NVIDIA 2010 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2010 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

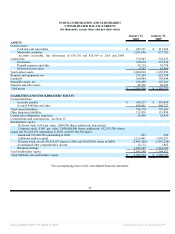

Investment and Interest Rate Risk

As of January 31, 2010 and January 25, 2009, we had $1.73 billion and $1.26 billion, respectively, in cash, cash equivalents and

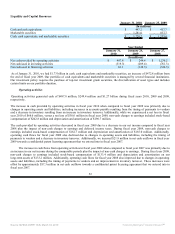

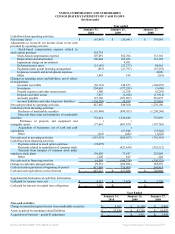

marketable securities. We invest in a variety of financial instruments, consisting principally of cash and cash equivalents, asset-backed

securities, commercial paper, mortgage-backed securities issued by Government-sponsored enterprises, equity securities, money

market funds and debt securities of corporations, municipalities and the United States government and its agencies. As of January 31,

2010, we did not have any investments in auction-rate preferred securities. Our investments are denominated in United States dollars.

All of the cash equivalents and marketable securities are treated as “available-for-sale.” Investments in both fixed rate and floating

rate interest earning instruments carry a degree of interest rate risk. Fixed rate securities may have their market value adversely

impacted due to a rise in interest rates, while floating rate securities may produce less income than expected if interest rates fall. Due

in part to these factors, our future investment income may fall short of expectations due to changes in interest rates or if the decline in

fair value of our publicly traded debt or equity investments is judged to be other-than-temporary. We may suffer losses in principal if

we are forced to sell securities that decline in securities market value due to changes in interest rates. However, because any debt

securities we hold are classified as “available-for-sale,” no gains or losses are realized in our Consolidated Statements of

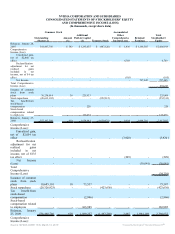

Operations due to changes in interest rates unless such securities are sold prior to maturity or unless declines in value are determined

to be other-than-temporary. These securities are reported at fair value with the related unrealized gains and losses included in

accumulated other comprehensive income (loss), a component of stockholders’ equity, net of tax.

As of January 31, 2010, we performed a sensitivity analysis on our floating and fixed rate financial investments. According to our

analysis, parallel shifts in the yield curve of both plus or minus 0.5% would result in changes in fair market values for these

investments of approximately $8.3 million.

The financial turmoil that affected the banking system and financial markets and increased the possibility that financial institutions

might consolidate or go out of business resulted in a tightening in the credit markets, a low level of liquidity in many financial

markets, and extreme volatility in fixed income, credit, currency and equity markets. There could be a number of follow-on effects

from the credit crisis on our business, including insolvency of key suppliers resulting in product delays; inability of customers,

including channel partners, to obtain credit to finance purchases of our products and/or customer, including channel partner,

insolvencies; and failure of financial institutions, which may negatively impact our treasury operations. Other income and expense

could also vary materially from expectations depending on gains or losses realized on the sale or exchange of financial instruments;

impairment charges related to debt securities as well as equity and other investments; interest rates; and cash, cash equivalent and

marketable securities balances. Volatility in the financial markets and economic uncertainty increases the risk that the actual amounts

realized in the future on our financial instruments could differ significantly from the fair values currently assigned to them. As of

January 31, 2010, our investments in government agencies and government sponsored enterprises represented approximately 62% of

our total investment portfolio, while the financial sector accounted for approximately 22% of our total investment portfolio. Of the

financial sector investments, over half are guaranteed by the U.S. government. Substantially all of our investments are with A/A2 or

better rated securities. If the fair value of our investments in these sectors was to decline by 2%-5%, fair market values for these

investments would decline by approximately $27-$67 million.

Exchange Rate Risk

We consider our direct exposure to foreign exchange rate fluctuations to be minimal. Gains or losses from foreign currency

remeasurement are included in “Other income (expense), net” in our Consolidated Financial Statements and to date have not been

significant. The impact of foreign currency transaction loss included in determining net income (loss) for fiscal years 2010, 2009 and

2008 was $0.9 million, $2.0 million and $1.7 million, respectively. Currently, sales and arrangements with third-party manufacturers

provide for pricing and payment in United States dollars, and, therefore, are not subject to exchange rate fluctuations. Increases in the

value of the United States’ dollar relative to other currencies would make our products more expensive, which could negatively impact

our ability to compete. Conversely, decreases in the value of the United States’ dollar relative to other currencies could result in our

suppliers raising their prices in order to continue doing business with us. Fluctuations in currency exchange rates could harm our

business in the future.

We may enter into certain transactions such as forward contracts which are designed to reduce the future potential impact

resulting from changes in foreign currency exchange rates. There were no forward exchange contracts outstanding at January 31,

2010.

58

Source: NVIDIA CORP, 10-K, March 18, 2010 Powered by Morningstar® Document Research℠