Red Lobster 2008 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2008 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

|

|

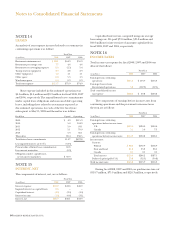

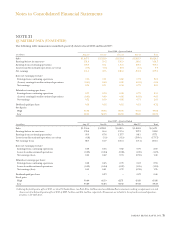

Notes to Consolidated Financial Statements

66 DARDEN RESTAURANTS, INC.

NOTE 17

RETIREMENT PLANS

DEFINED BENEFIT PLANS AND POSTRETIREMENT

BENEFIT PLAN

Substantially all of our employees are eligible to participate

in a retirement plan. We sponsor non-contributory defined

benefit pension plans, that have been frozen, for a group of

salaried employees in the United States, in which benefits are

based on various formulas that include years of service and

compensation factors; and for a group of hourly employees

in the United States, in which a fixed level of benefits is pro-

vided. Pension plan assets are primarily invested in U.S., inter-

national and private equities, long duration fixed-income

securities and real assets. Our policy is to fund, at a minimum,

the amount necessary on an actuarial basis to provide for

benefits in accordance with the requirements of the Employee

Retirement Income Security Act of 1974, as amended. We

also sponsor a contributory postretirement benefit plan that

provides health care benefits to our salaried retirees. During

fiscal 2008, 2007 and 2006, we funded the defined benefit

pension plans in the amounts of $0.5 million, $0.5 million and

$0.3 million, respectively. We expect to contribute approximately

$0.4 million to our defined benefit pension plans during fiscal

2009. During fiscal 2008, 2007 and 2006, we funded the

postretirement benefit plan in the amounts of $1.2 million,

$0.8 million and $0.4 million, respectively. We expect to

contribute approximately $0.6 million to our postretirement

benefit plan during fiscal 2009.

Effective May 27, 2007, we implemented the recognition

and measurement provisions of SFAS No. 158, “Employers’

Accounting for Defined Benefit Pension and Other Postretire-

ment Plans (an amendment of FASB Statements No. 87, 88,

106 and 132R).” The purpose of SFAS No. 158 is to improve

the overall financial statement presentation of pension and

other postretirement plans, but SFAS No. 158 does not impact

the determination of net periodic benefit cost or measurement

of plan assets or obligations. SFAS No. 158 requires companies

to recognize the over or under-funded status of the plan as an

asset or liability as measured by the difference between the fair

value of the plan assets and the benefit obligation and requires

any unrecognized prior service costs and actuarial gains and

losses to be recognized as a component of accumulated other

comprehensive income (loss).

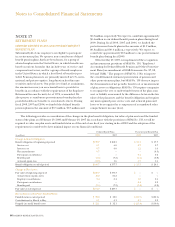

The following provides a reconciliation of the changes in the plan benefit obligation, fair value of plan assets and the funded

status of the plans as of February 29, 2008 and February 28, 2007 (in accordance with the provisions of SFAS No. 158, we will be

required to value our plan assets and funded status as of the end of our fiscal year starting in fiscal 2009 and the adoption of the

requirement is considered to have minimal impact on our financial condition):

Defined Benefit Plans Postretirement Benefit Plan

(in millions)

2008 2007 2008 2007

Change in Benefit Obligation:

Benefit obligation at beginning of period $ 177.7 $ 168.3 $ 20.1 $ 17.7

Service cost 6.1 6.0 0.7 0.7

Interest cost 9.7 9.0 1.2 1.0

Plan amendments 0.7 – – (0.3)

Participant contributions – – 0.4 0.2

Benefits paid (8.6) (7.2) (1.4) (0.8)

Actuarial (gain) loss (15.9) 1.6 4.7 1.6

Benefit obligation at end of period $ 169.7 $ 177.7 $ 25.7 $ 20.1

Change in Plan Assets:

Fair value at beginning of period $ 189.7 $ 175.3 $ – $ –

Actual return on plan assets 10.2 21.2 – –

Employer contributions 0.4 0.4 1.0 0.6

Participant contributions – – 0.4 0.2

Benefits paid (8.6) (7.2) (1.4) (0.8)

Fair value at end of period $ 191.7 $ 189.7 $ – $ –

Reconciliation of the Plan’s Funded Status:

Funded status at end of period $ 22.0 $ 12.0 $ (25.7) $ (20.1)

Contributions for March to May 0.1 0.1 0.3 0.2

Prepaid (accrued) benefit costs $ 22.1 $ 12.1 $ (25.4) $ (19.9)