Office Depot 2010 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2010 Office Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

base rate (defined as the higher of the Prime Rate (as announced by the Agent) and the Federal Funds Rate plus

1/2 of 1%) or (ii) the Adjusted LIBOR Rate (defined as the LIBOR Rate as adjusted for statutory revenues) plus,

in either case, a certain margin based on the aggregate average availability under the Facility. The Agreement

also contains representations, warranties, affirmative and negative covenants, and default provisions which are

conditions precedent to borrowing. The most significant of these covenants and default provisions include a

capital expenditure limitation of $500 million in any fiscal year and limitations in certain circumstances on

acquisitions, dispositions, share repurchases and the payment of cash dividends.

On March 26, 2010, the company executed a second amendment to its asset based credit facility. This second

amendment amends the facility by, among other things, allowing the company to make certain restricted

payments, including the payment of cash dividends on preferred stock and make share repurchases, in an

aggregate amount of $50 million per fiscal year, subject to the maintenance of certain minimum liquidity

conditions, removing the ability of the company to elect one- or two-month interest periods with respect to its

LIBOR borrowings, making certain technical amendments to permit the company to issue unsecured or

subordinated convertible debt securities, allowing the company and its subsidiaries to enter into certain internal

tax restructuring transactions subject in certain circumstances to various conditions, and waiving certain technical

events of default, including written notice of certain events to JP Morgan Chase Bank, N.A. (the “Agent”) under

the asset based credit facility and certain related security agreements. The company was in compliance with all

applicable financial covenants at December 25, 2010.

The company has never declared or paid cash dividends on its common stock. All 2010 dividends on its preferred

stock were paid in cash as permitted under this agreement.

The Facility also includes provisions whereby if the global availability is less than $218.8 million, or the

European availability is below $37.5 million, the company’s cash collections go first to the Agent to satisfy

outstanding borrowings. Further, if total availability falls below $187.5 million, a fixed charge coverage ratio test

is required which, based on current forecasts, could effectively eliminate additional borrowing under the Facility.

Any event of default that is not cured within the permitted period, including non-payment of amounts when due,

any debt in excess of $25 million becoming due before the scheduled maturity date, or the acquisition of more

than 40% of the ownership of the company by any person or group, could result in a termination of the Facility

and all amounts outstanding becoming immediately due and payable.

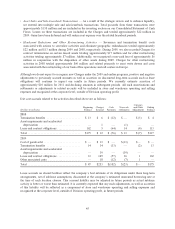

At December 25, 2010, the company had approximately $674 million of available credit under the Facility. At

December 25, 2010, $52.5 million was outstanding under the Facility and there were letters of credit outstanding

under the Facility totaling approximately $119 million. An additional $0.2 million of letters of credit were

outstanding under separate agreements. Average borrowings under the Facility in the fourth quarter of 2010 were

approximately $33.9 million at an average interest rate of 3.56%. We did not borrow under the Facility during

the first three quarters of 2010.

At December 25, 2010, we had short-term borrowings of $1.2 million. These borrowings primarily represent

outstanding balances under various local currency credit facilities for our international subsidiaries that had an

effective interest rate at the end of the year of approximately 6%. The majority of these short-term borrowings

represent outstanding balances on uncommitted lines of credit, which do not contain financial covenants.

In August 2003, we issued $400 million senior notes due August 2013. These notes are not callable and bear

interest at the rate of 6.25% per year, to be paid on February 15 and August 15 of each year. The notes contain

provisions that, in certain circumstances, place financial restrictions or limitations on us. Simultaneous with

completing the offering, we liquidated a treasury rate lock. The proceeds are being amortized over the term of the

issue, reducing the effective interest rate to 5.86%. During 2004, we entered into a series of fixed-to-variable

interest rate swap agreements as fair value hedges on the $400 million of notes. The swap agreements were

terminated during 2005.

Capital lease obligations primarily relate to buildings and equipment as indicated in Note E.

49