United Healthcare 2002 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2002 United Healthcare annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

{ 34 }

UnitedHealth Group

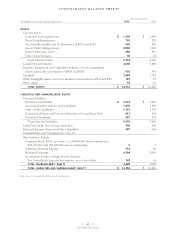

REGULATORY CAPITAL AND DIVIDEND RESTRICTIONS

We conduct a significant portion of our operations through companies that are subject to standards

established by the National Association of Insurance Commissioners (NAIC). These standards, among other

things, require these subsidiaries to maintain specified levels of statutory capital, as defined by each state, and

restrict the timing and amount of dividends and other distributions that may be paid to their parent

companies. Generally, the amount of dividend distributions that may be paid by a regulated subsidiary,

without prior approval by state regulatory authorities, is limited based on the entity’s level of statutory net

income and statutory capital and surplus. The agencies that assess our creditworthiness also consider capital

adequacy levels when establishing our debt ratings. Consistent with our intent to maintain our senior debt

ratings in the “A” range, we maintain an aggregate statutory capital level for our regulated subsidiaries that is

significantly higher than the minimum level regulators require. As of December 31, 2002, our regulated

subsidiaries had aggregate statutory capital of approximately $2.5 billion, which is significantly more than the

aggregate minimum regulatory requirements.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Critical accounting policies are those policies that require management to make the most challenging,

subjective or complex judgments, often because they must estimate the effects of matters that are

inherently uncertain and may change in subsequent periods. Critical accounting policies involve

judgments and uncertainties that are sufficiently sensitive to result in materially different results under

different assumptions and conditions. We believe our most critical accounting policies are those

described below. For a detailed discussion of these and other accounting policies, see Note 2 to the

Consolidated Financial Statements.

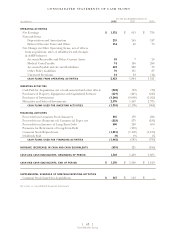

REVENUES

Revenues are principally derived from health care insurance premiums. We recognize premium revenues

in the period eligible individuals are entitled to receive health care services. Customers are typically billed

monthly at a contracted rate per eligible person multiplied by the total number of people eligible to

receive services, as recorded in our records. Employer groups generally provide us with changes to their

eligible population one month in arrears. Each billing includes an adjustment for prior month changes in

eligibility status that were not reflected in our previous billing. We estimate and adjust the current period’s

revenues and accounts receivable accordingly. Our estimates are based on historical trends, premiums

billed, the level of contract renewal activity and other relevant information. We also estimate the amount

of uncollectible receivables each period and record valuation allowances based on historical collection

rates, the age of unpaid amounts, and information about the creditworthiness of the customers. We revise

estimates of revenue adjustments and uncollectible accounts receivable each period, and record changes

in the period they become known.