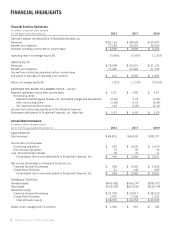

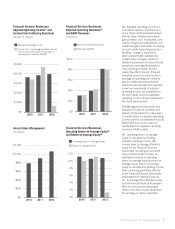

Prudential 2012 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2012 Prudential annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

with rate guarantee durations trending upward, primarily for group life insurance, as a general industry practice. There is also an increased

demand from clients for bundling of products and services to streamline administration and save costs by dealing with fewer carriers. As

employers are attempting to control costs and shift benefit decisions and funding to employees, who continue to value benefits offered in

the workplace, employee-pay (voluntary) product offerings and services are becoming increasingly important in the group market. For the

long-term care business, many companies, including Prudential, have taken actions in response to the continued low interest rate

environment including exiting the marketplace, seeking premium rate increases and changing plan designs. In 2012, we announced our

decision to cease sales of long-term care products reflecting our desire to focus our efforts on our core group life and disability lines of

business.

International Businesses

Financial and Economic Environment. Our international insurance operations, especially in Japan, continue to operate in the low

interest rate environment described below. However, the local market has adapted to the low rate environment in Japan. The continued low

interest rate environment in the U.S. may impact the attractiveness of U.S. dollar-denominated products in Japan relative to yen-

denominated products. We are also subject to financial impacts associated with movements in foreign currency rates, particularly the

Japanese yen. Fluctuations in the value of the yen will continue to impact the relative attractiveness of non-yen products marketed in Japan.

Regulatory Environment. In April 2012, Japanese tax law changed to reduce deductibility of premiums on certain insurance

products. This resulted in dislocations in the tax sensitive marketplace and elevated sales of these products prior to the effective date of the

tax law change and reduced sales thereafter. The Financial Services Agency, the insurance regulator in Japan, has implemented revisions to

the solvency margin requirements for certain assets and has changed the manner in which an insurance company’s core capital is

calculated. These changes were effective for the fiscal year ending March 31, 2012. We anticipate further changes in solvency regulation

from jurisdiction to jurisdiction based on regulatory developments in the U.S., the European Union, and recommendations by an

international standard setting body for the insurance regulators, as well as regulatory requirements for those companies deemed to be

systemically important financial institutions, or SIFIs, in the U.S. or abroad. In addition, local regulators, including in Japan, may apply

heightened scrutiny to non-domestic companies. Internationally, regulators are also increasingly adopting measures to provide greater

consumer protection and privacy rights.

Demographics. Japan has an aging population as well as a large pool of household assets invested in low yielding deposit and

savings vehicles. The aging of Japan’s population as well as strains on government pension programs have led to a growing demand for

insurance products with a significant savings element to meet savings and retirement needs as the population transitions to retirement.

These products have higher premiums with more of a savings component. We are seeing a similar shift to retirement oriented products in

Korea and Taiwan, each of which also has an aging population.

Competitive Environment. The life insurance markets in Japan and Korea are mature. We generally compete more on distribution

capabilities and service provided to customers than on price. The aging of Japan’s population creates an increasing need for product

innovation, introducing insurance products which allow for savings and income as the population transitions to retirement. In our Japanese

bank channel we experienced elevated sales of yen-denominated single premium reduced death benefit whole life products during periods

when competitors capped their sales of similar investment-oriented products. The ability to sell through multiple and complementary

distribution channels is a competitive advantage. However, competition for sales personnel as well as access to third party distribution

channels is intense.

Impact of Low Interest Rate Environment

The low interest rate environment in the U.S. has resulted in our current reinvestment yields being lower than the overall portfolio

income yield, primarily for our investments in fixed maturity securities and commercial mortgage loans. With the Federal Reserve Board’s

intention to keep interest rates low through at least 2014, our portfolio income yields are expected to continue to decline in future periods.

For the domestic Financial Services Businesses’ general account, we expect annual scheduled payments and pre-payments to be

approximately 10% of the fixed maturity security and commercial mortgage loan portfolios through 2014. The domestic Financial Services

Businesses’ general account has approximately $152 billion of such assets (based on net carrying value) as of December 31, 2012. As these

assets mature, the current average portfolio income yield for fixed maturities and commercial mortgage loans of approximately 5% is

expected to decline due to reinvesting in a lower interest rate environment.

The reinvestment of scheduled payments and pre-payments at rates below the current portfolio yield, including in some cases, at rates

below those guaranteed under our insurance contracts, will impact future operating results to the extent we do not, or are unable to, reduce

crediting rates on in-force blocks of business, or effectively utilize other asset-liability management strategies described below, in order to

maintain current net interest margins. As of December 31, 2012, our domestic Financial Services Businesses have approximately $143

billion of insurance liabilities and policyholder account balances. Of this amount, approximately $41 billion represents contracts with

guaranteed minimum crediting rates. The following table sets forth our contracts in the domestic Financial Services Businesses with

guaranteed minimum crediting rates, and the related range of the difference between interest rates being credited to contractholders on

these balances as of December 31, 2012 and the respective minimum guaranteed rates.

Account

Value % of Total

(in billions)

Contracts at guaranteed minimum crediting rate ............................................................... $21.9 53%

Contracts above guaranteed minimum crediting rate by:

0% – 0.49% ........................................................................................ 2.8 7

0.5% – 1% ......................................................................................... 2.0 5

greater than 1% ..................................................................................... 14.3 35

Total contracts with minimum guaranteed crediting rates ................................................ $41.0 100%

Prudential Financial, Inc. 2012 Annual Report 13