funds in the

year of purchase.

Licence fee amortisation

Under UK GAAP, the Group has adopted a policy of amortising licence fees in proportion to the expected usage of the

network during the start up period and then on a straight line basis to the end of the licence period. Under US GAAP,

licence fees are amortised on a straight line basis from the date that operations commence to the date the licence expires.

Deferred taxation

Under the UK GAAP partial provision method, deferred taxation is only provided for where timing differences are expected

to reverse in the foreseeable future. For US GAAP under the liability method, deferred taxation is provided for temporary

differences between the financial reporting basis and the tax basis of assets and liabilities at enacted rates expected to be

in effect when such amounts are realised or settled.

http://www.vodafone.com/download/investor/reports/annual99/USA_Accounting_Principals.htm (2 of 3)30/03/2007 00:12:25