Porsche 2004 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2004 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

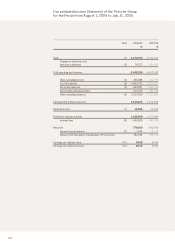

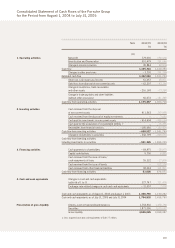

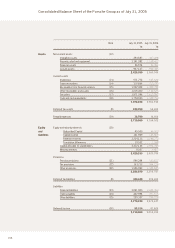

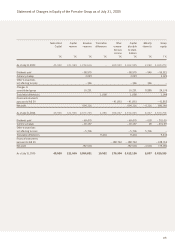

Group Notes Principles110

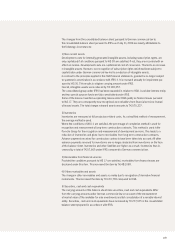

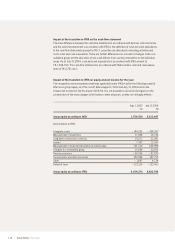

6) Deferred taxes

The differences in deferred taxes are based on different concepts for determining deferred taxes

in HGB and IFRS. Under IFRS, deferred tax assets and liabilities are recognized on all temporary

differences between the tax carrying amounts and the carrying amounts pursuant to IFRS.

Deferred tax assets are recognized when the conditions are met.

7) Pension provisions

Pension provisions under IFRS are calculated using the projected unit credit method pursuant

to IAS 19. The method also takes account of future salary and pension increases. The changes

compared to German commercial law amount to T€ 93,750.

8) Tax provisions and other provisions

Provisions may only be recognized if there is a legal or constructive obligation to third parties

and utilization is probable. Expense provisions are not recognized. Non-current provisions are

discounted to their present value. The aggregate difference amounts to T€ 339,337.

9) Liabilities

The financial liabilities item has essentially changed as a result of first-time consolidation of a

variable interest entity of T€ 254,171. In addition, an amount of T€ 576,825, which represents

some of the asset-backed financing and was reported under deferred income under HGB, was

reclassified and allocated in full to financial liabilities.

Advance payments received for inventories are disclosed as liabilities, which led to an increase

in liabilities compared to HGB. Liabilities thus increased by T€ 392,792 compared to the con-

solidated balance sheet under German commercial law.

10) Deferred income

Those parts of the asset-backed financing which were reported under deferred income in

accordance with HGB were reclassified to financial liabilities.