Whole Foods 2015 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2015 Whole Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

|

|

39

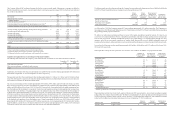

the cost method of accounting and classified as “Other assets” on the Consolidated Balance Sheet. Under the cost method,

investments are carried at cost and are adjusted only for other-than-temporary declines in fair value, certain distributions, and

additional investments. Additionally, the Company holds certain equity interests accounted for using the equity method of

accounting. The Company’s share of income and losses from equity method investments is included in “Selling, general and

administrative expenses” on the Consolidated Statements of Operations.

Restricted Cash

Restricted cash primarily relates to cash held as collateral to support a portion of our projected workers’ compensation obligations.

Additionally, the Company holds restricted cash as a rent guarantee on certain operating leases through fiscal year 2020.

Accounts Receivable

Accounts receivable are shown net of related allowances and consist primarily of credit card receivables, vendor receivables,

customer purchases, and occupancy-related receivables. Vendor receivable balances are generally presented on a gross basis

separate from any related payable due. Allowance for doubtful accounts is calculated based on historical experience, customer

credit risk and application of the specific identification method and was not material in fiscal year 2015 or 2014.

Inventories

The Company values inventories at the lower of cost or market. Cost was determined using the dollar value retail last-in, first-

out (“LIFO”) method for approximately 92.2% and 93.5% of inventories in fiscal years 2015 and 2014, respectively. Under the

LIFO method, the cost assigned to items sold is based on the cost of the most recent items purchased. As a result, the costs of

the first items purchased remain in inventory and are used to value ending inventory. The excess of estimated current costs over

LIFO carrying value, or LIFO reserve, was approximately $49 million and $48 million at September 27, 2015 and September 28,

2014, respectively. Costs for remaining inventories are determined by the first-in, first-out method. Cost before the LIFO

adjustment is principally determined using the item cost method, which is calculated by counting each item in inventory, assigning

costs to each of these items based on the actual purchase cost (net of vendor allowances) of each item and recording the actual

cost of items sold.

Property and Equipment

Property and equipment is stated at cost, net of accumulated depreciation and amortization. The Company provides depreciation

of equipment over the estimated useful lives (generally 3 to 15 years) using the straight-line method, and provides amortization

of leasehold improvements and real estate assets under capital leases on a straight-line basis over the shorter of the estimated

useful lives of the improvements or the expected terms of the related leases. The Company provides depreciation of buildings

over the estimated useful lives (generally 20 to 50 years) using the straight-line method. Costs related to a projected site determined

to be unsatisfactory and general site selection costs that cannot be identified with a specific store location are charged to operations

currently. The Company recognizes a liability for the fair value of a conditional asset retirement obligation when the obligation

is incurred. Repair and maintenance costs are expensed as incurred. Upon retirement or disposal of assets, the cost and related

accumulated depreciation are removed from the balance sheet and any gain or loss is reflected in earnings.

Leases

The Company generally leases stores, non-retail facilities and administrative offices under operating leases. Store lease

agreements generally include rent holidays, rent escalation clauses and contingent rent provisions for percentage of sales in

excess of specified levels. We recognize rent on a straight-line basis over the expected term of the lease, which includes rent

holiday periods and scheduled rent increases. The expected lease term begins with the date the Company has the right to possess

the leased space for construction and other purposes. The expected lease term may also include the exercise of renewal options

if the exercise of the option is determined to be reasonably assured. The expected lease term is also used in the determination

of whether a store is a capital or operating lease. Amortization of land and building under capital lease is included with occupancy

costs, while the amortization of equipment under capital lease is included with depreciation expense. Additionally, we review

leases for which we are involved in construction to determine whether build-to-suit and sale-leaseback criteria are met. For those

leases that trigger specific build-to-suit accounting, developer assets are recorded during the construction period with an offsetting

liability. Developer assets recorded as of September 27, 2015 were not material. As of September 28, 2014, the Company had

developer assets totaling approximately $67 million, with the offsetting liability included in the “Other current liabilities” line

item on the Consolidated Balance Sheets. Sale-leaseback transactions are recorded as financing lease obligations. We record

tenant improvement allowances and rent holidays as deferred rent liabilities, and amortize the deferred rent over the expected

lease term to rent. We record rent liabilities for contingent percentage of sales lease provisions when we determine that it is

probable that the specified levels as defined by the lease will be reached.

40

Goodwill and Intangible Assets

Goodwill consists of the excess of cost of acquired enterprises over the sum of the amounts assigned to identifiable assets

acquired less liabilities assumed. Goodwill is reviewed for impairment annually at the Company’s fiscal year end, or more

frequently if impairment indicators arise, on a reporting unit level. We allocate goodwill to one reporting unit for goodwill

impairment testing. A qualitative assessment, based on macroeconomic factors, industry and market conditions and company-

specific performance, is performed to determine whether it is more likely than not that the fair value of the reporting unit is

impaired. If it is more likely than not, we compare our fair value, which is determined utilizing both a market value method and

discounted projected future cash flows, to our carrying value for the purpose of identifying impairment.

Intangible assets include acquired leasehold rights, favorable lease assets, trade names, brand names, patents, liquor licenses,

license agreements, and non-competition agreements. The Company amortizes definite-lived intangible assets on a straight-line

basis over the period the intangible asset is expected to generate cash flows, generally the life of the related agreement. Currently,

the weighted average life is approximately 16 years for contract-based intangible assets and approximately two years for

marketing-related and other identifiable intangible assets. Indefinite-lived intangible assets are reviewed for impairment quarterly,

or whenever events or changes in circumstances indicate the carrying amount of an intangible asset may not be recoverable.

Impairment of Long-Lived Assets and Long-Lived Assets to be Disposed of

The Company evaluates long-lived assets for impairment whenever events or changes in circumstances, such as unplanned

negative cash flow, short lease life, or a plan to close is established, indicate that the carrying amount of an asset may not be

recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to

future undiscounted cash flows expected to be generated by the asset. If such assets are determined to be impaired, the impairment

to be recognized is measured by the amount by which the carrying value of the assets exceeds the fair value of the assets. The

fair value, based on hierarchy input Level 3, is determined using management’s best estimate based on a discounted cash flow

model based on future store operating results using internal projections or based on a review of the future benefit the Company

anticipates receiving from the related assets. Additionally for closing locations, the Company estimates net future cash flows

based on its experience and knowledge of the area in which the closed property is located and, when necessary, utilizes local

real estate brokers. Assets to be disposed of are reported at the lower of the carrying amount or fair value less costs to sell. When

the Company impairs assets related to an operating location, a charge to write down the related assets is included in the “Selling,

general and administrative expenses” line item on the Consolidated Statements of Operations. When the Company commits to

relocate, close, or dispose of a location, a charge to write down the related assets to their estimated recoverable value is included

in the “Relocation, store closure and lease termination costs” line item on the Consolidated Statements of Operations.

Fair Value of Financial Instruments

The Company records its financial assets and liabilities at fair value in accordance with the framework for measuring fair value

in generally accepted accounting principles. This framework establishes a fair value hierarchy that prioritizes the inputs used to

measure fair value:

• Level 1: Observable inputs that reflect unadjusted quoted prices for identical assets or liabilities traded in active markets.

• Level 2: Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly

or indirectly.

• Level 3: Inputs that are generally unobservable. These inputs may be used with internally developed methodologies that

result in management’s best estimate of fair value.

The Company holds money market fund investments that are classified as cash equivalents that are measured at fair value on a

recurring basis based on quoted prices in active markets for identical assets. The Company also holds available-for-sale securities

generally consisting of state and local municipal obligations and corporate bonds and commercial paper which hold high credit

ratings. These instruments are valued using a series of multi-dimensional relational models and series of matrices with standard

inputs obtained from readily available pricing sources and other observable market data, such as benchmark yields and base

spread. Investments are stated at fair value with unrealized gains and losses, net of related tax effect, included as a component

of shareholders’ equity until realized. Declines in fair value below the Company’s carrying value deemed to be other than

temporary are charged against net earnings.

The carrying amounts of accrued payroll, bonuses and other benefits due team members, and other accrued expenses approximate

fair value because of their short maturities. Store closure reserves and estimated workers’ compensation claims are recorded at

net present value to approximate fair value.