Abercrombie & Fitch 2004 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2004 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

|

|

stock at a cost of $434.7 million. The increase in working capital

in fiscal 2003 versus fiscal 2002 was the result of higher cash and

marketable securities.

The Company considers the following to be measures of liquidity

and capital resources:

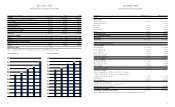

2004 2003 2002

Current ratio (current assets divided

by current liabilities) 1.58 2.42 2.32

Net cash provided by

operating activities (in thousands) $426,125 $342,545 $345,832

The increase in cash provided by operating activities in the 2004

fiscal year from the 2003 fiscal year was primarily driven by increas-

es in net income, accounts payable and accrued expenses, lessor con-

struction allowances received and income taxes. The increase in

accounts payable and accrued expenses was primarily due to the

accrual for the settlement of three related class action employment

discrimination lawsuits, for rent due to the net addition of 88 stores,

representing an increase of 574,000 gross square feet in 2004, and

increases in accounts payable for the purchase of merchandise.

The decrease in cash provided by operating activities in the 2003

fiscal year from the 2002 fiscal year was primarily driven by an

increase in inventories not offset by commensurate increases in net

income, lessor construction allowances, accounts payable and

accrued expenses. Inventories increased from the net addition of 103

stores representing an increase of 658,000 gross square feet in 2003.

Inventories at fiscal year-end were 3% higher on a per gross square

foot basis than at the end of the 2002 fiscal year.

The increase in cash provided by operating activities in the 2002

fiscal year from the 2001 fiscal year was primarily due to increases in

lessor construction allowances, accounts payable and accrued

expenses, and income taxes payable. Accounts payable increased in

the 2002 fiscal year due to both the increased level of inventory and

timing of payments. Accrued expenses increased in the 2002 fiscal

year primarily due to higher store expenses, consistent with the

increase in store openings. The increase in income taxes payable was

driven by higher pre-tax income and timing of payments.

The Company’s operations are seasonal in nature and typically

peak during the Back-to-School and Holiday selling periods.

Accordingly, cash requirements for inventory expenditures are highest

during these periods.

Cash outflows during the 2004 fiscal year related to investing

activities were primarily for purchase of marketable securities and

for capital expenditures related to new stores, the remodeling of

existing stores, expenditures in home office, improvements in the

distribution center, and information technology expenditures. See

“Capital Expenditures and Lessor Construction Allowances”.

Cash inflows from investing activities consisted of proceeds from

the sale of marketable securities. As of January 29, 2005, all invest-

ments had original maturities of less than 90 days and accordingly

were classified as cash equivalents.

Cash outflows during the 2003 fiscal year also related to purchas-

es of marketable securities and capital expenditures related to new

stores with approximately $35 million invested in the completion of

the home office expansion, improvements in the distribution center

and information technology expenditures for a new point-of-sale sys-

tem. This system was completely rolled-out to all stores during

the third quarter of the 2003 fiscal year. Cash inflows from investing

activities consisted of proceeds from the sale of marketable securities.

As of January 31, 2004, the Company held $464.7 million of mar-

ketable securities with original maturities of greater than 90 days.

Financing activities during the 2004, 2003 and 2002 fiscal years

consisted primarily of the repurchase of 11,150,500 shares, 4,401,000

shares, and 1,850,000 shares, respectively, of A&F’s Class A Common

Stock pursuant to previously authorized stock repurchase programs.

After the repurchases in 2004, the Company had 1,448,500 shares

available to repurchase as of January 29, 2005 of the 6,000,000

shares authorized by the Board of Directors in November 2004. In

addition to stock repurchases, financing activities also consisted of

stock option exercises, restricted stock issuances and overdrafts.

These overdrafts are outstanding checks reclassified from cash to

accounts payable.

Effective December 15, 2004, the Company entered into an

amended and restated $250 million syndicated unsecured credit

agreement, (the "Amended Credit Agreement") which extended

the original agreement, dated November 14, 2002 (the "Original

Credit Agreement"). The Amended Credit Agreement will expire

on December 15, 2009. The primary purpose of the Amended

Credit Agreement is for letters of credit (trade and stand-by) and

working capital. The Amended Credit Agreement has several

borrowing options, including interest rates that are based on the

agent banks “Alternate Base Rate,” or a LIBO rate. The facility

fees payable under the Amended Credit Agreement are based on

the Company’s ratio (the “leverage ratio”) of the sum of total debt

plus 600% of forward minimum rent commitments to consolidated

earnings before interest, taxes, depreciation, amortization and rent

(“EBITDAR”) for the trailing four-fiscal-quarter period. The

facility fees are projected to accrue at .175% on the committed

amounts per annum. The remaining terms of the Amended Credit

Agreement are similar to the Original Credit Agreement. Additional

details regarding the Credit Agreement can be found in the Notes

to Consolidated Financial Statements (see Note 8).

Letters of credit totaling approximately $49.6 million and

Abercrombie &FitchAbercrombie &Fitch

Back-to-School 2003. Shipping and handling revenue for the

corresponding periods was $10.2 million in 2003 and $7.8 million

in 2002. The direct-to-consumer business, including shipping and

handling revenue, accounted for 5.3% of net sales compared to

4.6% for the 2003 and 2002 fiscal years, respectively.

GROSS INCOME The Company’s gross income may not be com-

parable to those of other retailers since all significant costs related

to the Company’s distribution network, excluding direct shipping

costs related to the direct-to-consumer sales, are included in gen-

eral, administrative and store operating expenses (see “General,

Administrative and Store Operating Expenses” section below).

For the 2003 fiscal year, gross income increased to $716.9 mil-

lion from $655.7 million in the 2002 fiscal year. The gross income

rate in the 2003 fiscal year was 42.0% versus 41.1% in the 2002 fis-

cal year. The increase was driven by improvements in IMU that

were partially offset by increased buying and occupancy costs as a

percentage of net sales.

Buying and occupancy costs increased versus fiscal 2002, as a

percentage of net sales, due to the inability to leverage fixed expenses

with lower sales volume per average store.

GENERAL, ADMINISTRATIVE AND STORE OPERATING

EXPENSES Full year general, administrative and store operating

expenses were $385.8 million in the 2003 fiscal year versus $343.4

million in the 2002 fiscal year. The general, administrative and store

operating expense rate in the 2003 fiscal year was 22.6% versus

21.5% in the 2002 fiscal year. The increased rate in the 2003 fiscal

year resulted primarily from a drop in comparable store sales that

could not be offset by lower variable expenses per average store. In

addition, legal expense increased in the 2003 fiscal year compared to

the 2002 fiscal year as the Company reserved expected defense costs

for pending litigation. Partially offsetting these costs were improve-

ments in distribution center productivity, reduced expenses per order

in the direct-to-consumer business and reduced marketing expens-

es, as a percentage of net sales, due to savings from fewer direct mail

campaigns in the 2003 fiscal year.

Productivity at the distribution center, as measured in units

processed per labor hour, was 31% higher during the 2003 fiscal year

than during the 2002 fiscal year. Costs related to the distribution

center, excluding direct shipping costs related to the direct-to-con-

sumer sales, included in general, administrative and store operating

expenses were $19.3 million in the 2003 fiscal year compared to

$19.9 million in the 2002 fiscal year.

OPERATING INCOME For the 2003 fiscal year, operating income

was $331.2 million compared to $312.3 million for the 2002 fiscal

year. The operating income rate for the 2003 fiscal year was 19.4%

versus 19.6% in the 2002 fiscal year. The decline was attributable

to a higher general, administrative and store operating expense rate

due to the inability to leverage fixed costs on a comparable store

sales decrease. The increased expense rate was partially offset by a

gross income rate increase.

INTEREST INCOME AND INCOME TAXES Net interest income

for the 2003 fiscal year was $3.7 million compared to $3.8 million in

the 2002 fiscal year. The decline in the 2003 fiscal year net interest

income was due to lower interest rates. The Company continued to

invest in tax-free securities. The effective tax rate for the 2003 fiscal

year was 38.8% compared to 38.4% for the 2002 fiscal year.

NET INCOME AND NET INCOME PER SHARE Net income for

the 2003 fiscal year was $204.8 million versus $194.8 million for the

2002 fiscal year, an increase of 5.1%. Net income per weighted-

average diluted share was $2.06 in the fiscal 2003 year versus $1.94

in the fiscal 2002 year, an increase of 6.2%. The increase in net

income per diluted share outstanding versus net income was due to

the Company’s repurchase program in fiscal 2003. The Company

repurchased 4.4 million shares in fiscal 2003 versus 1.9 million

shares in fiscal 2002.

FINANCIAL CONDITION Continued growth in net income

resulted in higher cash provided by operating activities. A more

detailed discussion of liquidity, capital resources and capital

requirements follows.

LIQUIDITY AND CAPITAL RESOURCES The Company believes

cash provided by operating activities and cash on hand will provide

adequate resources to support operations, including projected growth,

seasonal requirements and capital expenditures. Furthermore, the

Company expects that cash from operating activities will fund

dividends currently being paid at a rate of $0.125 per quarter. The

Board of Directors will review and approve the appropriateness of

future dividend amounts. A summary of the Company's working

capital (current assets less current liabilities) position and capital-

ization follows (in thousands):

2004 2003 2002

Working capital $238,412 $441,583 $357,585

Capitalization:

Shareholders’ equity $669,326 $857,765 $736,307

The decrease in working capital in fiscal 2004 versus fiscal 2003 was

the result of lower cash and marketable securities resulting primarily

from the Company’s repurchase of 11.2 million shares of common

18 19