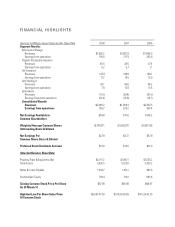

U-Haul 2008 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2008 U-Haul annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

9

Environmental laws and regulations are complex, change frequently and could become more stringent in the

future. We cannot assure you that future compliance with these regulations, future environmental liabilities, the cost

of defending environmental claims, conducting any environmental remediation or generally resolving liabilities

caused by us or related third parties will not have a material adverse effect on our business, financial condition or

results of operations.

Our quarterly results of operations fluctuate due to seasonality and other factors associated with our industry.

Our business is seasonal and our results of operations and cash flows fluctuate significantly from quarter to

quarter. Historically, revenues have been stronger in the first and second fiscal quarters due to the overall increase in

moving activity during the spring and summer months. The fourth fiscal quarter is generally weakest, due to a

greater potential for adverse weather conditions and other factors that are not necessarily seasonal. As a result, our

operating results for a given quarterly period are not necessarily indicative of operating results for an entire year.

We obtain our rental trucks from a limited number of manufacturers.

In the last ten years, we purchased most of our rental trucks from Ford Motor Company and General Motors

Corporation. Although we believe that we could obtain alternative sources of supply for our rental trucks,

termination of one or both of our relationships with these suppliers could have a material adverse effect on our

business, financial condition or results of operations for an indefinite period of time or we may not be able to obtain

rental trucks under similar terms, if at all. Additionally, our fleet rotation can be negatively affected by issues our

manufacturers face within their own supply chain. Such issues may impair their ability to fulfill our orders in a

timely fashion.

A.M Best financial strength ratings are crucial to our life insurance business.

A.M. Best downgraded Oxford and its subsidiaries during AMERCO’ s restructuring to C+. Upon AMERCO’ s

emergence from bankruptcy in March 2004, Oxford and its subsidiaries were upgraded to B-. The ratings were again

upgraded in October 2004 to B, in October 2005 to B+, and in November 2006 Oxford and Christian Fidelity Life

Insurance Company (“CFLIC”), a subsidiary of Oxford, were upgraded to B++ with a stable outlook. In January

2008, A.M. Best affirmed the financial strength rating for Oxford and CFLIC of B++ with a stable outlook and

assigned Dallas General Life Insurance Company (“DGLIC”), a subsidiary of CFLIC, with the same rating. Prior to

AMERCO’ s restructuring, Oxford was rated B++. Financial strength ratings are important external factors that can

affect the success of Oxford’ s business plans. Accordingly, if Oxford’ s ratings, relative to its competitors, are not

maintained or do not continue to improve, Oxford may not be able to retain and attract business as currently

planned.

We bear certain risks related to our notes receivable from SAC Holdings.

At March 31, 2008, we held approximately $198.1 million of notes receivable from SAC Holdings, which consist

of junior unsecured notes. SAC Holdings is highly leveraged with significant indebtedness to others. If SAC

Holdings is unable to meet its obligations to its senior lenders, it could trigger a default of its obligations to us. In

such an event of default, we could suffer a loss to the extent the value of the underlying collateral of SAC Holdings

is inadequate to repay SAC Holding’ s senior lenders and our junior unsecured notes. We cannot assure you that

SAC Holdings will not default on its loans to its senior lenders or that the value of SAC Holdings assets upon

liquidation would be sufficient to repay us in full.

We are highly leveraged.

As of March 31, 2008, we had total debt outstanding of $1,504.7 million and total undiscounted lease

commitments of $490.8 million. Although we believe that additional leverage can be supported by the Company’ s

operations, our existing debt could impact us in the following ways:

• require us to allocate a considerable portion of cash flows from operations to debt service payments;

• limit our ability to obtain additional financing; and

• place us at a disadvantage compared to our competitors who may have less debt.

Our ability to make payments on our debt depends upon our ability to maintain and improve our operating

performance and generate cash flow. To some extent, this is subject to prevailing economic and competitive

conditions and to certain financial, business and other factors, some of which are beyond our control. If we are

unable to generate sufficient cash flow from operations to service our debt and meet our other cash needs, we may

be forced to reduce or delay capital expenditures, sell assets, seek additional capital or restructure or refinance our

indebtedness. If we must sell our assets, it may negatively affect our ability to generate revenue. In addition, we may

incur additional debt that would exacerbate the risks associated with our indebtedness.