Whole Foods 2015 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2015 Whole Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

|

|

27

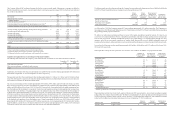

adjustment is principally determined using the item cost method, which is calculated by counting each item in inventory, assigning

costs to each of these items based on the actual purchase cost (net of vendor allowances) of each item and recording the actual

cost of items sold.

Goodwill and Intangible Assets

Goodwill consists of the excess of cost of acquired enterprises over the sum of the amounts assigned to identifiable assets

acquired less liabilities assumed. Goodwill is reviewed for impairment annually at the Company’s fiscal year end, or more

frequently if impairment indicators arise, on a reporting unit level. We allocate goodwill to one reporting unit for goodwill

impairment testing. A qualitative assessment, based on macroeconomic factors, industry and market conditions and company-

specific performance, is performed to determine whether it is more likely than not that the fair value of the reporting unit is

impaired. If it is more likely than not, we compare our fair value, which is determined utilizing both a market value method and

discounted projected future cash flows, to our carrying value for the purpose of identifying impairment. Our annual impairment

review requires extensive use of accounting judgment and financial estimates. Application of alternative assumptions and

definitions, such as reviewing goodwill for impairment at a different organizational level, could produce significantly different

results. Because of the significance of the judgments and estimation processes, it is possible that materially different amounts

could be recorded if we used different assumptions or if the underlying circumstances were to change.

Impairment of Long-Lived Assets and Long-Lived Assets to be Disposed of

The Company evaluates long-lived assets for impairment whenever events or changes in circumstances, such as unplanned

negative cash flow, short lease life, or a plan to close is established, indicate that the carrying amount of an asset may not be

recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to

future undiscounted cash flows expected to be generated by the asset. If such assets are determined to be impaired, the impairment

to be recognized is measured by the amount by which the carrying amount of the assets exceeds the fair value of the assets. The

fair value, based on hierarchy input Level 3, is determined using management’s best estimate based on a discounted cash flow

model based on future store operating results using internal projections or based on a review of the future benefit the Company

anticipates receiving from the related assets. Additionally for closing locations, the Company estimates net future cash flows

based on its experience and knowledge of the area in which the closed property is located and, when necessary, utilizes local

real estate brokers. Assets to be disposed of are reported at the lower of the carrying amount or fair value less costs to sell.

Application of alternative assumptions, such as changes in estimates of future cash flows, could produce significantly different

results. Because of the significance of the judgments and estimation processes, it is likely that materially different amounts could

be recorded if we used different assumptions or if the underlying circumstances were to change.

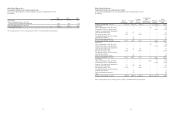

Insurance and Self-Insurance Liabilities

The Company uses a combination of insurance and self-insurance plans to provide for the potential liabilities for workers’

compensation, general liability, property insurance, director and officers’ liability insurance, vehicle liability, and employee

health care benefits. Liabilities associated with the risks that are retained by the Company are estimated, in part, by considering

historical claims experience, demographic factors, severity factors and other actuarial assumptions. While we believe that our

assumptions are appropriate, the estimated accruals for these liabilities could be significantly affected if future occurrences and

claims differ from these assumptions and historical trends.

We have not made any changes in the accounting methodology used to establish our insurance and self-insured liabilities during

the past three fiscal years.

Because of the significance of the judgments and estimation processes, it is likely that materially different amounts could be

recorded if we used different assumptions or if the underlying circumstances were to change. A 10% change in our insurance

and self-insured liabilities at September 27, 2015 would have affected net income by approximately $10 million for fiscal year

2015.

Leases

The Company generally leases stores, non-retail facilities and administrative offices under operating leases. Store lease

agreements generally include rent holidays, rent escalation clauses and contingent rent provisions for percentage of sales in

excess of specified levels. We recognize rent on a straight-line basis over the expected term of the lease, which includes rent

holiday periods and scheduled rent increases. The expected lease term begins with the date the Company has the right to possess

the leased space for construction and other purposes. The expected lease term may also include the exercise of renewal options

if the exercise of the option is determined to be reasonably assured. The expected lease term is also used in the determination

of whether a store is a capital or operating lease. Amortization of land and building under capital lease is included with occupancy

costs, while the amortization of equipment under capital lease is included with depreciation expense. Additionally, we review

leases for which we are involved in construction to determine whether build-to-suit and sale-leaseback criteria are met. For those

28

leases that trigger specific build-to-suit accounting, developer assets are recorded during the construction period with an offsetting

liability. Sale-leaseback transactions are recorded as financing lease obligations. We record tenant improvement allowances and

rent holidays as deferred rent liabilities, and amortize the deferred rent over the expected lease term to rent. We record rent

liabilities for contingent percentage of sales lease provisions when we determine that it is probable that the specified levels as

defined by the lease will be reached.

Reserves for Closed Properties

The Company maintains reserves for retail stores and other properties that are no longer being utilized in current operations.

The Company provides for closed property operating lease liabilities using a discount rate to calculate the present value of the

remaining noncancelable lease payments and lease termination fees after the closing date, net of estimated subtenant income.

The closed property lease liabilities are expected to be paid over the remaining lease terms, which generally range from three

months to 9 years. The reserves for closed properties include management’s estimates for lease subsidies, lease terminations

and future payments on exited real estate. The Company estimates subtenant income and future cash flows based on the Company’s

experience and knowledge of the area in which the closed property is located, the Company’s previous efforts to dispose of

similar assets, existing economic conditions and when necessary utilizes local real estate brokers.

Adjustments to closed property reserves primarily relate to changes in estimated subtenant income or actual exit costs differing

from original estimates. Adjustments are made for changes in estimates in the period in which the changes become known.

Because of the significance of the judgments and estimation processes, it is likely that materially different amounts could be

recorded if we used different assumptions or if the underlying circumstances were to change. A 10% change in our closed

property reserves at September 27, 2015 would not have materially affected net income for fiscal year 2015.

Share-Based Payments

The Company maintains several share-based incentive plans. We grant both options to purchase common stock and restricted

common stock under our Whole Foods Market 2009 Stock Incentive Plan. Options outstanding are governed by the original

terms and conditions of the grants, unless modified by a subsequent agreement. Options are granted at an option price equal to

the market value of the stock at the grant date and generally vest ratably over a four- or nine-year period beginning one year

from grant date and have a five, seven or ten year term. The grant date is established once the Company’s Board of Directors

approves the grant and all key terms have been determined. Stock option grant terms and conditions are communicated to team

members within a relatively short period of time. Our Company generally approves one primary stock option grant annually,

occurring during a trading window. Restricted common stock is granted at the market price of the stock on the day of grant and

generally vests over a four- or six-year period.

The Company uses the Black-Scholes multiple option pricing model which requires extensive use of accounting judgment and

financial estimates, including estimates of the expected term team members will retain their vested stock options before exercising

them, the estimated volatility of the Company’s common stock price over the expected term, and the number of options that will

be forfeited prior to the completion of their vesting requirements. The related share-based payment expense is recognized on a

straight-line basis over the requisite service period. The tax savings resulting from tax deductions in excess of expense reflected

in the Company’s financial statements are reflected as a financing cash flow.

The Company intends to keep its broad-based stock option program in place, but also intends to limit the number of shares

granted in any one year so that annual earnings per share dilution from share-based payment expense will not exceed 10%.

We do not believe there is a reasonable likelihood that there will be a material change in the future estimates or assumptions we

use to determine share-based payment expense. However, if actual results are not consistent with our estimates or assumptions,

we may be exposed to changes in share-based payment expense that could be material.

Because of the significance of the judgments and estimation processes, it is likely that materially different amounts could be

recorded if we used different assumptions or if the underlying circumstances were to change. A 10% change in our share-based

payment expense would not have materially affected net income for fiscal year 2015.

Income Taxes

We recognize deferred income tax assets and liabilities by applying statutory tax rates in effect at the balance sheet date to

differences between the book basis and the tax basis of assets and liabilities. Deferred tax assets and liabilities are measured

using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to

reverse. Deferred tax assets and liabilities are adjusted to reflect changes in tax laws or rates in the period that includes the

enactment date. Significant accounting judgment is required in determining the provision for income taxes and related accruals,