Vodafone 1999 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 1999 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

|

|

Financial Review

digital networks in the Netherlands, Australia and Greece to enhance capacity and improve quality of service. The Group

also intends to bid for third generation mobile phone licences, the UK auction for which is currently scheduled for early

2000.

BACK TO TOP

Treasury management and policy

The principal financial risks arising from the Group’s activities are funding risk, interest rate risk, currency risk and

counterparty risk. The Group’s treasury function provides a centralised service for funding, foreign exchange, interest rate

management and counterparty risk management.

Treasury operations are conducted within a framework of policies and guidelines authorised and reviewed annually by the

Board. The treasury function provides regular update reports to the Board. The Group uses a number of derivative

instruments, which are transacted for risk management purposes only, by specialist treasury personnel.

There has been no change during the year, or since the year end, to the major financial risks faced by the Group or the

Group’s approach to the management of those risks.

Funding and liquidity

The Group has a strong financial position, demonstrated by credit ratings of A-1/P-1 short term and A+/A2 long term from

Standard and Poor’s and Moody’s respectively, which enables the Group to access a wide range of debt finance,

including Eurobonds, commercial paper and committed bank facilities. Following completion of the merger with AirTouch it

is anticipated that these ratings will continue to be investment grade at A-1/P-1 short term and A/A2 long term.

The Board has approved ratios consistent with those used by companies with high credit ratings for net interest cover,

market capitalisation to net debt and net cash flow to net debt, which establish internal limits for the maximum level of

debt that the Group may have outstanding. Total Group interest, excluding that of associated undertakings, is covered 15

times by Group EBITDA (adjusted to exclude the Group’s share of the profit of associated undertakings).

The Group’s policy is to borrow centrally, using a mixture of long term and short term loans and borrowing facilities, to

meet anticipated funding requirements. These borrowings, together with cash generated from operations, are lent or

contributed as equity to subsidiaries.

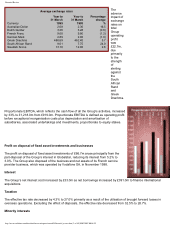

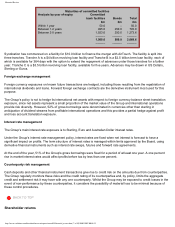

The Group’s net debt profile at the end of the year is shown below:

Net debt profile at 31 March 1999

Analysis by repayment year £m

Less than 1 year 371.1

Between 2-5 years 1,136.9

––––––

1,508.0

––––––

A substantial proportion of the debt maturing within one year is commercial paper, issued under the Group’s £800m multi-

currency Euro commercial paper programme, which is fully supported by committed bank facilities that expire in the period

to 30 November 2003.

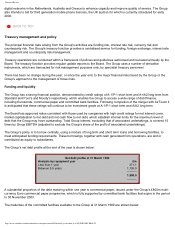

The maturities of the committed facilities available to the Group at 31 March 1999 are shown below:

http://www.vodafone.com/download/investor/reports/annual99/financial_review.htm (6 of 10)30/03/2007 00:08:22