Bed, Bath and Beyond 2000 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2000 Bed, Bath and Beyond annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24

|

|

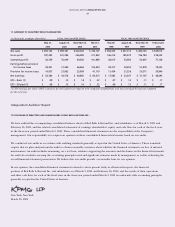

BED BATH & BEYOND ANNUAL REPORT 2000

15

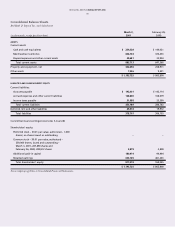

I. PROPERTY AND EQUIPMENT

Property and equipment are stated at cost. Depreciation is

computed primarily using the straight-line method over the

estimated useful lives of the assets (five to ten years for furniture,

fixtures and equipment and three to five years for computer

equipment). Leasehold improvements are amortized using the

straight-line method over the lesser of their estimated useful life

or the life of the lease.

The cost of maintenance and repairs is charged to earnings as

incurred; significant renewals and betterments are capitalized.

Maintenance and repairs amounted to $28.4 million, $24.2

million and $17.3 million for fiscal 2000, 1999 and 1998,

respectively.

J. DEFERRED RENT

The Company accounts for scheduled rent increases contained

in its leases on a straight-line basis over the noncancelable lease

term. Deferred rent amounted to $23.3 million and $20.0

million as of March 3, 2001 and February 26, 2000, respectively.

K. SHAREHOLDERS’ EQUITY

In July 2000 and June 1998, the Board of Directors approved

two-for-one splits of the Company’s common stock effected in

the form of 100% stock dividends. The stock dividends were

distributed on August 11, 2000 and July 31, 1998, respectively, to

shareholders of record on July 28, 2000 and July 10, 1998,

respectively.

Unless otherwise stated, all references to common shares

outstanding and net earnings per share are on a post-split basis.

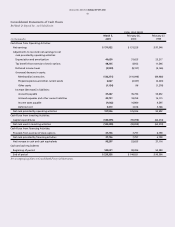

L. REVENUE RECOGNITION

The Company recognizes revenue at the time of sale of

merchandise to its customers. Revenues from the sale of gift

cards, gift certificates and store credits are recognized when

redeemed. A provision for merchandise returns is provided in

the period that the related sales are recorded.

M. PREOPENING EXPENSES

Expenses associated with new or expanded stores are charged to

earnings as incurred.

N. ADVERTISING COSTS

Expenses associated with store advertising are charged to

earnings as incurred.

O. INCOME TAXES

The Company files a consolidated Federal income tax return.

Separate state income tax returns are filed with each state in

which the Company conducts business.

The Company accounts for its income taxes using the asset and

liability method. Deferred tax assets and liabilities are

recognized for the future tax consequences attributable to the

differences between the financial statement carrying amounts of

existing assets and liabilities and their respective tax bases and

operating loss and tax credit carryforwards. Deferred tax assets

and liabilities are measured using enacted tax rates expected to

apply to taxable income in the year in which those temporary

differences are expected to be recovered or settled. The effect

on deferred tax assets and liabilities of a change in tax rates is

recognized in earnings in the period that includes the

enactment date.

P. FAIR VALUE OF FINANCIAL INSTRUMENTS

The Company’s financial instruments include cash and cash

equivalents, accounts payable and accrued expenses and other

current liabilities. The book value of cash and cash equivalents,

accounts payable and accrued expenses and other current

liabilities are representative of their fair values due to the short-

term maturity of these instruments.

Q. IMPAIRMENT OF LONG-LIVED ASSETS

The Company periodically reviews long-lived assets for

impairment by comparing the carrying value of the assets with

their estimated future undiscounted cash flows. If it is

determined that an impairment loss has occurred, the loss would

be recognized during that period. The impairment loss is

calculated as the difference between asset carrying values and

the present value of the estimated net cash flows. The Company

does not believe that any material impairment currently exists

related to its long-lived assets.

R. USE OF ESTIMATES

The preparation of financial statements in conformity with

generally accepted accounting principles requires management

to make estimates and assumptions that affect the reported

amounts of assets and liabilities and disclosure of contingent

assets and liabilities as of the date of the financial statements and

the reported amounts of revenues and expenses during the

reporting period. Actual results could differ from these

estimates.