Westjet 2005 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2005 Westjet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64

|

|

2005 WESTJET ANNUAL REPORT

59

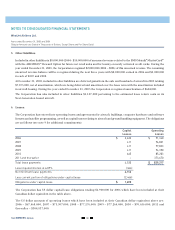

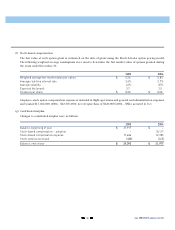

(d) Credit risk:

The Corporation does not believe it is subject to any significant concentration of credit risk. Most of the Corporation’s

receivables result from tickets sold to individual guests through the use of major credit cards and travel agents. These

receivables are short-term, generally being settled shortly after the sale. The Corporation manages the credit exposure

related to financial instruments by selecting counter parties based on credit ratings, limiting its exposure to any single

counter party and monitoring the market position of the program and its relative market position with each counter

party.

(e) Ontario Teachers’ Financing Agreement:

The Corporation had an agreement with Ontario Teachers’ Pension Plan Board (“Ontario Teachers”) for the right to

require Ontario Teachers to purchase up to $100,000,000 of common shares, which

expired in 2004. The Corporation

elected not to exercise the financing agreement and has included the 1% annual standby fee in general and administration

expenses for the year ended December 31, 2004.

(f) Fair value of financial instruments:

The carrying amounts of financial instruments included in the balance sheet, other than long-term debt, approximate

their fair value due to their short term to maturity.

At December 31, 2005, the fair value of long-term debt was approximately $1.2 billion (2004 – $1.1 billion).

The fair value of

long-term debt is determined by discounting the future contractual cash flows under current financing arrangements

at discount rates which represent borrowing rates presently available to the Corporation for loans with similar terms

and maturity.