Xcel Energy 2007 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2007 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

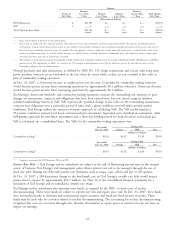

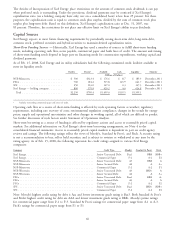

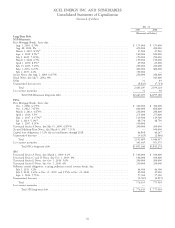

The Articles of Incorporation of Xcel Energy place restrictions on the amount of common stock dividends it can pay

when preferred stock is outstanding. Under the provisions, dividend payments may be restricted if Xcel Energy’s

capitalization ratio (on a holding company basis only, not on a consolidated basis) is less than 25 percent. For these

purposes, the capitalization ratio is equal to common stock plus surplus, divided by the sum of common stock plus

surplus plus long-term debt. Based on this definition, Xcel Energy’s capitalization ratio at Dec. 31, 2007, was

85 percent. Therefore, the restrictions do not place any effective limit on Xcel Energy’s ability to pay dividends.

Capital Sources

Xcel Energy expects to meet future financing requirements by periodically issuing short-term debt, long-term debt,

common stock, preferred securities and hybrid securities to maintain desired capitalization ratios.

Short-Term Funding Sources — Historically, Xcel Energy has used a number of sources to fulfill short-term funding

needs, including operating cash flow, notes payable, commercial paper and bank lines of credit. The amount and timing

of short-term funding needs depend in large part on financing needs for construction expenditures, working capital and

dividend payments.

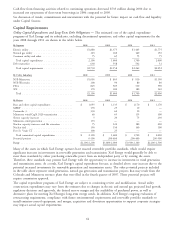

As of Feb. 15, 2008, Xcel Energy and its utility subsidiaries had the following committed credit facilities available to

meet its liquidity needs:

Facility Drawn* Available Cash Liquidity Maturity

(Million of Dollars)

NSP-Minnesota ................... $ 500 $323.4 $ 176.6 $ 8.7 $ 185.3 December 2011

PSCo ......................... 700 184.2 515.8 125.9 641.7 December 2011

SPS .......................... 250 103.0 147.0 0.3 147.3 December 2011

Xcel Energy — holding company ........ 800 179.8 620.2 4.6 624.8 December 2011

Total ........................ $2,250 $790.4 $1,459.6 $139.5 $1,599.1

* Includes outstanding commercial paper and letters of credit.

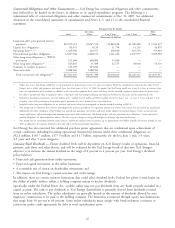

Operating cash flow as a source of short-term funding is affected by such operating factors as weather; regulatory

requirements, including rate recovery of costs; environmental regulation compliance; changes in the trends for energy

prices; supply and operational uncertainties and other changes in working capital, all of which are difficult to predict.

See further discussion of such factors under Statement of Operations Analysis.

Short-term borrowing as a source of funding is affected by regulatory actions and access to reasonably priced capital

markets. For additional information on Xcel Energy’s short-term borrowing arrangements, see Note 4 to the

consolidated financial statements. Access to reasonably priced capital markets is dependent in part on credit agency

reviews and ratings. The following ratings reflect the views of Moody’s, Standard & Poor’s, and Fitch. A security rating

is not a recommendation to buy, sell or hold securities, and is subject to revision or withdrawal at any time by the

rating agency. As of Feb. 15, 2008, the following represents the credit ratings assigned to various Xcel Energy

companies:

Company Credit Type Moody’s Standard & Poor’s Fitch

Xcel Energy ........................................ Senior Unsecured Debt Baa1 BBB BBB+

Xcel Energy ........................................ Commercial Paper P-2 A-2 F2

NSP-Minnesota ..................................... Senior Unsecured Debt A3 BBB A

NSP-Minnesota ..................................... Senior Secured Debt A2 A A+

NSP-Minnesota ..................................... Commercial Paper P-2 A-2 F1

NSP-Wisconsin ..................................... Senior Unsecured Debt A3 BBB+ A

NSP-Wisconsin ..................................... Senior Secured Debt A2 A A+

PSCo ............................................ Senior Unsecured Debt Baa1 BBB A-

PSCo ............................................ Senior Secured Debt A3 A A

PSCo ............................................ Commercial Paper P-2 A-2 F2

SPS............................................. Senior Unsecured Debt Baa1 BBB+ BBB+

SPS............................................. Commercial Paper P-2 A-2 F2

Note: Moody’s highest credit rating for debt is Aaa and lowest investment grade rating is Baa3. Both Standard & Poor’s

and Fitch’s highest credit rating for debt are AAA and lowest investment grade rating is BBB-. Moody’s prime ratings

for commercial paper range from P-1 to P-3. Standard & Poor’s ratings for commercial paper range from A-1 to A-3.

Fitch’s ratings for commercial paper range from F1 to F3.

66