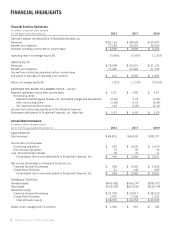

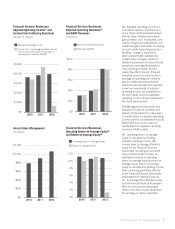

Prudential 2012 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2012 Prudential annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

lower returns to us on this existing block of business will continue to affect our consolidated results of operations for many years. Our

Common Stock reflects the performance of our Financial Services Businesses, but there can be no assurance that the market value of the

Common Stock will reflect solely the performance of these businesses.

See “Risk Factors” included in Prudential Financial’s 2012 Annual Report on Form 10-K for a discussion of risks that have affected

and may affect in the future our business, results of operations or financial condition, cause the trading price of our Common Stock to

decline materially or cause our actual results to differ materially from those expected or those expressed in any forward looking statements

made by or on behalf of the Company.

Executive Summary

Prudential Financial, a financial services leader with approximately $1.060 trillion of assets under management as of December 31,

2012, has operations in the United States, Asia, Europe and Latin America. Through our subsidiaries and affiliates, we offer a wide array of

financial products and services, including life insurance, annuities, retirement-related services, mutual funds, and investment management.

We offer these products and services to individual and institutional customers through one of the largest distribution networks in the

financial services industry.

Industry Trends

Our U.S. and international businesses are impacted by financial markets, economic conditions, regulatory oversight, and a variety of

trends that affect the industries where we compete.

U.S. Businesses

Financial and Economic Environment. Although economic and financial conditions continue to show signs of improvement, global

market conditions and uncertainty continue to be factors in the markets in which we operate. This uncertainty, particularly in the equity

markets, has led to, among other things, increased demand for guaranteed retirement income, fixed income and stable value products, and

defined benefit risk transfer solutions.

The continued low interest rate environment continues to negatively impact our portfolio income yields, as discussed further below,

and continued high unemployment rates and limited growth in salaries also continue to be factors impacting certain business drivers,

including contributions to defined contribution plans and the costs of group disability claims.

Regulatory Environment. Financial market dislocations have produced, and are expected to continue to produce, extensive changes

in existing laws and regulations, and regulatory frameworks applicable to our businesses. In addition, state insurance laws regulate all

aspects of our U.S. insurance businesses and our insurance products are substantially affected by federal and state tax laws. Insurance

regulators have begun to implement significant changes in the way in which industry participants must determine statutory reserves and

statutory capital, particularly for products with embedded options and guarantees such as variable annuities and universal life products with

secondary guarantees.

Demographics. Income protection, wealth accumulation and the needs of retiring baby boomers continue to shape the insurance

industry. Retirement security is one of the most critical issues in the U.S. for individuals and the investment professionals and institutions

that support them. The risk and responsibility of retirement savings continues to shift to employees, away from the government and

employers. Life insurance ownership among U.S. households has reached its lowest point in fifty years, with consumers citing other

financial priorities and cost of insurance as reasons for the lack of coverage.

Competitive Environment. For the annuities business, traditional competitors continue to take actions to either exit the marketplace

or de-risk products in response to recent market volatility. New non-traditional competitors are beginning to enter this marketplace. In

2012, we implemented modifications to scale back benefits and increase pricing for certain product features. We believe our current

product offerings are competitively positioned and that our differentiated risk management strategies will provide us with an attractive risk

and profitability profile. All of our new variable annuity sales, as well as a significant portion of our in force business, where an optional

living benefit has been elected, include an automatic rebalancing feature, which is a feature that is valued in the variable annuity market.

Our retirement and asset management businesses compete on price, service and investment performance. The full service retirement

markets are mature, with few dominant players. We have seen a trend toward unbundling of the purchase decision related to the

recordkeeping and investment offerings, where the variety of available funds and their performance are the key selection criteria of plan

sponsors and intermediaries. Additionally, changes in the regulatory environment have driven more transparent fee disclosures, which have

heightened pricing pressures and may accelerate the trend toward unbundling of services. Market disruption and rating agency downgrades

have caused some of our institutional investment product competitors to withdraw from the market, creating significant growth

opportunities for us in certain markets, including the investment-only stable value market. The recovery of the equity, fixed income, and

commercial real estate markets has positively impacted asset managers by increasing assets under management and corresponding fee

levels. In addition, institutional fixed income managers have generally experienced positive flows as investors have re-allocated assets into

fixed income to reduce risk, including the reduction of risk in pension plans. In 2012, we closed two significant pension risk transfer

transactions, which potentially changes the landscape for how plan sponsors consider their pension risk alternatives. The longevity risk

associated with these transactions complements our mortality risk businesses.

The individual life and group life and disability markets are mature and, due to the large number of competitors, competition is driven

mainly by price and service. The economy has exacerbated pressure on pricing, creating a challenge of maintaining pricing discipline. In

the individual life market, many of our competitors took pricing actions in 2012 in response to the low interest rate environment, following

our own price increases implemented in 2009 and 2010. Our individual life sales in 2012 benefited from a strong competitive position as a

result of these competitor actions. Maintaining this competitive positioning is dependent on sources of financing for the reserves associated

with this business and timely utilization of the associated tax benefits. For group products, rate guarantees have become the industry norm,

12 Prudential Financial, Inc. 2012 Annual Report