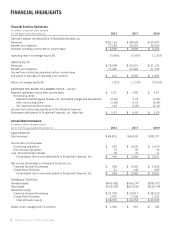

Prudential 2012 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2012 Prudential annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

For the contracts above guaranteed minimum crediting rates, although we have the ability to lower crediting rates, our willingness to

do so may be limited by competitive pressures.

Our domestic Financial Services Businesses also have approximately $14 billion of insurance liabilities and policyholder account

balances representing participating contracts for which the investment income risk is expected to ultimately accrue to contractholders. The

crediting rates for these contracts are periodically adjusted based on the yield earned on the related assets. The remaining $88 billion of the

$143 billion of insurance liabilities and policyholder account balances in our domestic Financial Services Businesses represents long

duration products such as group annuities, structured settlements and other insurance products that do not have stated crediting rate

guarantees, but have fixed and guaranteed terms, for which underlying assets may have to be reinvested at interest rates that are lower than

portfolio rates. We seek to mitigate the impact of a prolonged low interest rate environment on these contracts through asset-liability

management, as discussed further below.

For the domestic Financial Services Businesses’ general account, assuming a hypothetical scenario where the average 10-year U.S.

Treasury rate is 1.75% for the period from January 1, 2013 through December 31, 2014, and credit spreads remain unchanged from levels

as of December 31, 2012, we estimate that the unfavorable impact to net interest margins included in pre-tax adjusted operating income of

reinvesting in such an environment, compared to reinvesting at current average portfolio income yields, would be approximately $51

million in 2013 and $154 million in 2014. This impact is largely concentrated in the Retirement and Individual Annuities segments. This

hypothetical scenario only reflects the impact related to the approximately $41 billion of contracts with guaranteed minimum crediting rates

shown above, and does not reflect: i) any benefit from potential changes to the crediting rates on the corresponding contractholder

liabilities where the Company has the contractual ability to do so, or other potential mitigants such as changes in investment mix that we

may implement as funds are reinvested; ii) any impact related to assets that do not directly support our liabilities; iii) any impact from other

factors, including but not limited to, new business, contractholder behavior, changes in competitive conditions, and changes in capital

markets; and/or iv) any impact from other factors described below.

In order to mitigate the unfavorable impact that the current interest rate environment has on our net interest margins, we employ a

proactive asset-liability management program, which includes strategic asset allocation and derivative strategies within a disciplined risk

management framework. These strategies seek to match the characteristics of our products, and to closely approximate the interest rate

sensitivity of the assets with the estimated interest rate sensitivity of the product liabilities. Our asset-liability management program also

helps manage duration gaps, currency and other risks between assets and liabilities through the use of derivatives. We adjust this dynamic

process as products change, as customer behavior changes and as changes in the market environment occur. As a result, our asset-liability

management process has permitted us to manage interest-sensitive products successfully through several market cycles.

Our interest rate exposure is also mitigated by our business mix, as we have relatively limited exposure to lines of business in which

net interest margin plays a more prominent role in product profitability, such as fixed annuities and universal life, which represents a

limited portion of our individual life business in force. In addition, within our Retirement business, a substantial portion of our stable value

account values have very low crediting rate floors.

Our Japanese insurance operations have experienced a prolonged low interest rate environment for many years. These operations issue

recurring payment and single premium products that are denominated in both Japanese yen and U.S. dollars, as well as fixed annuity

products that are denominated in U.S. dollars. For the Japanese yen-denominated products, the exposure to decreased interest rates is

limited as our Japanese insurance operations have considered the prolonged low interest rate environment in product pricing, and a rigorous

asset-liability management program, which includes our duration management and crediting rate strategies, further limits our exposure. For

the U.S. dollar-denominated recurring payment products, our exposure to low interest rates in the U.S. is also limited by our asset-liability

management program. For the U.S. dollar-denominated single premium and fixed annuity products, the risk of reduced interest rates is

limited, as new fixed annuity contracts are re-priced frequently and pricing for other products is reviewed and updated regularly to reflect

current market interest rates.

Current Developments

Effective January 1, 2012, the Company adopted, retrospectively, the amended authoritative guidance issued by the Financial

Accounting Standards Board (“FASB”) to address which costs relating to the acquisition of new or renewal insurance contracts qualify for

deferral. The Company has applied the retrospective method of adoption. In addition, in December 2012, the Company adopted

retrospectively a change in method of applying an accounting principle for the Company’s pension plans. The change in accounting method

relates to the calculation of market related value of pension plan assets used to determine net periodic pension cost. All historical financial

information presented has been revised to reflect these changes. For further information, see “—Accounting Policies and

Pronouncements—Adoption of New Accounting Pronouncements” and Note 2 to the Consolidated Financial Statements.

On June 1, 2012, we announced the signing of an agreement with General Motors Co., pursuant to which we would assume certain of

its pension benefit obligations to U.S. salaried retiree plan participants and beneficiaries that are covered by the agreement. At closing on

November 1, 2012, we issued a non-participating group annuity contract to the General Motors Salaried Employees Pension Trust, and

assumed responsibility for providing specified benefits to certain participants. In addition, on October 17, 2012, we signed an agreement

with Verizon Communications Inc., pursuant to which we will assume certain of its pension benefit obligations to U.S. salaried retiree plan

participants and beneficiaries that are covered by the agreement. At closing on December 10, 2012, we issued a non-participating group

annuity contract to the Verizon Management Pension Plan, and assumed responsibility for providing specified benefits to certain

participants. These pension risk transfer transactions significantly expand the size of our existing payout annuity business.

On June 12, 2012, Prudential Financial’s Board of Directors authorized the Company to repurchase at management’s discretion up to

$1.0 billion of its outstanding Common Stock during the period from July 1, 2012 through June 30, 2013. As of December 31, 2012,

2.7 million shares of our Common Stock were repurchased under this authorization for a total cost of $150 million. The Company

exhausted an earlier $1.5 billion share repurchase authorization established in June 2011 including 8.8 million shares purchased in the first

six months of 2012 at a total cost of $500 million.

14 Prudential Financial, Inc. 2012 Annual Report