Abercrombie & Fitch 2007 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2007 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

|

|

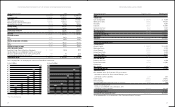

reserve was $5.4 million, $6.8 million and $10.0 million at February

2, 2008, February 3, 2007 and January 28, 2006, respectively.

Additionally, as part of inventory valuation, an inventory shrink

estimate is made each period that reduces the value of inventory for lost

or stolen items. The Company performs physical inventories throughout

the year and adjusts the shrink reserve accordingly. The shrink reserve

was $11.5 million, $7.7 million and $3.8 million at February 2, 2008,

February 3, 2007 and January 28, 2006, respectively.

Inherent in the retail method calculation are certain significant

judgments and estimates including, among others, markdowns and

shrinkage, which could significantly impact the ending inventory

valuation at cost as well as the resulting gross margins. An increase

or decrease in the inventory shrink estimate of 10% would not have a

material impact on the Company’s results of operations. Management

believes this inventory valuation method is appropriate since it preserves

the cost-to-retail relationship in ending inventory.

PROPERTY AND EQUIPMENT Depreciation and amortization

of property and equipment are computed for financial reporting

purposes on a straight-line basis, using service lives ranging principally

from 30 years for buildings; the lesser of the useful life of the asset,

which ranges from three to 15 years, or the term of the lease for leasehold

improvements; the lesser of the useful life of the asset, which ranges

from three to seven years, or the term of the lease when applicable for

information technology; and three to 20 years for other property and

equipment. The cost of assets sold or retired and the related accu-

mulated depreciation or amortization are removed from the accounts

with any resulting gain or loss included in net income. Maintenance

and repairs are charged to expense as incurred. Major remodels and

improvements that extend service lives of the assets are capitalized.

Long-lived assets are reviewed at the store level periodically for

impairment or whenever events or changes in circumstances indicate

that full recoverability of net assets through future cash flows is in

question. Factors used in the evaluation include, but are not limited

to, management’s plans for future operations, recent operating results

and projected cash flows.

INCOME TAXES Income taxes are calculated in accordance with

SFAS No. 109,“Accounting for Income Taxes,” which requires the use

of the asset and liability method. Deferred tax assets and liabilities

are recognized based on the difference between the financial statement

carrying amounts of existing assets and liabilities and their respective

tax bases. Deferred tax assets and liabilities are measured using current

enacted tax rates in effect for the years in which those temporary dif-

ferences are expected to reverse. Inherent in the measurement of

deferred balances are certain judgments and interpretations of enacted

tax law and published guidance with respect to applicability to the

Company’s operations. A valuation allowance is established against

deferred tax assets when it is more likely than not that some portion

or all of the deferred tax assets will not be realized. The Company has

recorded a valuation allowance against the deferred tax asset arising

from the net operating loss of a foreign subsidiary. No other valuation

allowances have been provided for deferred tax assets. The effective

tax rate utilized by the Company reflects management’s judgment of

expected tax liabilities within the various tax jurisdictions.

In June 2006, the FASB issued Financial Accounting Standards

Board Interpretation (“FIN”) No. 48, “Accounting for Uncertainty in

Income Tax – an interpretation of FASB Statement No. 109.” FIN 48

clarifies the accounting for uncertainty in income taxes recognized in

a company’s financial statements in accordance with SFAS No. 109,

“Accounting for Income Taxes.” This interpretation prescribes a rec-

ognition threshold and measurement attribute for the financial statement

recognition and measurement of a tax position taken or expected to

be taken in a tax return. This interpretation also provides guidance

on derecognition, classification, interest and penalties, accounting in

interim periods, disclosure and transition. The Company recognizes

accrued interest and penalties related to unrecognized tax benefits as

a component of tax expense.

The provision for income taxes is based on the current estimate of

the annual effective tax rate adjusted to reflect the tax impact of items

discrete to the quarter. The Company records tax expense or benefit that

does not relate to ordinary income in the current fiscal year discretely

in the period in which it occurs pursuant to the requirements of APB

Opinion No. 28, “Interim Financial Reporting” and FIN 18,

“Accounting for Income Taxes in Interim Periods – an Interpretation of

APB Opinion No. 28.” Examples of such types of discrete items

include, but are not limited to, changes in estimates of the outcome

of tax matters related to prior years, provision-to-return adjustments,

tax-exempt income and the settlement of tax audits.

FOREIGN CURRENCY TRANSLATION The majority of the

Company’s international operations use local currencies as the func-

tional currency. In accordance with SFAS No. 52, “Foreign Currency

Translation”, assets and liabilities denominated in foreign currencies

were translated into U.S. dollars (the reporting currency) at the

exchange rate prevailing at the balance sheet date. Equity accounts

denominated in foreign currencies were translated into U.S. dollars

at historical exchange rates. Revenues and expenses denominated in

foreign currencies were translated into U.S. dollars at the monthly

average exchange rate for the period. Gains and losses resulting from

foreign currency transactions are included in the results of operations;

whereas, translation adjustments are reported as an element of other

comprehensive income in accordance with SFAS No. 130, “Reporting

Comprehensive Income”.

CONTINGENCIES In the normal course of business, the

Company must make continuing estimates of potential future legal

obligations and liabilities, which requires the use of management’s

judgment on the outcome of various issues. Management may also

use outside legal advice to assist in the estimating process. However,

the ultimate outcome of various legal issues could be different than

management estimates, and adjustments may be required.

EQUITY COMPENSATION EXPENSE Prior to January 29,

2006, the Company reported share-based compensation through the

disclosure-only requirements of SFAS No. 123, “Accounting for Stock-Based

Compensation” (“SFAS No.123”), as amended by SFAS No. 148,

“Accounting for Stock-Based Compensation–Transition and

Disclosure–an Amendment of FASB Statement No. 123,” but elected to

measure compensation expense using the intrinsic value method in

accordance with Accounting Principles Board (“APB”) Opinion No.

25, “Accounting for Stock Issued to Employees”, for which no expense

was recognized for stock options if the exercise price was equal to the

market value of the underlying Common Stock on the date of grant,

and provided the required pro forma disclosures in accordance with

SFAS No. 123, as amended.

21

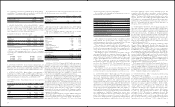

The remaining $51.7 million was used for projects at the home office,

including home office improvements, information technology invest-

ments, DC improvements and other projects.

Lessor construction allowances are an integral part of the decision

making process for assessing the viability of new store locations. In

making the decision whether to invest in a store location, the

Company calculates the estimated future return on its investment

based on the cost of construction, less any construction allowances to

be received from the landlord. The Company received $43.4 million,

$49.4 million and $42.3 million in construction allowances during

Fiscal 2007, Fiscal 2006 and Fiscal 2005, respectively.

During Fiscal 2008, the Company anticipates capital expenditures

between approximately $420 million and $425 million. Approximately

$300 million of this amount is allocated to new store construction and

full store remodels, including $55 million allocated for the Hollister

flagship in the SoHo area of New York City, the Abercrombie & Fitch

flagships in Europe and Japan and the four new Hollister mall-based

U.K. stores. Approximately $50 million is expected to be allocated to

refresh existing stores. The store refreshes will include new floors,

sound systems and fixture replacements at Abercrombie & Fitch and

abercrombie stores. In addition, Hollister store refreshes will include

the addition of video walls and the refitting of lighting and shelving

to accommodate the rollout of the personal care product line. The

Company is planning approximately $73 million in capital expendi-

tures at the home office related to information technology investments,

new direct-to-consumer distribution and logistics systems and other

home office projects.

The Company intends to add approximately 760,000 gross square

feet of stores during Fiscal 2008, which will represent an increase of

approximately 10% over Fiscal 2007. The Company anticipates the

increase during Fiscal 2008 will be primarily due to the addition of

approximately 70 new Hollister stores, 16 new abercrombie stores,

three new Abercrombie & Fitch stores, six new RUEHL stores and 15

new Gilly Hicks stores.

During Fiscal 2008, the Company expects the average construction

cost per square foot, net of construction allowances, for non-flagship

Abercrombie & Fitch stores to remain flat compared to Fiscal 2007’s

cost of approximately $140; for new abercrombie stores to decrease

from Fiscal 2007’s cost of approximately $171 to approximately $148;

for new Hollister stores to decrease from Fiscal 2007’s cost of approx-

imately $131 to approximately $126; and for RUEHL to decrease from

Fiscal 2007’s cost of $267 to $257. The changes from Fiscal 2007’s

estimates for Hollister, abercrombie and RUEHL stores were driven

by a number of factors, including landlord allowance levels and lower

construction costs. The Company expects the average construction

cost per square foot, net of construction allowances, for new Gilly

Hicks stores to be approximately $392 in Fiscal 2008.

The Company expects initial inventory purchases for the stores to

average approximately $0.4 million, $0.2 million, $0.4 million, $0.5

million and $0.6 million per store for Abercrombie & Fitch, abercrombie,

Hollister, RUEHL and Gilly Hicks, respectively.

The Company expects that substantially all future capital expen-

ditures will be funded with cash from operations. In addition, the

Company has $250 million available, less outstanding letters of credit,

under its Amended Credit Agreement to support operations.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The Company’s discussion and analysis of its financial condition and

20

results of operations are based upon the Company’s consolidated

financial statements, which have been prepared in accordance with

accounting principles generally accepted in the U.S. (“GAAP”). The

preparation of these consolidated financial statements requires the

Company to make estimates and assumptions that affect the reported

amounts of assets, liabilities, revenues and expenses. Since actual results

may differ from those estimates, the Company revises its estimates

and assumptions as new information becomes available.

The Company’s significant accounting policies can be found in

Note 2, “Summary of Significant Accounting Policies”, of the Notes

to Consolidated Financial Statements. The Company believes that

the following policies are most critical to the portrayal of the

Company’s financial condition and results of operations.

REVENUE RECOGNITION The Company recognizes retail sales

at the time the customer takes possession of the merchandise. Direct-

to-consumer sales are recorded upon customer receipt of merchandise.

Amounts relating to shipping and handling billed to customers in a

sale transaction are classified as revenue and the related direct shipping

and handling costs are classified as stores and distribution expense.

Associate discounts are classified as a reduction of revenue. The Company

reserves for sales returns through estimates based on historical expe-

rience and various other assumptions that management believes to be

reasonable. The sales return reserve was $10.7 million, $8.9 million

and $8.2 million at February 2, 2008, February 3, 2007 and January

28, 2006, respectively.

The Company’s gift cards do not expire or lose value over periods

of inactivity. The Company accounts for gift cards by recognizing a

liability at the time a gift card is sold. The liability remains on the

Company’s books until the earlier of redemption (recognized as revenue)

or when the Company determines the likelihood of redemption is

remote (recognized as other operating income). The Company determines

the probability of the gift card being redeemed to be remote based on

historical redemption patterns and recognizes the remaining balance

as other operating income. At February 2, 2008 and February 3, 2007,

the gift card liabilities on the Company’s Consolidated Balance Sheets

were $68.8 million and $65.0 million, respectively.

The Company is not required by law to escheat the value of unre-

deemed gift cards to the states in which it operates. During Fiscal

2007, Fiscal 2006 and Fiscal 2005, the Company recognized other

operating income for adjustments to the gift card liability of $10.9

million, $5.2 million and $2.4 million, respectively.

INVENTORY VALUATION Inventories are principally valued

at the lower of average cost or market utilizing the retail method. The

Company determines market value as the anticipated future selling

price of the merchandise less a normal margin. An initial markup is

applied to inventory at cost in order to establish a cost-to-retail ratio.

Permanent markdowns, when taken, reduce both the retail and cost

components of inventory on hand so as to maintain the already estab-

lished cost-to-retail relationship. At first and third fiscal quarter end,

the Company reduces inventory value by recording a markdown

reserve that represents the estimated future anticipated selling price

decreases necessary to sell-through the current season inventory. At

second and fourth fiscal quarter end, the Company reduces inventory

value by recording a markdown reserve that represents the estimated

future selling price decreases necessary to sell-through any remaining

carryover inventory from the season just passed. The markdown