Navy Federal Credit Union 2012 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2012 Navy Federal Credit Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35

|

|

Navy Federal Credit Union38 Leading with Vision. Achieving Results. 39

2012 Financial Section

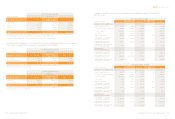

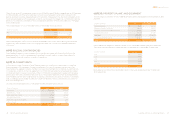

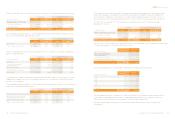

NOTE 20: FAIR VALUE MEASUREMENT

Eective with the adoption of ASC 820-10, Fair Value Measurements and Disclosures, Navy Federal

determines the fair values of its financial instruments based on the fair value hierarchy established

in that standard, which requires an entity to maximize the use of quoted prices and observable inputs

when measuring fair value. A description of the fair value hierarchy is as follows:

> Level 1—Valuation is based upon quoted prices for identical instruments traded in active markets.

> Level 2—Valuation is based upon observable inputs, such as quoted prices for similar instruments in

active markets, quoted prices for identical or similar instruments in markets that are not active, and

model-based valuation techniques for which all significant assumptions are observable in the market.

> Level 3—Valuation is based upon unobservable inputs that are supported by little or no market activity

and are significant to the fair value of the instrument. Valuation is typically performed using pricing

models, discounted cash flow methodologies, or similar techniques, which incorporate management’s

own estimates of assumptions that market participants would use in pricing the instrument or

valuations that require significant management judgment or estimation.

Certain assets and liabilities may be required to be measured at fair value on a non-recurring basis.

These non-recurring fair value measurements usually result from the application of lower of cost or

market accounting or the write-down of individual assets due to impairment.

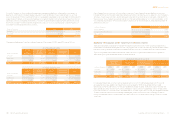

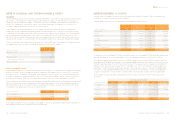

The following is a description of the valuation methodologies used by Navy Federal for the assets

measured at fair value:

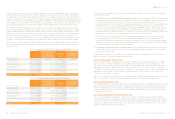

Securities Available-for-Sale (AFS)

Navy Federal receives pricing for AFS securities from a third-party pricing service. These securities

are classified as Level 2 in the fair value hierarchy. The following is a description of the valuation

methodologies used for these securities:

> Residential and Commercial Mortgage-backed Securities—Residential and commercial mortgage-

backed securities are valued either based on similar assets in the marketplace and the vintage of

the underlying collateral, or at the closing price reported in the active market in which the individual

security is traded.

> Federal Agency Securities, Treasury Securities, Municipal Securities, and Bank Notes—Federal agency

securities, treasury securities, municipal securities, and bank notes are valued based on similar assets

in the marketplace and the vintage of the underlying collateral, or at the closing price reported in the

active market in which the individual security is traded.

Mortgage Servicing Rights (MSRs)

MSRs do not trade in an active, open market with readily observable prices. Accordingly, Navy Federal

obtains the fair value of the MSRs using a third-party pricing provider. The provider uses a combination

of market and income valuation methodologies. All assumptions are market driven. Once the preliminary

results are complete, they are further calibrated to observable market transactions, when they exist.

Therefore, MSRs are classified within Level 3 of the fair value hierarchy, as the valuation is model driven

and primarily based on unobservable inputs.

Derivative Commitments—Assets and Liabilities

Navy Federal uses derivative commitments to hedge against interest rate risk. These derivatives (assets

and liabilities) are valued using quoted market prices of similar assets and are classified within Level 2

of the fair value hierarchy.

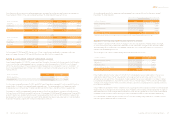

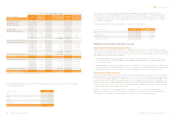

All benefits are paid from Navy Federal assets and are in compliance with all federal laws and

regulations. Navy Federal accrued $2.9 million and $1.3 million in the years ended December 31, 2012

and 2011, respectively.

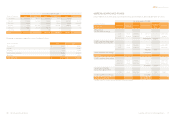

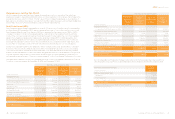

NOTE 18: RELATED PARTY TRANSACTIONS

In the normal course of business, Navy Federal extends loans to credit union ocials. The total principal

amount of loans extended to ocials during 2012 and 2011 was $35.3 million and $33.2 million, respectively.

Credit union ocials are defined as volunteer members of the Board of Directors and board committees,

and employees with the title of Vice President and above.

Navy Federal’s wholly owned subsidiary, NFFG, had $25.5 million and $29.6 million on deposit with

Navy Federal as of December 31, 2012 and 2011, respectively.

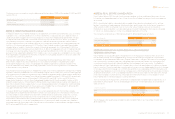

NOTE 19: RESERVES AND UNDIVIDED EARNINGS

Navy Federal is subject to regulatory capital requirements administered by the NCUA. Failure to meet

minimum capital requirements can initiate certain mandatory and possibly additional discretionary

actions by regulators that, if undertaken, could have a direct material eect on Navy Federal’s

consolidated financial statements. Under capital adequacy regulations and the regulatory framework

for prompt corrective action, Navy Federal must meet specific capital requirements that involve

quantitative measures of Navy Federal’s assets, liabilities, and certain commitments as calculated under

GAAP. Navy Federal’s capital amounts and net worth classification are also subject to qualitative

judgments by the regulators about components, risk weightings, and other factors.

Quantitative measures established by regulation to ensure capital adequacy require Navy Federal to

maintain minimum amounts and ratios of net worth to total assets. Credit unions are also required to

calculate a risk-based net worth (RBNW) requirement that establishes whether the credit union will

be considered “complex” under the regulatory framework. A credit union is defined as “complex” if

the credit union’s quarter-end total assets exceed ten million dollars ($10,000,000) and its RBNW

requirement exceeds six percent (6.0%). Navy Federal’s RBNW requirement as of December 31, 2012

and 2011 was 6.1% and 6.4%, respectively, which exceeds the regulatory threshold of 6.0% and places

Navy Federal in the “complex” category. There is no impact to Navy Federal based on the complex

designation because their statutory net worth ratio qualifies us as “well capitalized” by NCUA standards,

and our statutory net worth exceeds their RBNW requirement.

The NCUA categorized Navy Federal as “well capitalized” under the regulatory framework for prompt

corrective action with a net worth-to-assets ratio of 10.9% and 10.6% as of December 31, 2012 and 2011,

respectively. Net worth for this calculation is defined as undivided earnings plus regular and capital

reserves. To be categorized as “well capitalized,” Navy Federal must maintain a minimum net worth

ratio of 7.0%. There are no conditions or events since that notification that management believes have

changed the institution’s category.