Tesco 2013 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2013 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

21

Tesco PLC Annual Report and Financial Statements 2013

OVERVIEW BUSINESS REVIEW PERFORMANCE REVIEW GOVERNANCE FINANCIAL STATEMENTS

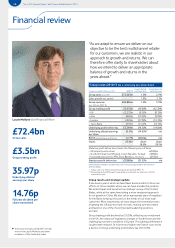

Group statutory profit before tax declined by (51.5)% to £1,960

million due to the impact of three main one-off charges:

• UK property write-down of £(804) million, following an in-depth

review of our property pipeline in the context of our fundamentally

different approach to new space and our announcement in April

2012 that we would be reducing the level of new space growth in

the UK going forward;

• Goodwill impairment of £(495) million, reflecting the impact

of differing growth prospects in today’s environment for the

businesses we acquired in Poland, the Czech Republic and Turkey

in the mid 1990s to early 2000s; and

• Increase of £(115) million in our provision for potential Payment

Protection Insurance claims against Tesco Bank.

Based on our progress so far with our strategic review of Fresh &

Easy, we have confirmed that the outcome of the review will be

an exit from the United States. The results of our business there,

in addition to those of our business in Japan, have been classified

as discontinued operations in these results.

Segmental results

UK

It is a year since we unveiled our six-part plan to get the UK business

back on top form. The UK is absolutely fundamental to the success

of the Group, which is why this was our number one priority for the

year, and I’m pleased to say the plan is very much on track.

We have made the investment as planned and it has led to a clear

improvement in performance, both in absolute terms and relative to

the market. Total sales rose by 2.6% excluding petrol, and like-for-

like performance improved during the course of the year, with a

particularly encouraging result at Christmas.

UK results 2012/13

£m % growth

UK sales £48,216m 1.8%

UK revenue (exc. VAT, exc. impact of IFRIC 13) £43,579m 1.8%

UK revenue (exc. petrol, exc. VAT, exc. impact of IFRIC 13) 2.6%

UK trading profit £2,272m (8.3)%

Trading margin (trading profit/revenue) 5.21% (58)bp

When we laid out our plans last year, we described the impact of

the investment in terms of a rebasing of our trading margin to 5.2%

and the progress we have made in the UK has been achieved whilst

delivering a margin absolutely in line with these expectations.

The most important judge of progress is the customer and we

introduced a new way of measuring customer perceptions back

in July – our ‘customer viewpoint’. This measures real customer

feedback in all of our stores on a regular and frequent basis, across

12 aspects of their shopping trip. Pleasingly, every one of these

aspects improved throughout the second half of the year. This

underpins our confidence that the underlying improvement we

have seen in our trading performance is driven by the changes

we have made for customers.

While there are a number of drivers that could enable us to improve

overall UK margins, we believe the new base of 5.2% is appropriate

for the foreseeable future and any outperformance will be reinvested

in driving additional improvements in our customer offer.

Asia

Our Asia performance was in line with expectations and was

dominated by the South Korean regulatory changes concerning

trading hours. These changes held back headline numbers, and the

impact on trading profit was broadly in line with our £(100) million

guidance, with significant levels of Sunday store closures throughout

the second half and considerable uncertainty in the market about

exactly which stores would be closed and when, impacting operations

even when stores were able to open. Following the passing of the

legislation in January this year, the situation seems more certain,

with more consistent store closures expected on alternate Sundays.

As such, we expect the full-year effect of the regulations, combined

with the extension of 24-hour trading restrictions to between

midnight and 10am, to lead to an incremental impact of around

£(40) million in 2013/14.

Asia results* 2012/13

Actual rates Constant rates

£m % growth % growth

Asia sales £12,317m 5.9% 6.1%

Asia revenue

(exc. VAT, exc. impact of IFRIC 13)

£11,479m 6.0% 6.2%

Asia trading profit £661m (10.3)% (9.8)%

Trading margin (trading profit/revenue) 5.76% (105)bp (102)bp

* Exc. Japan.

In Thailand, like-for-like sales grew by 3.1% and we continued to

gain market share. We benefited from a strong opening programme,

including almost 300 Express stores and we launched our first

dotcom grocery operation in Bangkok in February.

We have adopted a more cautious stance in China. We still see

an excess amount of new space being opened in the market –

ahead of customer demand – and we have moderated our pace of

development accordingly, opening just 12 new stores this year and

closing five underperforming stores as part of our increased focus

on our three strongest regions.

Europe

Whilst our markets in Europe remain fundamentally attractive,

our performance this year was disappointing.

Clearly, we faced significant headwinds throughout the year, as

macroeconomic uncertainties continued to impact businesses.

This had a particularly marked impact on our general merchandise

businesses across the region, holding back our overall like-for-like

sales performance.

Europe results 2012/13

Actual rates Constant rates

£m % growth % growth

Europe sales £10,809m (4.9)% 2.1%

Europe revenue

(exc. VAT, exc. impact of IFRIC 13)

£9, 319m (5.5)% 1.4%

Europe trading profit £329m ( 37. 8)% (33.3)%

Trading margin (trading profit/revenue) 3.53% (183)bp (183)bp