U-Haul 2008 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2008 U-Haul annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

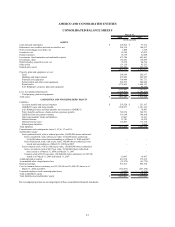

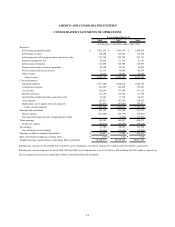

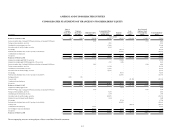

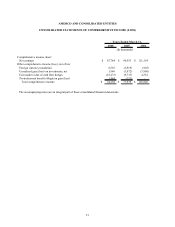

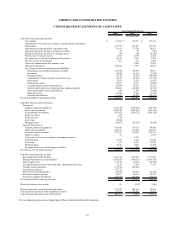

AMERCO AND CONSOLIDATED ENTITIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Note 1: Basis of Presentation

AMERCO has a fiscal year that ends on the 31st of March for each year that is referenced. Our insurance company

subsidiaries have fiscal years that end on the 31st of December for each year that is referenced. They have been consolidated

on that basis. Our insurance companies’ financial reporting processes conform to calendar year reporting as required by

state insurance departments. Management believes that consolidating their calendar year into our fiscal year financial

statements does not materially affect the financial position or results of operations. The Company discloses any material

events occurring during the intervening period. Consequently, all references to our insurance subsidiaries’ years 2007, 2006

and 2005 correspond to fiscal 2008, 2007 and 2006 for AMERCO.

Accounts denominated in non-U.S. currencies have been translated into U.S. dollars. Certain amounts reported in

previous years have been reclassified to conform to the current presentation.

Note 2: Principles of Consolidation

The consolidated balance sheet as of March 31, 2008 includes the accounts of AMERCO and its wholly-owned

subsidiaries. The consolidated balance sheet as of March 31, 2007 includes the accounts of AMERCO and its wholly-

owned subsidiaries and SAC Holding II and its subsidiaries (“SAC Holding II”). The March 31, 2008 statements of

operations and cash flows include AMERCO and its wholly-owned subsidiaries for the entire year, and reflect SAC

Holding II and its subsidiaries for the seven months ended October 31, 2007. The March 31, 2007 and 2006 statements of

operations and cash flows include the accounts of AMERCO and its wholly-owned subsidiaries and SAC Holding II and its

subsidiaries.

In fiscal 2003 and fiscal 2002, SAC Holding Corporation and its subsidiaries, and SAC Holding II Corporation and its

subsidiaries, collectively referred to as “SAC Holdings” were considered special purpose entities and were consolidated

based on the provisions of Emerging Issues Task Force (“EITF”) Issue No. 90-15. In fiscal 2004, the Company applied

Financial Accounting Standards Board Interpretation No. 46(R) (“FIN 46(R)”) to its interests in SAC Holdings. Initially,

the Company concluded that SAC Holdings were variable interest entities (“VIE”) and that the Company was the primary

beneficiary. Accordingly, the Company continued to include SAC Holdings in its Consolidated Financial Statements.

In February and March 2004 SAC Holding Corporation triggered a requirement to reassess AMERCO’ s involvement in

it, which led to the conclusion SAC Holding Corporation was not a VIE and AMERCO ceased to be the primary

beneficiary.

In November 2007, Blackwater Investments Inc. (“Blackwater”), wholly-owned by Mark V. Shoen, a significant

shareholder and executive officer of AMERCO contributed additional capital to its wholly-owned subsidiary, SAC Holding

II. This contribution was determined by us to be material with respect to the capitalization of SAC Holding II; thereby,

triggering a requirement under FIN 46(R) for us to reassess the Company’ s involvement with those subsidiaries. This

required reassessment led to the conclusion that SAC Holding II attained the ability to fund its own operations and execute

its business plan without any future subordinated financial support; therefore, the Company was no longer considered to be

the primary beneficiary of SAC Holding II as of the date of Blackwater’ s contribution.

Accordingly, at the dates AMERCO ceased to have a variable interest and ceased to be the primary beneficiary of SAC

Holding II and its current subsidiaries, it deconsolidated these entities. The deconsolidation was accounted for as a

distribution of SAC Holding II’ s interests to the sole shareholder of the SAC entities. Because of AMERCO’ s continuing

involvement with SAC Holding II and its subsidiaries, the distribution does not qualify as discontinued operations as

defined by SFAS 144.

It is possible that SAC Holdings could take future actions that would require us to re-determine whether SAC Holdings

has become a VIE or whether we have become the primary beneficiary of SAC Holdings. Should this occur, we could be

required to consolidate some or all of SAC Holdings with our financial statements.

F-8