Bed, Bath and Beyond 2004 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2004 Bed, Bath and Beyond annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

|

|

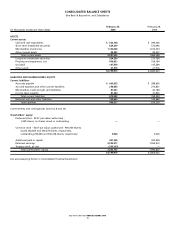

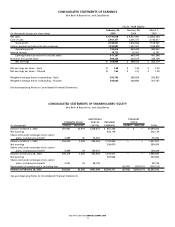

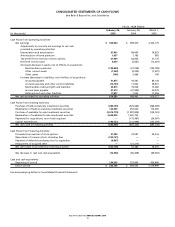

BED BATH & BEYOND ANNUAL REPORT 2004

8

Inventory Valuation: Merchandise inventories are stated at the lower of cost or market. Inventory costs for BBB and

Harmon are calculated using the retail inventory method and inventory cost for CTS is calculated using the first-in,

first-out cost method. Under the retail inventory method, the valuation of inventories at cost and the resulting gross

margins are calculated by applying a cost-to-retail ratio to the retail value of inventories.

At any one time, inventories include items that have been written down to the Company’s best estimate of their

realizable value. Factors considered in estimating realizable value include the age of merchandise and anticipated

demand. Actual realizable value could differ materially from this estimate based upon future customer demand or

economic conditions.

The Company estimates its reserve for shrinkage throughout the year, based on historical shrinkage. Actual shrinkage

is recorded at year-end based upon the results of the Company’s physical inventory count. Historically, the Company’s

shrinkage has not been volatile.

Impairment of Long-Lived Assets: The Company reviews long-lived assets for impairment annually or when events

or changes in circumstances indicate the carrying value of these assets may exceed their current fair values. If it is

determined that an impairment loss has occurred, the loss would be recognized during that period. The impairment

loss is calculated as the difference between asset carrying values and the estimated future undiscounted cash flows.

The Company has not historically had any material impairment of long-lived assets. In the future, if events or market

conditions affect the estimated cash flows generated by the Company’s long-lived assets to the extent that an asset is

impaired, the Company will adjust the carrying value of these assets in the period in which the impairment occurs.

Goodwill and Other Indefinitely Lived Intangible Assets: The Company reviews goodwill and other intangibles that

have indefinite lives for impairment annually or when events or changes in circumstances indicate the carrying value

of these assets might exceed their current fair values. Impairment testing is based upon the best information avail-

able including estimates of fair value which incorporate assumptions marketplace participants would use in making

their estimates of fair value. The Company has not historically recorded an impairment to its goodwill and other

indefinitely lived intangible assets. In the future, if events or market conditions affect the estimated fair value to

the extent that an asset is impaired, the Company will adjust the carrying value of these assets in the period in which

the impairment occurs.

Income Taxes: The Company accounts for its income taxes using the asset and liability method. Deferred tax assets

and liabilities are recognized for the future tax consequences attributable to the differences between the financial

statement carrying amounts of existing assets and liabilities and their respective tax bases and operating loss and

tax credit carryforwards. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to

taxable income in the year in which those temporary differences are expected to be recovered or settled. The effect

on deferred tax assets and liabilities of a change in tax rates is recognized in earnings in the period that includes the

enactment date.

Judgment is required in determining the provision for income taxes and related accruals, deferred tax assets and

liabilities. In the ordinary course of business, there are transactions and calculations where the ultimate tax outcome

is uncertain. Additionally, the Company’s tax returns are subject to audit by various tax authorities. Although the

Company believes that its estimates are reasonable, actual results could differ from these estimates.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

(continued)