Vistaprint 2015 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2015 Vistaprint annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

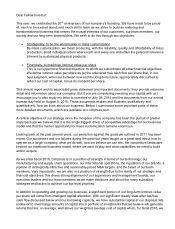

estimate to be 8.5%. We consider any use of cash that we expect to require more than 12 months to

return our invested capital to be an allocation of capital.

Our capital allocation can be grouped into several broad categories: organic long-term investments

(which we also refer to as discretionary growth spending), share repurchases, M&A, and repayment of

debt. We consider our capital to be fungible across all of these categories. Because of the

attractiveness of these categories we do not intend to pay dividends for the foreseeable future.

Given the significant investments and acquisitions that we need and expect to make as we execute on

our multi-decade opportunity, over the past year we've spent significant time thinking about a concept

we refer to as our steady state after-tax free cash flow per share. We define “steady state” as having a

sustainable and defensible business over the long term capable of growing after-tax free cash flow per

share at the rate of inflation.

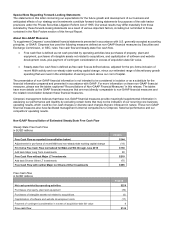

We believe our steady state free cash flow for fiscal year 2015 lay somewhere between $210 million

and $385 million1. Note that we had 33.8 million weighted average diluted shares outstanding for the

year ended June 30, 2015. Since our uppermost financial objective is per-share based, we evaluate our

steady state free cash flow at a per-share level. Our analysis of the steady state concept is relatively

new and is inherently subjective but, over time, we will seek to become more precise about our public

estimates of the prior fiscal year’s steady state free cash flow. Importantly, in my July 29, 2015 letter to

investors and in our August 5, 2015 investor day presentation we provided significant amount of detail

that we believe enables an investor to make his or her own judgments of a narrower range of steady

state free cash flow per share.

Estimates of steady state are important for us and shareholders to understand because the difference

between the actual after-tax free cash flow and an estimate of steady state after-tax free cash flow

represents an estimate of discretionary growth spending that we invest in the anticipation of earning a

return above our cost of capital. We look to the future with optimism because we see the opportunity to

make large amounts of such value-creating investments for years to come.

I would like to thank each of our team members for their hard work and dedication last year. As of June

30, 2015, we employed over 6,500 team members in more than 20 different locations across 19

countries. Without their talents we could never have grown into this company, and we could never

achieve the objectives set out above.

Sincerely,

Robert S. Keane

Chairman of the Management Board, President and CEO

1 Please see reconciliation of non-GAAP financial measures at the end of this letter.