Rite Aid 2015 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2015 Rite Aid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

RITE AID CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

For the Years Ended February 28, 2015, March 1, 2014 and March 2, 2013

(In thousands, except per share amounts)

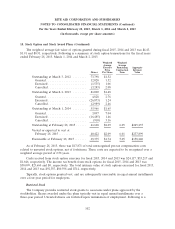

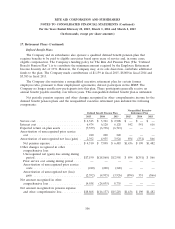

13. Indebtedness and Credit Agreement (Continued)

with available cash, were used to repurchase the 8.625% senior notes and the 9.375% senior notes,

respectively. These notes are unsecured, unsubordinated obligations of Rite Aid Corporation and rank

equally in right of payment with all other unsubordinated indebtedness. The Company’s obligations

under the notes are fully and unconditionally guaranteed, jointly and severally, on an unsubordinated

basis, by all of its subsidiaries that guarantee the Company’s obligations under the senior secured credit

facility, the second priority secured term loan facility and the outstanding 8.00% senior secured notes,

7.5% senior secured notes, 10.25% senior secured notes and 9.5% senior notes.

In May 2012, the Company completed a tender offer for the 9.375% notes in which $296,269

aggregate principal amount of the outstanding 9.375% notes were tendered and repurchased. In June

2012, the Company redeemed the remaining 9.375% notes for $108,731, which included the call

premium and interest through the redemption date. The May 2012 refinancing resulted in an aggregate

loss on debt retirement of $17,842.

Interest Rates and Maturities

The annual weighted average interest rate on the Company’s indebtedness was 5.7%, 6.4%, and

7.1% for fiscal 2015, 2014, and 2013, respectively.

The aggregate annual principal payments of long-term debt for the five succeeding fiscal years are

as follows: 2016—$69,535; 2017—$0; 2018—$0; 2019—$0 and $5,480,000 in 2020 and thereafter.

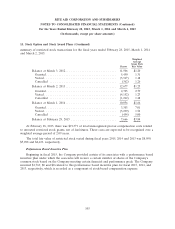

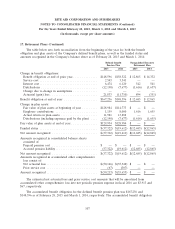

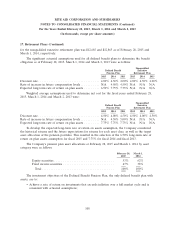

14. Leases

The Company leases most of its retail stores and certain distribution facilities under noncancellable

operating and capital leases, most of which have initial lease terms ranging from 5 to 22 years. The

Company also leases certain of its equipment and other assets under noncancellable operating leases

with initial terms ranging from 3 to 10 years. In addition to minimum rental payments, certain store

leases require additional payments based on sales volume, as well as reimbursements for taxes,

maintenance and insurance. Most leases contain renewal options, certain of which involve rent

increases. Total rental expense, net of sublease income of $8,559, $8,369, and $8,536, was $964,484,

$952,777, and $951,239 in fiscal 2015, 2014, and 2013, respectively. These amounts include contingent

rentals of $18,919, $18,679 and $21,026 in fiscal 2015, 2014, and 2013, respectively.

During fiscal 2015, the Company did not enter into any sale-leaseback transactions whereby the

Company sold owned operating stores to independent third parties and concurrent with the sale,

entered into an agreement to lease the store back from the purchasers.

During fiscal 2014, the Company sold one owned operating store to an independent third party.

Net proceeds from the sale were $3,989. Concurrent with this sale, the Company entered into an

agreement to lease the store back from the purchaser over a minimum lease term of 20 years. The

Company accounted for this lease as an operating lease. The transaction resulted in a gain of $269

which is included in the gain on sale of assets, net for the fifty-two weeks ended March 1, 2014.

During fiscal 2013, the Company sold two owned operating stores to independent third parties.

Net proceeds from the sale were $6,355. Concurrent with these sales, the Company entered into

agreements to lease the stores back from the purchasers over a minimum lease term of 12 to 20 years.

98