United Healthcare 2007 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2007 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

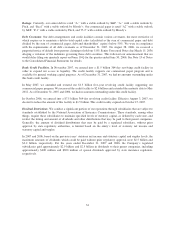

Ratings. Currently, our senior debt is rated “A-” with a stable outlook by S&P, “A-” with a stable outlook by

Fitch, and “Baa1” with a stable outlook by Moody’s. Our commercial paper is rated “A2” with a stable outlook

by S&P, “F-1” with a stable outlook by Fitch, and “P-2” with a stable outlook by Moody’s.

Debt Covenants. Our debt arrangements and credit facilities contain various covenants, the most restrictive of

which require us to maintain a debt-to-total-capital ratio (calculated as the sum of commercial paper and debt

divided by the sum of commercial paper, debt and shareholders’ equity) below 50%. We were in compliance

with the requirements of all debt covenants as of December 31, 2007. On August 28, 2006, we received a

purported notice of default from persons claiming to hold our 5.8% Senior Unsecured Notes due March 15, 2036

alleging a violation of the indenture governing those debt securities. This followed our announcement that we

would delay filing our quarterly report on Form 10-Q for the quarter ended June 30, 2006. See Note 13 of Notes

to the Consolidated Financial Statements for details.

Bank Credit Facilities. In November 2007, we entered into a $1.5 billion 364-day revolving credit facility in

order to expand our access to liquidity. The credit facility supports our commercial paper program and is

available for general working capital purposes. As of December 31, 2007, we had no amounts outstanding under

this bank credit facility.

In May 2007, we amended and restated our $1.3 billion five-year revolving credit facility supporting our

commercial paper program. We increased the credit facility to $2.6 billion and extended the maturity date to May

2012. As of December 31, 2007 and 2006, we had no amounts outstanding under this credit facility.

In October 2006, we entered into a $7.5 billion 364-day revolving credit facility. Effective August 3, 2007, we

elected to reduce the amount of this facility to $1.5 billion. This credit facility expired on October 15, 2007.

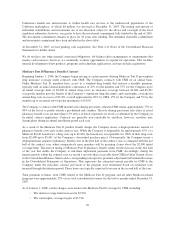

Dividend Restrictions. We conduct a significant portion of our operations through subsidiaries that are subject to

standards established by the National Association of Insurance Commissioners. These standards, among other

things, require these subsidiaries to maintain specified levels of statutory capital, as defined by each state, and

restrict the timing and amount of dividends and other distributions that may be paid to their parent companies.

Generally, the amount of dividend distributions that may be paid by a regulated subsidiary, without prior

approval by state regulatory authorities, is limited based on the entity’s level of statutory net income and

statutory capital and surplus.

In 2007 and 2006, based on the previous years’ statutory net income and statutory capital and surplus levels, the

maximum amounts of dividends which could be paid without prior regulatory approval were $2.5 billion and

$2.2 billion, respectively. For the years ended December 31, 2007 and 2006, the Company’s regulated

subsidiaries paid approximately $2.9 billion and $2.5 billion in dividends to their parent companies, including

approximately $400 million and $300 million of special dividends approved by state insurance regulators,

respectively.

34