Food Lion 2003 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2003 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

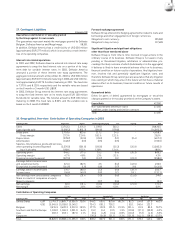

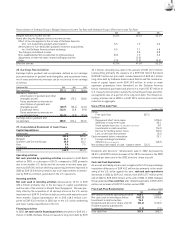

Delhaize Group - Annual Report 2003

58

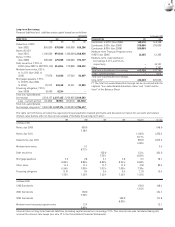

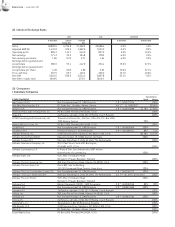

Foreign Currency Transactions

Under Belgian GAAP, the Group had deferred foreign currency trans-

action exchange rate losses incurred on debts contracted to finance

non-monetary assets. These losses were recognized based on the

principle of matching expenses to the income to which they relate.

Under US GAAP, the increase or decrease in expected functional cur-

rency cash flows is a foreign currency transaction gain or loss that is

included in determining net income for the period in which the

exchange rate changes.

Income Taxes

Under Belgian GAAP, Delhaize Group accounts for deferred income

tax assets and liabilities for its U.S. subsidiaries under the provisions

of SFAS 109, Accounting for Income Taxes (SFAS 109). For all other

consolidated entities, deferred income tax assets and liabilities are

calculated on certain, but not all, temporary differences arising in the

accounts of these consolidated entities. Deferred income tax assets

and liabilities are not calculated on tax-exempt reserves and tax loss

carryforwards. Under US GAAP, all subsidiaries of Delhaize Group are

accounted for under the provisions of SFAS 109.

Dividends and Directors’ Remuneration

Under Belgian GAAP, the proposed annual dividend on ordinary

shares to be approved by the General Meeting of Shareholders, which

is held subsequent to year-end, is accrued at year-end. Under US

GAAP, such dividends are not considered an obligation until approved.

Under Belgian GAAP, the directors’ remuneration is considered a dis-

tribution of profits, similar to a dividend to shareholders, and is

recorded as a charge to retained earnings. Under US GAAP, such

remuneration is considered compensation expense.

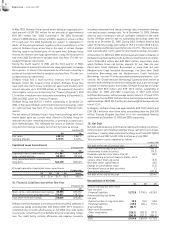

Derivative Instruments

Under US GAAP, Delhaize Group follows the provisions of SFAS 133,

Accounting for Derivative Instruments and Hedging Activities, to

account for derivative instruments such as interest rate swaps or

cross currency swaps. Additionally, under Belgian GAAP, the loss (net

of tax) related to the interest-rate lock agreements that were entered

into prior to the bond issues related to the acquisition of Hannaford,

was classified in the balance sheet caption “Prepayments and

accrued income”. Under US GAAP, this loss was classified in the bal-

ance sheet caption “Other comprehensive income”, which is part of

shareholders’ equity.

Stock Based Compensation

Under Belgian GAAP, compensation expense related to stock options

is not recorded. Under US GAAP, Delhaize Group has elected to follow

the accounting provisions of Accounting Principles Board Opinion

(APBO) N° 25, Accounting for Stock Issued to Employees, for grant of

shares, stock options and other equity instruments. This resulted in

the recording of compensation expense relating to Delhaize

America’s restricted stock plans and Delhaize Group’s stock option

plans. In addition, expenses recorded in Belgian GAAP to recognize

the difference between the market price of a share and its exercise

price when stock options are exercised, are reversed for US GAAP.

The Delhaize America share exchange resulted in a new measure-

ment date for the Delhaize America’s stock option and restricted

stock plans. As a result, a one-time, non-cash compensation expense

of EUR 13.1million pre-tax was recorded in 2001 under US GAAP.

Treasury Shares

Under Belgian GAAP, treasury shares are classified in the balance

sheet caption “Short-term investments” and are subject to a valuation

allowance when the share price at the reporting date is lower than the

acquisition price. Under US GAAP, treasury shares are deducted from

shareholders’ equity in the captions “Capital” and “Additional Paid in

Capital” and are maintained at cost.

Inventories

Under Belgian GAAP, amounts received from suppliers for in-store

promotions and co-operative advertising are recognized when the

activities required by the supplier are completed. Under US GAAP,

Delhaize Group adopted the Emerging Issues Task Force (EITF) Issue

No. 02-16, “Accounting by a Reseller for Cash Consideration

Received” in 2003. EITF issue No. 02-16 directs that cash considera-

tion received from a vendor should be presumed to be a reduction of

inventory, and recognized in cost of sales when the product is sold,

unless it is a reimbursement of specific costs incurred in advertising

the vendor’s products. The resulting before tax adjustment was EUR

15.9million.

Other Items

Other items include adjustments to record differences between

Belgian GAAP and US GAAP for interest cost capitalization, software

development cost capitalization, accounting for security investments

and accounting for a highly inflationary country (Romania).