Porsche 2012 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2012 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

|

|

Consolidation principles

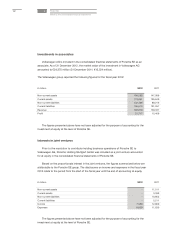

As the accounting at equity has a significant influence on the net assets and results of oper-

ations of the Porsche SE group, the consolidation principles applicable only within the Porsche

Holding Stuttgart GmbH group and the Volkswagen group are also included in the explanations

below.

In the reporting period, the financial statements of all subsidiaries and investments account-

ed for at equity were prepared as of the reporting date of the consolidated financial statements,

which is the reporting date of Porsche SE. Where necessary, adjustments are made to uniform

group accounting policies.

Business combinations are accounted for by applying the acquisition method pursuant to

IFRS 3 (rev. 2008).

The cost of a business combination is measured in accordance with IFRS 3 (rev. 2008) as

the aggregate of the consideration transferred at fair value as of the acquisition date, measured

at acquisition-date fair value, and the non-controlling interests in the entity. The non-controlling

interests can be measured either at fair value or at the proportionate share of the acquiree’s

identifiable net assets. Acquisition-related costs are expensed and therefore do not constitute a

component of cost. Contingent consideration is measured at the fair value on the acquisition

date. Subsequent changes in value do not generally lead to an adjustment in the measurement

as of the acquisition date.

If the business combination is achieved in stages, the acquisition-date fair value of the ac-

quirer’s previously held equity interest in the acquiree is remeasured to fair value as of the acqui-

sition date and the gain or loss resulting from remeasurement recognized in profit or loss.

Where the cost of a business combination exceeds the fair value of identifiable assets ac-

quired net of liabilities assumed as of the acquisition date, the excess is recognized as goodwill.

In contrast, where the cost of a business combination is less than the fair value of identifiable

assets acquired net of liabilities assumed as of the acquisition date, the difference is recognized

in the income statement after reassessing the fair values.

Any difference arising upon acquisition of additional shares or sale of shares after initial con-

solidation without loss of control in a subsidiary that has already been fully consolidated is rec-

ognized within equity.

163